Online retail sales growth slowed in May following a fairly strong April

Insight

US equities have been boosted by a string of positive data.

https://soundcloud.com/user-291029717/us-bounce-pushes-equities-to-record-highs?in=user-291029717/sets/the-morning-call

Higher, Higher, Higher, Higher, Yeah, Yeah – Kool & The Gang

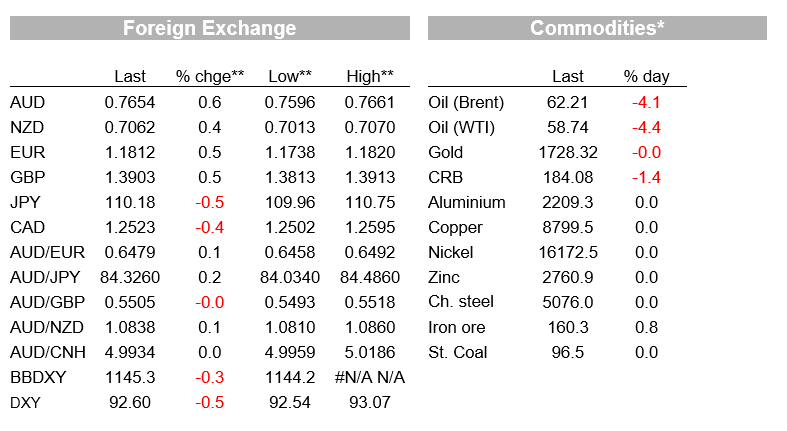

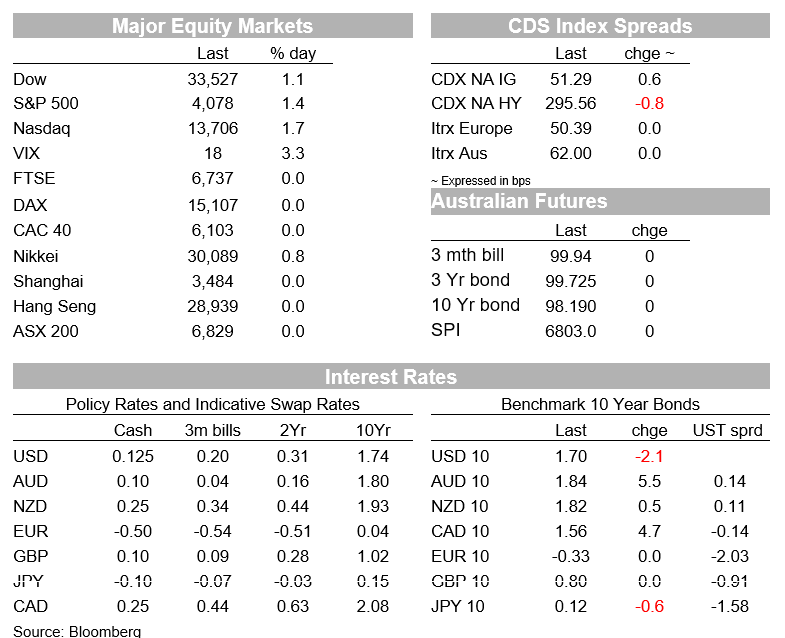

Considering the strength of the US economic news flow since we left off on Thursday for the Easter break, the surprise from a markets perspective is that US bond yields are lower than they were in the middle of last week and the USD is softer – the flip side of which is AUD/USD back above 0.7650 after hitting a new year to date low around 0.7535 on Thursday. Equities have loved the signals from the data alongside the absence of still higher bond yields, the S&P 500 posting a record high on Thursday to close above 4,000 for the fast time, and adding another 1.4% on Monday to 4,078.

The US economic news since last Thursday has all fallen into the ‘strong, and stronger than expected’ bucket, starting with the Manufacturing ISM at 64.7, up from 60.8 in March and well above the 61.5 expected. Then Friday’s non-farm payrolls jumped by 916k – plus there were 156k worth of upward revisions to the prior two months – well above the 660k consensus. The unemployment rate dropped by 2/10% to 6.0% (as expected) but the U6 underemployment rates fell by 4/10% to 10.7%. Average hourly earnings growth is now trending back lower as the majority of jobs being regained (specifically in hospitality and leisure) are at the lower end of the pay spectrum, biasing down the average (to 4.2% y/y from 5.3% last time). And then overnight we’ve had the Services ISM printing at 63.7, the strongest since this series began in 1997, up from 55.3 in February and well above the 59.0 consensus.

Prices paid in the Services report were up to their highest since before the GFC at 74.0 from 71.8, though supply chain issued are doubtless still a factor here (and in which respect Cleveland Fed President Loretta Mester has just been out saying that businesses she speaks to don’t have pricing power). She also notes that the level of employment is still 8.5 million below where it was prior to the pandemic.

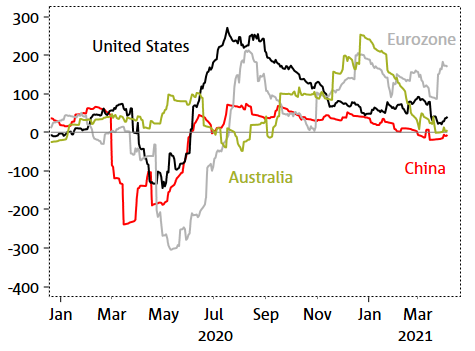

Europe has been out for the four days the same as Australia and NZ so no economic news there, though covid related news flow continues to make grim reading, with France having gone into a fresh 28 lockdown amid infection rates now the second highest since the pandemic started (Italy was also in lockdown for Easter). There is as yet no sign of a significant pick up in vaccination rates (less then 14% of EU citizens have received a first dose, compared to over 50% in the UK and 40% in the US). Despite this, it’s worth noting that even with the trifecta of strong US numbers since last Thursday, the Citi economic surprise indices published daily by Bloomberg still have the EU ahead of the US (as well as China and Australia – see chart below). The covid news may be disconcerting, but the EU economy is showing some surprising resilience.

So the US equity market has posted consecutive record highs – on Thursday and Monday – with IT, Consumer Discretionaries and Communications sectors leading Monday’s charge (all up by more than 2%). The one drag on the index has been Energy, down 2.4% and where benchmark oil prices are off around $2.60 for both Brent and WTI – this after prices rose last Thursday on news that while OPEC+ had agreed to increase production from next month, it will not be by much. Demand side consideration, given Europe’s covid news, seems to be back to the fore overnight.

US 10 year Treasuries hit a new YTD high of 1.775% last Tuesday in front of the US data deluge, but are currently 7bp down on this at 1.7050. Evidently there is no rush to price in an earlier than previously expected commencement of Fed tightening on the strength of the data (again this was the message from the Fed’s Mester just now, someone traditionally seen as a ‘hawk’).

The story in FX seems to be one of positive risk sentiment being associated with USD slippage, but where the absence of further rise in US bond yield – indeed falls – also looks to be relevant. The BBDXY index is currently about a percent down on its new YTD high hit on March 31. Not even the oil sensitive NOK and CAD are weaker overnight (up 0.3% and 0.4% respectively) while AUD has added just over 0.5% to now be more than 1.5% up on last Thursday’s intraday and year to date low. The NZD turnaround is even more impressive, at about 1.7%

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.