On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

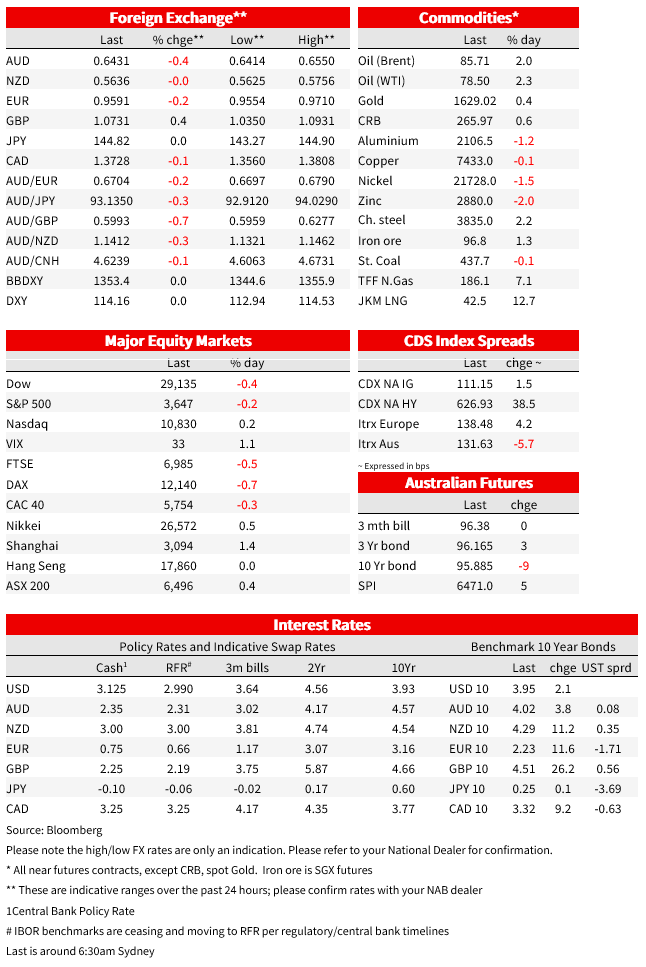

UK rates continue to push higher

A partial reversal of much of yesterday’s price moves and signs of an improving risk appetite over the Asian session couldn’t hold on amid hawkish Fed speak, US data continuing to point to resilience, and as focus remained on the implications of the UK’s fiscal plan.

Yields have generally continued to push higher. The UK again leading the moves, with the 10yr gilt yield up a further 26bp to 4.51%. The 2yr 13bp higher to 4.61%. The BoE’s Chief Economist Pill said that based on Chancellor Kwarteng’s fiscal update “it’s hard not to draw the conclusion that all this will require a significant monetary policy response. ” Pricing for BoE hikes has pushed another 30bp higher to 6.25% by May next year. Pill indicated that the 3 November meeting, alongside updated forecasts was the appropriate time to assess the news and that if market repricing remains orderly, the Bank’s program of government bond sales should go ahead as planned next week. Pill said that the energy price subsidies “freed monetary policy to do its job to address these longer-term dynamics” and said that “I am happy to be unpopular”

Fed speakers continued to sing from their hawkish hymn sheet. St Louis Fed President Bullard said that inflation was a “serious problem” and the credibility of the inflation-targeting regime was at risk. He noted the dot plot that showed the Fed Funds rate heading to a range of 4.5-4.75% next year and said that “I think we need to stay at that higher rate for some time”. Chicago Fed President Evans’ spoke to CNBC and his comments were in line with the official Fed view we heard last week. Neel Kashkari told the WSJ, “ We are moving very aggressively.” US rates traded a large range but the daily moves were smaller. the 10yr is up another 2bp to 3.95%, knocking on the door of 4% overnight, at one point touching 3.99% after earlier falling back to 3.80%. The 2yr is 6bp lower at 4.29%

On the data flow, US data generally came in on the stronger side of expectations , another sign of the US economies stubborn resilience. The Conference Board consumer confidence measure rose more than expected to a five-month high of 108.0, with gains across the expectations and present situation indices and no doubt helped by recent declines in gas prices. New home sales unexpectedly surged 29% in August, an unlikely result that contrasts with other indicators including mortgage application numbers. Durable goods orders data were solid, with core capital goods orders up 1.3% m/m in August vs expectations for a 0.2% rise.

Energy concerns have also renewed as a new disagreement over fuel transit between Russia and Ukraine puts the little gas that’s still flowing to northwest Europe from Moscow through Ukraine at risk. That news added to the news that Swedish and Danish authorities had identified gas leaks the key Nord Stream link and one line of the idled Nord Stream 2 in the Baltic Sea. Dutch front-month gas, the European benchmark, closed 7% higher.

In FX moves, the DXY is up 0.1%, staging a turnaround after sinking as much as 0.7% over the Asian session. The AUD climbed back above 65 cents briefly, reaching an intraday high of 0.6513, but is now 0.4% lower at 0.6431 after hitting an intraday low of 0.6414. The pound traded a wide range, falling from a low of 1.0653 to high of 1.0838, but regaining some ground over the past 24 hours, currently up 0.4% at 1.0729. JPY ended up little changed over the past 24 hours, edging back towards 145 alongside the retracement in the dollar, currently at 104.82.

US equities markets spent much of the day in the green but closed in the red, the S&P500 down 0.2% for its second consecutive lowest close for the year. The S&P is also now down for six days in a row, its longest losing streak since February 2020. The Nasdaq held on for a 0.2% gain.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.