Online retail sales growth slowed in May following a fairly strong April

Insight

Not too good, not too bad, that seems to have been the market response to the non-farm payrolls numbers out of the US on Friday.

https://soundcloud.com/user-291029717/us-jobs-numbers-hit-the-sweet-spot?in=user-291029717/sets/the-morning-call

Oh, that’s the way, uh-huh uh-huh

I like it, uh-huh, uh-huh – KC & The Sunshine Band

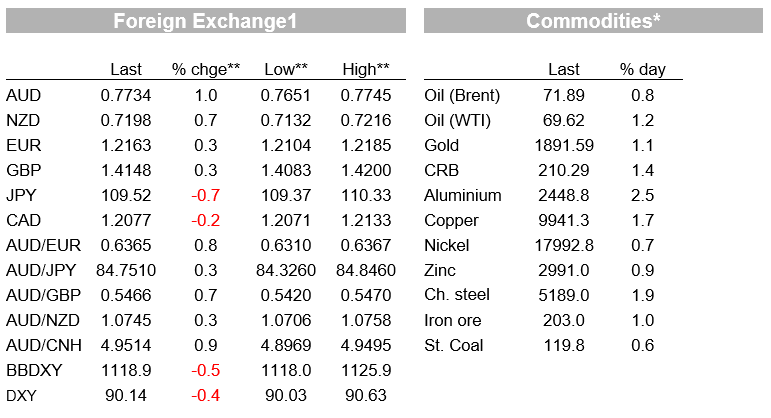

US equities ended the week on a positive note with the tech heavy NASDAQ index leading the way. US labour market data delivered the ideal outcome for risk assets, the labour market is improving but not fast enough to instigate an imminent need for the Fed to start talking about QE tapering. Shortage of US workers has also resulted in an increase hourly wages, adding to inflation worries. The data triggered a sharp decline in UST yields from the 5 to 30y part of the curve and the USD was broadly weaker given the combo of lower yields and improved risk appetite. AUD and NZD were the outperformers with the AUD reversing the strong ADP induced technical damage, closing the week back above 77c.

After the solid ADP employment print, the market was gearing up for a strong US nonfarm payrolls report and in the end the report was not too strong to instigate Fed tapering talk, but strong enough to suggest the US labour market remains on a strong recovery path. The May nonfarm payrolls printed at 559k, below the consensus, 675k and much lower than the whisper number (+750k to 1m) following the big 978k ADP print on Thursday. Revisions to the April number was a trivial +27k but looking through the volatility of the monthly numbers, there has been a steady rise in the 3 month nonfarm payrolls moving average, now at 541k, a lot higher than a few month ago ( January’s 3MA was 67k and March was 518k).

The unemployment rate, meanwhile, fell by 0.3 percentage point to 5.8%, but remained well above the pre-pandemic level of 3.5% and the average hourly earnings rose 0.5%mom well above the 0.2% expected by the market. The increase in hourly wages reflect the current supply constraints in the US labour market with the monthly uptick largely coming from a rise in average wages within the leisure and hospitality sector, up 7% relative to pre pandemic levels and up 12% in annualised terms over the past six months.

Employers are having to pay up in order to attract workers, but the thinking here is that the current labour supply shortage is largely driven by factors that are likely to fade over the coming months . For one the enhanced unemployment benefits officially end in September, but we know there are 25 states that will be stopping these benefits over coming weeks. There is also the issue of childcares and schools not being fully open because of covid, making it very difficult for both moms and dads to go to work, these facilities are also expected to fully open over coming weeks. Finally, covid is still a concern making many workers apprehensive, but here is were the vaccine rollout is expected to alleviate these anxieties and allow workers to get back to work.

The conclusion for markets and the Fed is that only time will help resolve these uncertainties, playing to the view that markets are likely to remain range bound until we know more . Some like Harvard professor Jason Furman and Harvard Kennedy School research associate Wilson Powell believe the “realistic” unemployment rate, which adjusts for the unusually large reduction in labour force participation, was 7.3% in May, over 1.5% higher than the official reading. Others point out that there are about 9m job adds in the US and about 9m unemployed, this mismatch needs time to resolve, but when it does it will reveal a much tighter labour market with potentially much higher wages, which again may instigate concern over higher inflation. But for now we just need to wait and see how it all plays out.

