Total spending grew 0.9% in June.

US economy brushes Omicron aside with a strong January Labour market report

In the words of Shaggy, the January US nonfarm payrolls report was nothing but Boombastic! In addition to the much better than expected January print of 467K new jobs vs a consensus of 125k and a very wide range of estimates from -400k to +250k, the release also revealed net revision to the previous three months of an additional 709K new jobs, amazing! After the ECB tilt on Thursday, the strong US labour report saw core global yields extend their ascendency on Friday with the 10y UST yield closing the week above 1.90% while the 2y rate climbed up 12bps to 1.13%. European equities were a sea of red while US stock ended the week on a high with Amazon leading the charge. The USD was broadly stronger on Friday, but still lower on the week, the euro retained its post ECB gains while NOK and AUD were the main underperformers with the latter starting the new week below 71c. Commodities had a positive Friday and a solid week with both WTI and Brent closing the week above $90.

Looking at the details of the report, the US Labor Department noted that payrolls might have been even stronger if not for the surge in Omicron cases with nearly 2m workers unable to look for work last month because of the pandemic. While some analysts have highlighted the sharp declines in high frequency data over January could imply some payback will be due in February, overall it is hard to disagree with the assessment that the US economy and its labour market are currently exhibiting big resilience and strong momentum.

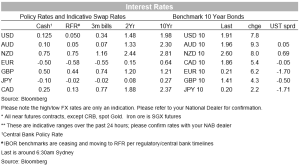

The US unemployment rate rose by a tenth to 4.0%, above the consensus of 3.9% while average hourly earnings rose 0.7%mom vs 0.5% expected by economists. On a y/y basis wage growth jumped to 5.7%, but the last three-month annualized rate was an astonishing 7.7%. This acceleration in wages growth is not sustainable and if it is corroborated by upcoming labour market data releases, FOMC officials will be emboldened to accelerate their expected pace of rate hikes over 2022. The market is now back towing with the idea of five Fed fund rate hikes in 2022, pricing and end of the year rate of 1.43%, up 12bps from Thursday.

Of some significance as well, the increase in the unemployment rate was attributed to a rise in labour force participation, by a statistically significant 0.28%, to 62.2 %. This increase was bigger among women, rising more than three times faster than men’s over the past year, the re-opening of schools and childcare likely factors helping women back into the labour market. Ian Shepherdson, Pantheon chief economist, noted that if participation continues to rise at this pace, the Fed will become more confident that wage growth will moderate as excess labour demand diminishes. But this won’t happen overnight.

