Online retail sales growth slowed in May following a fairly strong April

Insight

A distinctly cautious air prevails in front of tonight’s all-important US CPI release and tomorrow’s FOMC.

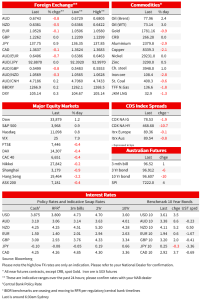

You wouldn’t’ know if looking at the current ‘change on the day’ for all the main US stock indices coming into the last hour of NYSE trade (currently up by 0.7-1.0%) but a distinctly cautious air prevails in front to tonight’s all-important US CPI release and tomorrow’s FOMC. The VIX is up 2 points to around 24.5, its highest level since 17 November, the USD is firmer (DXY +0.33%) And AUD/USd is the worst performing G10 currency so far this week, currently off 0.9% and back nearer 0.67 than 0.68. US bond yields are higher, front-end led but not helped by a poorly received US 10-year note auction which tailed almost 4bps above its pre-auction yield. China credit data overnight underwhelmed expectations and together with news of surging covid-related hospitalisations, confirms that optimism regarding the impact of the shift away from the ‘dynamic’ zero covid strategy will bring bad economic (and health) news before the good.

One explanation on offer for the better showing by US (cash) equities in front of CPI tonight and the Fed tomorrow is the latest New York Fed survey of consumer inflation expectations , showing a fall-back from 5.7% to 5.2% on a 12-month horizon. To what extent this simply reflects falling gasoline prices (off about 25 cents a gallon so far in December and over 50 cents in the past month) is unclear, or the fact inflation fell back in October. Whatever, it is getting a lot of mention on the wires in attempting to explain higher stocks on a day when there is no other economic news on offer. But then the 24-hour business news channels always have to have a fundamental explanation for everything. Sometimes there are just more buyers than sellers, or vice versa.

Let’s see what CPI brings tonight, but in the meantime the WSJ’s venerable Fed watcher Nick Timiraos has penned a new piece overnight in which he notes that Fed officials are divided over how long the Fed should keep raising rates , noting “cracks are beginning to emerge among them (Fed officials) over how stubborn inflation has become and what they should do about it”. He goes on, “Some expect inflation to cool steadily next year and want to stop raising rates soon. Others worry inflation won’t ease enough next year, a scenario that calls for raising rates higher or holding them at that level for longer, boosting the chance of a sharp downturn”. In this light, don’t expect clear cut signals from the Fed on Wednesday night/Thursday morning on what they expect to be doing at early 2023 FOMC meetings after a widely expected 50bps Fund rate hike this week.

Gains for US cash equities (and futures) contrast with a rise in the VIX index, implying increased demand for downside protection against a near term fall-back in the S&P500, up 2-points at the open to about 24.5 and staying there (to its highest level since November 17). Bond markets, meanwhile, mid-way through the afternoon US session, are exhibiting more (bearish) curve flattening, The 2-year note is currently up 6bps on the day and 10s just under 4bps. The latter follows a poorly received 10-year Note auction (but for which timing perhaps could not have been worse), clearing some 4bps above the prevailing (When-Issued) yield (the biggest ‘tail’ since December 2009) a relatively low 2.31 bid-cover ratio and the Street having to take down more than half the Notes on offer. The 10-year yield of just above 3.60% is more than 20bps up on its 3.40% recent low in the middle of last week.

Other economic news of note overnight Is latest China credit and money supply data for November. These show CNY bank loans expanding by a less than expected 1,210bn (1,350bn consensus) and the widest Aggregate Financing measure by ¥1.990bn (2,100bn expected) with weak household demand the key feature in the face of stronger corporate demand (latter most probably to better rated property developers). Bank loan growth is down to 11.0% in the last year from 11.1% and Aggregate Financing to 10.0% from 10.3% (marking a return to a 15-year low last seen in 2021). And, while annual M2 money supply growth jumped to 12.4% from 11.8%, this most likely reflects households parking cash in savings accounts that would otherwise have gone to finance mortgage payments on house purchases.

We’ve also had a slug of better than – or less-worse than – expected UK data , including monthly (October) GDP of 0.5% against the 0.4% consensus (3m3/m -0.3% vs -0.4% expected), Manufacturing production +0.7% against -0.1% and Construction output +0.8% against -0.1% expected. This might help explain why GBP is (once again) one of the top performing G10 currencies overnight. Indeed, together with CAD, which has drawn some support from a +/-$2 jump in benchmark crude oil prices, GBP is one of only two G10 currencies not to have lost ground against a generally firmer USD (DXY index currently up one-third of a percent).

USD/JPY (+0.9% on higher US Treasury yields) and AUD (-0.8%) to a low of 0.6729 are currently vying for the wooden spoon. Of some note on the latter, USD/CNH is back looking up at 7.0 (6.99) having been below 6.95 last week. Here, the worsening health and current economic news is now pushing back somewhat against the exuberance evident in the past few weeks on the evidence of China beating the retreat on its hitherto zero covid stance.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.