Total spending grew 0.9% in June.

It’s been a mixed session for US equities overnight whilst bonds headed sideways.

https://soundcloud.com/user-291029717/us-dollar-heading-to-2018-lows?in=user-291029717/sets/the-morning-call

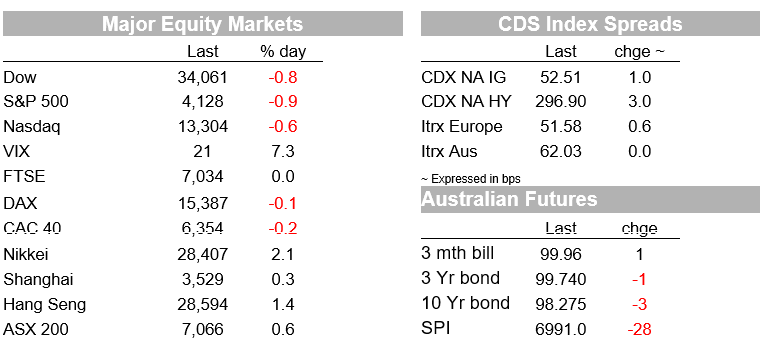

It was mostly an uneventful overnight market, but stocks have taken a step lower later in the session, not helping the case of the USD, the DXY moving down to its lowest level in four months. Oil prices did an about face, earlier supported before heading lower on hopes of a US-Iran nuclear deal. US Treasury yields were mostly little changed, before the 10y Treasury eased a little further to 1.6369%, -1.2bps. Though not quite in the same time sequence, European and UK bond yields were little changed, the 10y bund up 1.2bps to -0.102% and the 10y gilt at 0.868%, +0.3bps.

US equities have taken a turn for the worse in the past hour, the S&P down 0.85% and the Nasdaq down 0.56%, led by energy stocks and falls in some of the tech majors, Facebook -1.7% and 1-1.2% falls in Apple, and Amazon, Alphabet. European equities were little changed, the E600 index up 0.17%, but the E50 index off 0.31%. US homebuilder stocks were down 2.61% in the wake of softer than expected US housing starts for April.

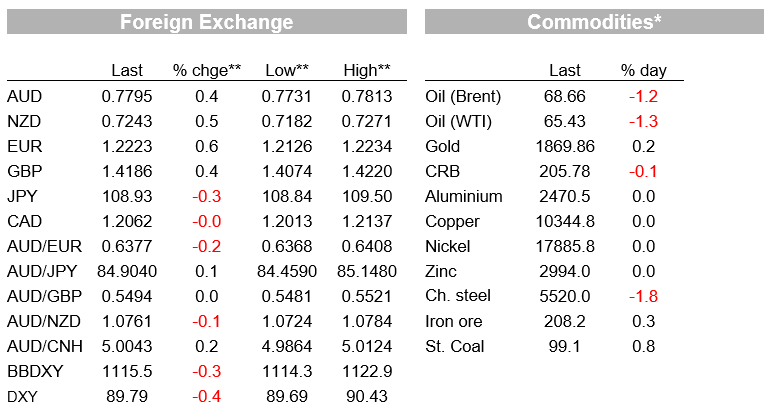

The USD has taken another step lower overnight, the DXY breaking below 90, currently sitting at 89.79, within clear sight of its mid-February 2018 low of 88.25. There was no clear proximate daily trigger (stocks falling more later in the session, the USD soggy throughout), though one Bloomberg writer opined a correlation between vaccinations and currencies over time and that the European program had stepped up another gear recently, supporting the Euro. From the open in London, among the major currencies, the Euro is up 0.5% to 1.2228, cable +0.19% to 1.4192. The AUD and NZD rose by 0.20% and 0.24% respectively, the AUD tracking close to 0.78, the NZD around 0.7250.

Base metal prices rose further, LME copper and nickel up 0.3%, tin popping its head again over $30,000 to $30,455, +1.87%, the best in the base complex. Singapore iron ore futures pulled back after earlier gains but remains north of $200/t at $208.15 having pulled back in recent days on the back of official concern from Chinese officials voiced for several days now over higher commodity prices.

US housing starts and permits came and went without any discernible market rection from the USD and bonds, though it didn’t help the case of US homebuilder stocks. Even though the market tends to focus more on housing starts, that series tells you as much about the weather, and the inevitable lumpiness in starts according to project timetables and capacity. April Starts were down 9.5%, slicing a large piece off the Mar 19.8% m/m gain that rebounded after the bad weather-affected crimped building activity in Feb. April building permits (a closer reflection of demand, if over time) were very close to expectations at 1760K, following on from the large lift in sales during the second half of last year, levels remaining high if choppy into this year.

The pipeline of US resi construction activity still looks quite healthy as builders face into rising costs, incl lumber, notwithstanding timber prices may have peaked for now. Even so, mortgage applications for purchases a more sober outlook than the NAHB housing index that remained high in this week’s report. Following today’s starts data, the Atlanta Fed reduced its Q2 GDPNow estimate to 10.1% from 10.5%, cutting its estimate of Q2 residential investment to 10.6% from 19.2%.

Elsewhere, testifying to the House of Lords, BoE Governor Andrew Bailey and fellow MPC members Ben Broadbent and Dave Ramsden were speaking, their comments on inflation very much in a similar vein to those from most Fed views on the transitory element in the current rise in inflation. Bailey noted that while the BoE is very vigilant on inflationary expectations, the inflation gain is likely due to energy and is temporary. He did say that while it’s useful to have negative rates as a possible tool, the BoE is nowhere near any talk of whether to sue negative rates. EURGBP has been somewhat higher in the aftermath of these comments. .

In the overnight GDT dairy auction, the price index was little changed at -0.2%, sustaining the high level of prices, up about 42% y/y. Last week our BNZ colleagues lifted their milk price forecast slightly to $7.80 per kg/milk solids for farmers and noted that little change in product prices and the NZD from here would translate into a $9 payout for next season – not a forecast, but an indication of the current strength of the dairy market and the “cheapness” of the NZD against a very strong terms of trade backdrop, not dissimilar to the AUD right now.

As my BNZ colleague Jason Wong has already noted this morning, oil prices moved higher initially, Brent crude breaking up through USD70/bbl before selling emerged, prices pulling back after the BBC reported the Russian envoy in Vienna saying that significant progress had been made in efforts to broker an agreement between Iran and the US to revive the 2015 nuclear deal. A positive outcome here would the pave the way for increased oil supply from Iran – the best-case scenario (for oil production, not prices) would be an increase in 4m barrels a day from Iran within three months.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.