Coming in for landing in a heavy cross wind

Insight

It’s been a fairly quiet session overnight.

https://soundcloud.com/user-291029717/us-cpi-today-all-jabs-are-not-equal?in=user-291029717/sets/the-morning-call

Paradise is a platinum card, Behind the wheel of your car, With your new pair of trainers, Designer clothes, Go on, I’ll have seven of those , And go to ski where it snows, Its bounty sustains us. Credit, In love with the never never, Wish I could get something I really need – The Buzzcocks

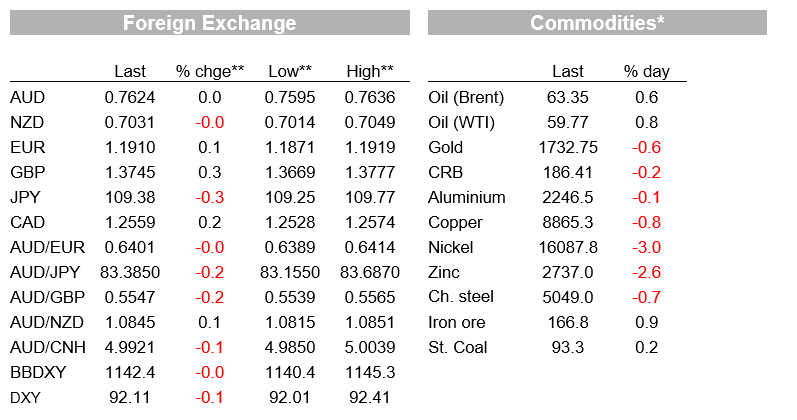

Continuing on from last week, it’s been a fairly quiet start to the new week, in front of US CPI tonight and the US Q1 earnings reporting season that kicks off with three of the major banks on Wednesday. Equities have started the week on the back foot, bonds yield are little changed and the USD is almost flat, with AUD/USD still range bound, currently flat on Friday’s close at 0.7623.

The main piece of economic news since we broke off last night has been the March China credit and money supply data, a release keenly awaited after a recent FT report suggesting that the PBoC had ordered banks to clamp down on lending in light of concerns about an overheating housing market (sound familiar?). In the event, there is nothing to worry about regarding there being sufficient credit and money supply growth to keep the domestic economy bubbling long – and with that support for the global economy. Annual growth of the broad Aggregate Financing measure was up Y3.34tn, so down to a still-strong 12.6%y/y from 12.9% while M2 money supply growth slipped to a still healthy 9.4% from 10.1%. New Yuan Loans rose by a bigger than expected Y2.73tn. See Chart of the Day below.

Other economic news overnight incudes better than expected Eurozone retail sales figures (+3.0% m/m against 1.7% expected) though these are for February so ahead of new lockdowns in France and elsewhere imposed in front of the Easter holidays, and the Bank of Canada’s latest Business Outlook, showing gains in both future sales expectations and the overall outlook. The survey adds to the likelihood that the BoC will announce a tapering of its bond buying programme when it meets next week.

There has been no letup in incoming Fed speak overnight, Boston Fed President Eric Rosengren and St. Louis Fed President James Bullard both on the wires. Bullard often has something original to say and didn’t disappoint last night, suggesting that Fed tapering could be considered when the overall covid vaccination rate in the United States hits 75% (the US is about 40% of the way there at the moment while daily vaccination jumped to a record 4.6 million on Saturday). This is the first time a Fed official has mentioned this as a possible trigger point, with all prior Fed commentary talking only in terms of substantial progress toward its full employment and inflation goals. Rosengren meanwhile suggested that the US could have a tight labour market ‘after two years’ (in contrast to her former boss Janet Yellen’s contention that the $1.9tn recently passed covid stimulus bill could produce full employment by next year).

Talking of Janet Yellen, a source report just in says that The Treasury Secretary will refrain from labelling China a currency manipulator when the next currency report is published (likely Thursday), though recall former Treasury Secretary Steve Mnuchin dropped the label as part of the Phase 1 trade deal at the start of 2020, having imposed it under order from President Trump just five months earlier.