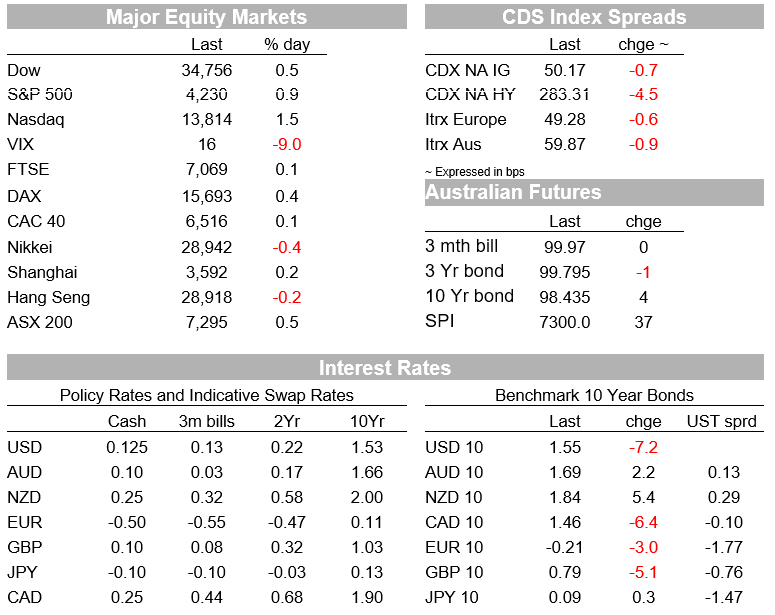

Moving onto markets, the not so hot not so strong US labour data release was the perfect antidote for the US equity market. The data release helped reversed Thursday’s losses and added a little bit more gains on top of that, main US equity indices not only ended the day but also the week in positive territory. After falling 1% on Thursday, the NASDAQ led the gains on Friday climbing 1.5% on the day and closing the week +0.57%, no doubt the mover in UST yields (more below), helping the rebound in the tech heavy index. The S&P gained 0.88% on Friday and closed the week close to its all time high at 4229.89, up 0.69% on the week. Japan’s Nikkei was the big underperformer last week, but the solid lead from the US suggest Japan is likely to enjoy a positive start to the new week. Of note too, NZ and AU equities were the outperformers last week up 2.58% and 1.61% respectively.

Moving onto the rates markets, the US labour market data triggered a decent decline in UST yields over the 5 to 30y part of the curve. After the solid ADP number on Thursday it seem the rates market was gearing up for a solid nonfarm payrolls print, the softer number triggered a bid and then the break of some support levels accelerated the move on the back of some short covering. 10y UST yields were trading around 1.635% before the data release and ended the day at 1.5534%, close to the bottom of the 1.50% to 1.75% range that has largely contained the benchmark yield since early March. The UST curve bull flattened on the week with the 30y Bond down 5bps, closing the week at 2.23%.

The USD lost ground after the US data release, hit by a combo of lower UST yields and improved risk appetite . The USD fell around 0.45% in index term, leaving both the BBDXY and DXY indices essentially unchanged on the week and closer to the bottom of recent ranges. Within G10 the AUD and NZD were the big performers on Friday, up 1.06% and 0.96% respectively. The AUD starts the new week at 0.7736 and NZD is at 0.7198. After the ADP report on Thursday, the AUD fell to low of 0.7646 and in the process, it broke below its 0.7675 to 0.7891 range held since early March, Thursday’s technical damage increased the prospect for the pair to trade lower, but Friday’s recovery now leaves the AUD more comfortable and like my UK colleague Gavin Friend remarked, the AUD starts the week within its old range and lives to fight another day.

CAD was the notable underperformer on Friday, up just 0.19% against the USD . Canda’s labour report was a bit softer than expected with a decline of 68k jobs vs -22k expected. The BoC meets this week and no change in policy setting is expected. The Ontario lockdown was the big factor affecting the labour data and there is sense the numbers should improve next month.

Looking at commodities, it was a positive end across to broad excluding lead while Copper and Aluminium led the charge. On the week steam coal was the big winner with copper the big underperform, down just over 3%.

Early on Saturday, the G7 agreed that businesses should pay a minimum tax rate of at least 15% in each of the countries in which they operate. There are still significant details to be worked and importantly to make this new tax a global standard G20 nations also need to agree, making the G-20 meeting in Venice on July 9-10 the one to watch.

Speaking to Bloomberg Fed Mester said the Fed should be “deliberately patient” and wait to see more evidence that the US labor market has made more progress before they consider cutting down their asset-purchase program.

Overnight Treasury Secretary Janet Yellen said that President Joe Biden’s $4 trillion spending plan would be good for the US even if it contributes to rising inflation and results in higher interest rates . “We’ve been fighting inflation that’s too low and interest rates that are too low now for a decade,” the former Federal Reserve chair said, adding that “we want them to go back to” a normal interest rate environment, “and if this helps a little bit to alleviate things then that’s not a bad thing — that’s a good thing.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.