Markets Today: US dollar rises as Powell stays put

Ahead of a speech by President Biden later today on the economy and inflation, we got news that Jay Powell is to be re-appointed to a second term as Fed chair.

Powell to be reappointed to 2nd term as Fed chair, Brainard to replace Clarida as Fed VC

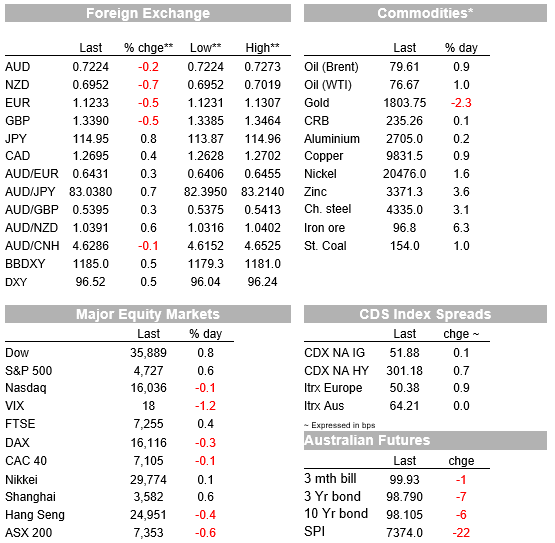

US yields shift materially higher, USD to highest since July 2020, S&P up but NASDAQ down

US data stronger than expected, EZ consumer confidence takes fresh covid-related hit

AUD (>72) resisting the lure of stronger USD as borders set to re-open, unlike NZD (<70)

China about to loosen the monetary spigots

Coming up today: ‘Flash’ UK, EZ, US Markit PMIs; BoE speakers

The only way is up, baby, For you and me now, The only way is up, baby, For you and me now – Yazz

News of the re-appointment of Jay Powell to a second term as Fed chair has seen a fairly level shift up in the US Treasury yield curve, by 6-7bps, and the USD rise almost 0.5% to its highest since July 2020. The S&P 500 (+0.4%) has taken the news in its stride in contrast to the NASDAQ (-0.4%) where higher rates look to have taken a bigger toll on the sector than the support drawn for ‘stay-at-home stocks’ from last Fridays’ lockdown news in Austria and the prospect this will extend to more European economies before much longer – quite possibly including Germany where the hospital system is being overwhelmed.

Ahead of a speech by President Biden later today on the economy and inflation, we got news that Jay Powell is to be re-appointed to a second term as Fed chair and that the only other candidate for the job, Fed Governor Lael Brainard, is to be elevated to the role of Fed vice chair – a position currently held by Richard Clarida (and who recently came under fire for stock trading activity, albeit not deemed to have done anything wrong). Clarida of late has sounded more hawkish than other FOMC heavy hitters, so arguably this a ‘dovish tilt’ of sorts in terms of the Fed make-up, while there will now be three vacancies on the Fed Board which Biden says he will move to quickly fill (he mentions December for nominations) with diversity to be one key consideration.

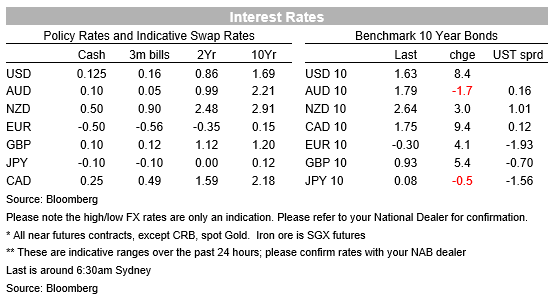

That the US government bond market has reacted the way it has, with 2 and 10-year yields both up a little over 7 basis points, reveals that market rightly or wrongly (most likely wrongly) had applied a bit of a discount to yields against the risk of Brainard getting the nod for the Fed chair. Our view has been that whether Powell or Brainard, it wouldn’t make a heap of difference for a mandate-constrained Fed. The fact is though that the front end of the US curve is now closer to pricing three quarter-point rate rises next year, from two a week or so ago. In this respect though, the comments last Friday from Fed Governors Waller and Clarida suggesting the need to accelerate the pace of QE tapering – which would only makes sense if the Fed wanted the option of lifting rates as early as Q2 2022 – has continued to reverberate (e.g. some of Monday’s lift in 2-year yields occurred during the Tokyo session yesterday, ahead of the Powell re-appointment news)..