Headlines on COVID19 show a mix of positive and negative reports. On the negative side, further research on China’s Sinovac vaccine being used in Brazil suggested an efficacy result of just above 50%, raising some alarm bells in China and across a number of countries using the vaccine. This can only suggest a longer period ahead to bring the virus under control across much of the developing world. The weekly death toll in the US rose for the first time since February and the infection rate climbed for a fourth straight week. Infection and death rates across India continue to rise at an alarming rate. India’s key share market index saw its gains for the year wiped out yesterday with a 3½% fall, on concerns about India’s economic outlook.

On a positive note, vaccinations in the EU do appear to be ramping up, with some 22% on average of the populations in France, Italy and Germany now having received a first jab. And the Brits have been allowed out to play for the first time in months, in terms of outdoor pub/restaurant visitations and non-essential shops and hairdressers re-opening for business (though my spies tell me it’s way too cold to be sipping even a warm beer outside).

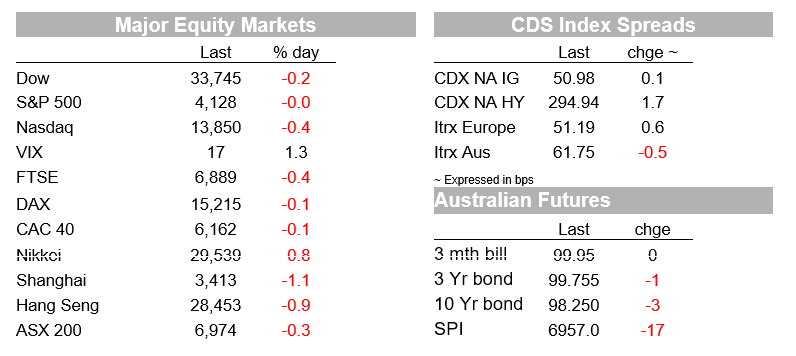

US equity markets have closed with the S&P virtually unchanged (-0.02% and the NASDAQ -0.4%) implying a decent last hour of power rally in the S&P with 8 of the 12 sub-sectors ending in the green (led by Real Estate and Consumer Discretionaries).

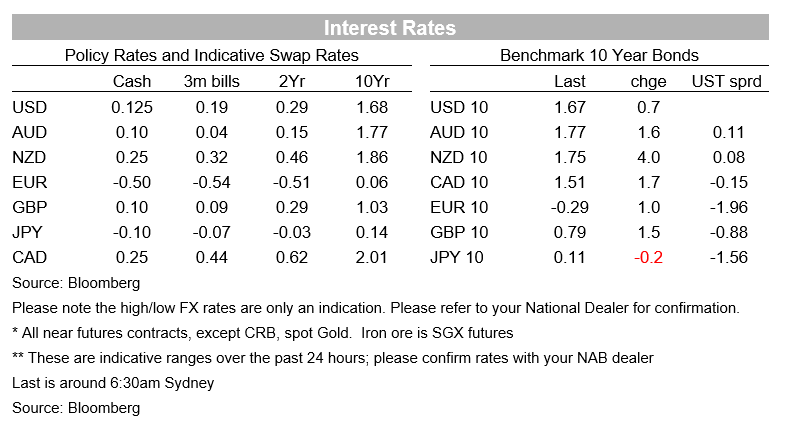

Bond markets don’t show much movement and continue to consolidate comfortably inside recent ranges. The US 10-year Treasury yield has traded a 1.64-1.68% range overnight, currently towards the top end of that range. The $38b 10-year auction went off without any drama, at a rate of 1.68% and demand slightly lower from last month’s auction.

Currency markets have started the week on a mixed but generally quiet note, with the AUD unchanged in Friday’s NY close at 0.7623. GBP, JPY and CHF are all up 0.2-0.3% while CAD and SEK are down 0.3-0.4%, CAD despite the aforementioned positive BoC business survey. The BBDXY index is currently unchanged on the day.

China credit & money supply

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.