Firmer consumer and steady outlook

Insight

Since Australia Day the two biggest pieces of news were the BoC explicitly signalling a pause to the hiking cycle on Wednesday after hiking by 25bps, and US Q4 GDP which although beating expectations had a soft underbelly (2.9% annualised vs. 2.6% expected; but private domestic just 0.2%).

“You’re the voice, try and understand it; Make a noise and make it clear; Oh, whoa”, John Farnham, 1985

The BoC’s explicit pause signal has many thinking whether other central banks will do likewise – note BoC was one of the first to start the initial hiking cycle. There has also been extensive media coverage of Wednesday’s Aussie CPI figures in the press with the AFR’s RBA whisperer Kehoe opining this firms up hikes for February and March (as is NAB’s view). Also in the media is more signs of the Australia-China relationship on the mend with President Xi saying it is proceeding in “the right direction”. Risk sentiment has been positive with US equities supported by earnings (Tesla and Chevron) and the S&P500 was flat on Wednesday and into today’s last hour of power is up 0.7%.

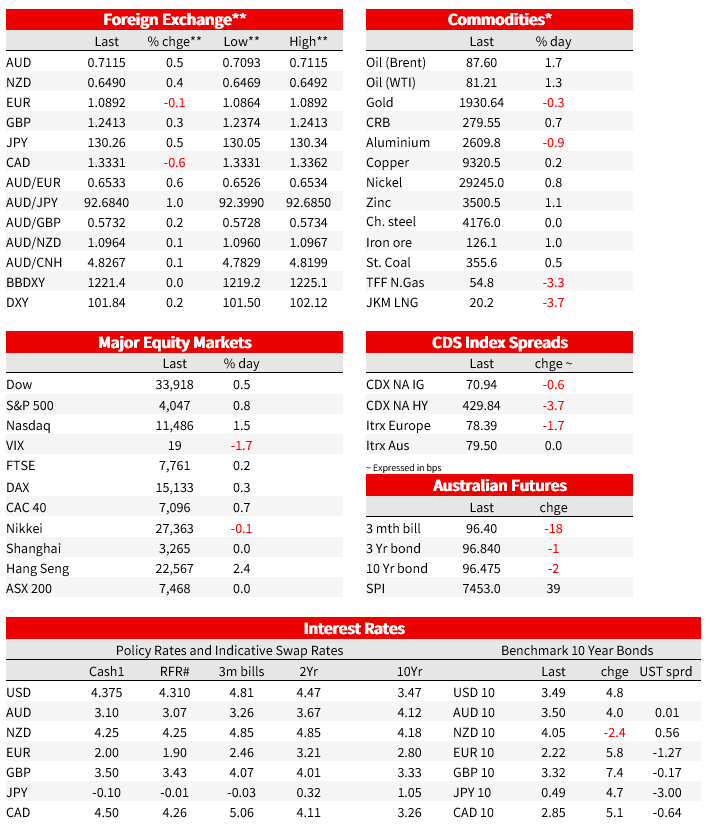

Yields are broadly flat since Wednesday, though overnight they did rise on US data headlines with the US 10yr +4.4bps at 3.49%; ditto the 2 year. Fed Funds pricing is also little changed with a peak of around 4.91% priced by June 2023 and still 47bps worth of cuts in H2 2023. North of the border in Canada, the market now sees the BoC is largely done, pricing in only a 20% chance of another 25bp hike by June and then 59.6bps worth of cuts in H2 2023. The USD (DXY) is also little changed since Wednesday at 101.87, though is up 0.2% overnight in sync with higher yields. The AUD has held onto its post-CPI gains and trades at 0.7113; a spike in the oil price (Brent +1.6% to $87.54) supported commodity currencies overnight (USD/CAD ‑0.5% to 1.3339: AUD +0.4%). That spike in oil coming from both stronger US data, and positive demand out of China. USD/JPY (+0.5% to 130.24) was the weak one overnight given the rise in yields.

First to US Q4 GDP which beat expectations at 2.9% quarter annualised vs. 2.6% expected. There was though a soft underbelly to the report with final sales to private domestic purchasers, cooling to a 0.2% annual pace in Q4, from 1.1% in Q3. Around half of the overall rise in GDP came from building inventories (adding 1.5pts to growth) and from trade from a fall in imports (adding 0.6pts). Consumer spending was the main engine of growth although continued to show slower momentum (+2.1%), residential investment remained in a deep hole (-26.7%) and business investment remained sluggish (+0.7%). The GDP figures also contained the Fed’s preferred inflation gauge of Core PCE which rose as expected by 3.9% in Q4. Tonight the monthly PCE figures come out for December with today’s data implying a 0.28% m/m rise the core PCE deflator, in line with the consensus.

There was also plenty of second tier US data with Jobless Claims lower-than expected at 186k vs. 205k expected. At first blush that would suggest a still very tight labour market, though announced layoffs do suggest this should start ticking higher and Continuing Claims did rise more than expected to 1675k vs. 1658k expected. Overnight there were more announced layoffs happening from IBM, SAP and DOW, totalling more 10,000k (see WSJ: Corporate Layoffs Spread Beyond High-Growth Tech Giants for details). This spread of layoffs outside of tech is potentially important given firms had been holding onto workers after struggling to hire and retain them during the pandemic. Core durable orders excluding transportation was broadly soft as expected at -0.1% m/m, though including civilian aircraft orders rose a stronger than expected 5.6% vs. 2.5% expected. The Goods Trade Balance was weaker than expected at -90.3bn vs. 87.9bn.

The Bank of Canada (BoC) signalled a pause ahead after hiking by 25bps to 4.50% on Wednesday. The BoC said any pause would be ‘conditional on economic developments’ unfolding as anticipated and here the BoC forecasts inflation falling to 3.6% in 2023 and 2.3% in 2024 (note the BoC targets inflation at the 2% midpoint of the 1%–3% range). Governor Macklem gave further details on the conditionality of the pause: “ …we expect to pause rate hikes while we assess the impacts of the substantial monetary policy tightening already undertaken. To be clear, this is a conditional pause—it is conditional on economic developments evolving broadly in line with our MPR outlook. If we need to do more to get inflation to the 2% target, we will. We are trying to balance the risks of under-and-over-tightening. If we do too little, the decline in inflation will stall before we get back to target. But if we do too much, we will make the adjustment unnecessarily painful and undershoot the inflation target.” (see: BoC: Monetary Policy Report Press Conference Opening Statement and BoC Monetary Policy Report for details).

In Australia, the AFR’s RBA whisperer Kehoe states the most recent CPI figures locks in hikes for February and March: “The bottom line is that the Reserve Bank of Australia will be concerned that its preferred measure of underlying inflation – which strips out some volatile items – was above its most recent forecast issued in November. Inflation may have peaked, but the RBA will have more interest rate work to do in February and March to take the cash rate to 3.6 per cent, and possibly beyond thereafter, to get inflation back towards its 2 per cent to 3 per cent target.” (see AFR: Why the RBA won’t like the latest inflation figures ). The key figures from here will be the WPI on 22 February and National Accounts on 1 March to assess whether wages growth is still consistent with inflation returning to the 2-3% target range. Thereafter it will be Retail Sales for January on 28 February (note December numbers will be hard to read given shifting seasonality) and Labour Force on 18 February to assess the yet to be seen activity impact from the significant monetary tightening seen to date. NAB’s view remains that the RBA will hike rates by 25bps in February and March, taking the cash rate to 3.60%, and then pause thereafter.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.