Playing to the grain of higher yields (and a stronger S&P) overnight has been better-than-expected US economic news, in the form of Existing Home Sales rising to a 9-month high of 6.34mn in October, above the 6.2mn expected and 6.29mn last time. In contrast, Eurozone November consumer confidence fell by more than expected, to -6.8 from -4.8 previously and -5.5 expected.

The contrasting fortunes of incoming US and Eurozone economic news is expected to be further exemplified in tonight’s ‘flash’ PMI data (see ‘Coming Up’ below) and is currently a key driver of the (EUR-led) strengthening in the USD. The DXY index (57.6% weighted to EUR/USD) is up by exactly 0.5% on last Friday’s New York close to 96.5, its highest since July 13 2020. NAB’s FX strategists back in early September suggested that DXY could now trade within a broad 92-97 range, and there looks to be every prospect of the top of that range being tested in coming days and weeks. It will likely some better news out of Europe to prevent it, and it is hard to see where that comes from just at the moment.

That said, one glimmer of hope comes from the PBoC’s late quarterly Monetary Policy Review, which appears to hint that some form of monetary policy easing is in the wings. Reading the PBoC’s runes is often about seeing what they don’t say than what they do, in which respect this latest report omits references to sticking with “normal monetary policy” to “control the valve on money supply” or vowing not to “flood the economy with stimulus.”

Quite what form earlier monetary policy will take is uncertain, though given that over the weekend the PBoC’s issued some directives in regards to FX trading suggesting they are getting uneasy about the strength of the Yuan, then lower interest rates (rather than further cut(s) to RRRs) might be a strong candidate, aimed at diminishing the attraction of long Yuan ‘carry trades’ (though of course, that could just lead to more capital inflows in the short term as foreign investors seek to take advantage of a rallying Chinese government bond market).

So, while EUR/USD is one of the poorest performing G10 currencies overnight (down 0.5% to a low of 1.1231) the Japanese Yen is weaker still, consist with its high beta to US Treasury yield, USD/JPY back testing Y115 (high of Y114.92, up 0.8% on the day). AUD in contrast was the top performer yesterday during our local session and while it has given back 20-30 pips offshore, is currently little changed on Friday’s NY close.

Of some assistance to AUD was news yesterday that Au stralia will open its international border to fully vaccinated skilled workers and students from the start of December. The government has re-opened the country to a backlog of up to 235k overseas visa holders. The vast majority of the 235,000 of overseas visa holders who may be eligible to enter Australia after December 1 are 162,000 foreign students while another 57,400 are skilled workers. If they are fully vaccinated and test negative 72 hours before entry, the arrivals will not need a travel exemption to enter participating states. In addition to the above, vaccinated travellers from Japan and South Korea will join Singaporeans in being allowed to enter. We caution that the news is not necessarily all good, in so far as border restrictions will still be applicable in QLD, WA and SA, plus we might now expect to see more young Australian’s travelling abroad to work. So how this plays out in terms of easing upward pressure on wages as we go through next year (with implications for monetary policy) remains to be seen.

Coming Up

It’s ‘flash’ (preliminary) November Markit PMI day and where the focus will be on whether or not we are seeing further divergence between US (rising) and Eurozone (falling) readings. Have sharply rising covid case numbers across swathes of (mostly northern) Europe impacted firms ahead of new restrictions only now coming into place? And in the case of Manufacturing PMIs, whether or not China’s slowdown is having negative impact on export sectors (in Germany in particular). Every reading, whether for Germany, France or pan-Eurozone and whether for Services or Manufacturing, is expected to be down on October, with the pan-Eurozone Composite seen at 53.0 from 54.2. In contrast, US readings are seen up on last month from October levels already well above Eurozone equivalents – to 59.1 from 58.4 for manufacturing and to 59.0 from 58.7 for services.

The UK PMIs are also seen down a touch on October but from much more elevated levels more comparable to the US (i.e. closer to 60). Also in the UK are no less than three BoE speakers ahead of what is a highly uncertain MPC decision next week, though Governor Bailey and Deputy Governor Cunliffe testimonies to a House of Lords Committee are on central bank digital currencies. Of greater interest therefore will MPC member Jonathon Haskel speaking on ‘high inflation now and then’.

Locally, NZ Q3 real retail sales will show the hit to activity from covid lockdowns, with a double digits fall expected (-10.5%).

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.