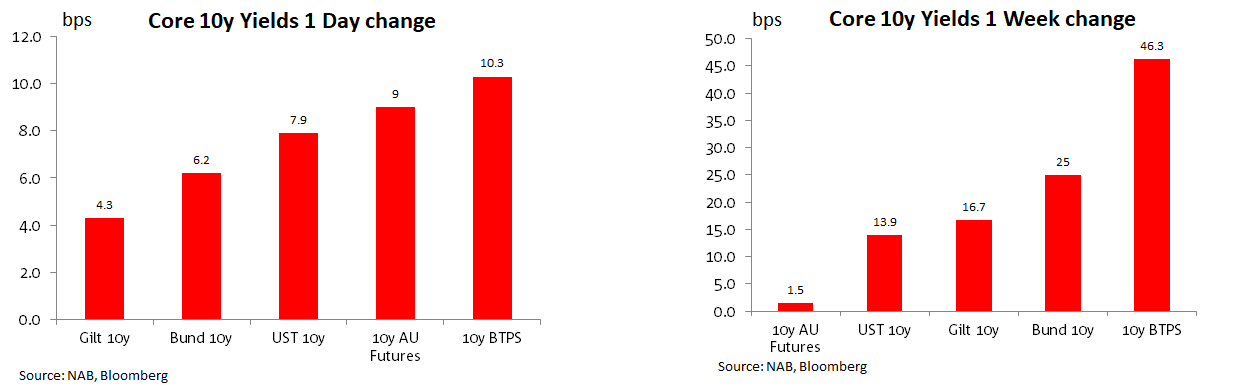

Moving on to markets, the strong US labour report contributed to an extension in the rise of core global bond yields that had begun post the ECB meeting on Thursday. 10y German Bunds rose another 6bps on Friday, closing the week at 0.2% while 10y Italian BTPS gained 10bps on the day with an eye watering increase of 46bps for the week to 1.7430%. 10y UST yields closed the week at 1.9085%, up 8bps on the day, after trading to an intraday high of 1.9338%, a level not seen since December 2019. 2y UST yields rose 12bps on Friday, to 1.313%, flattening the curve. On the week, the 5y tenor recorded the biggest rise in UST yields, up 16bps to 1.77%.

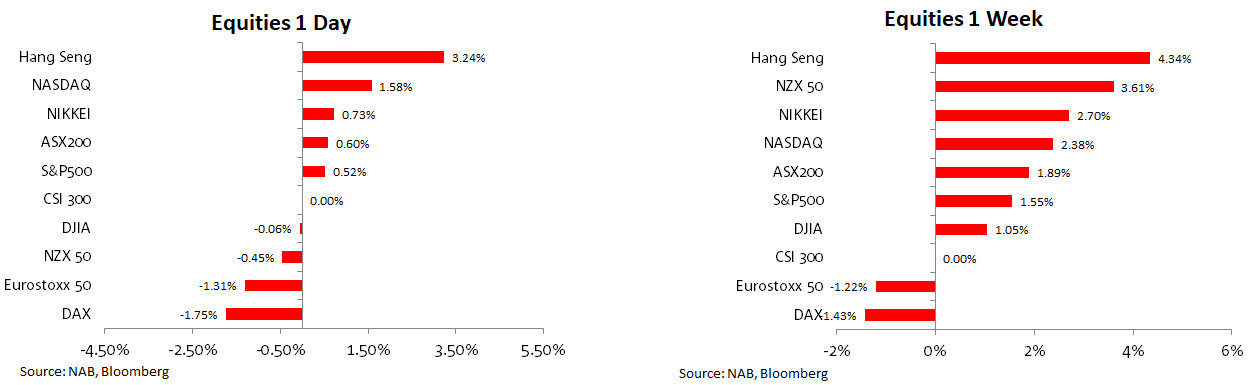

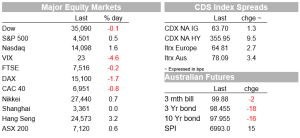

European and US equities had contrasting fortunes on Friday with the former still adjusting to the ECB hawkish tilt in the previous day while the latter ended a volatile week on a positive note with both the NASDAQ and S&P 500 closing the week in the green . The surge in European yields alongside ECB hawkish rhetoric saw European equities erase their weekly gains on Friday with Stoxx 600 Europe Index falling 1.38% by the close. The index has yet to record a positive week in 2022, its longest losing streak since March 2020. Meanwhile in the US the S&P 500 climbed 0.52% on Friday and 1.55% on the week, its best weekly gain since late December. The NASDAQ gained 1.58% on Friday and 2.38% on the week with the Dow the odd one out, down 0.06% on the day and -0.24% on the week. Amazon led the charge within US equities on Friday, after posting a strong quarter and announcing a price hike to its Prime membership. The Hang Seng had a solid return from holiday, up 3.24% on Friday and our S&P/ASX 200 gained 1.89% on the week.

Although US equities had a broadly positive week, gains were obtained in a volatile environment with the VIX index climbing to 26 before ending the week at 23 . It was a week of contrasting fortunes for many companies, Google parent Alphabet and Snap enjoyed extra-large gains, while others including Meta Platforms (Facebook) and PayPal got severely punished, after reporting underwhelming numbers. Amazon is another great example of the volatile environment, tumbling 7.8% ahead of its results on Thursday, only to surge 14% on Friday after positive reporting news.

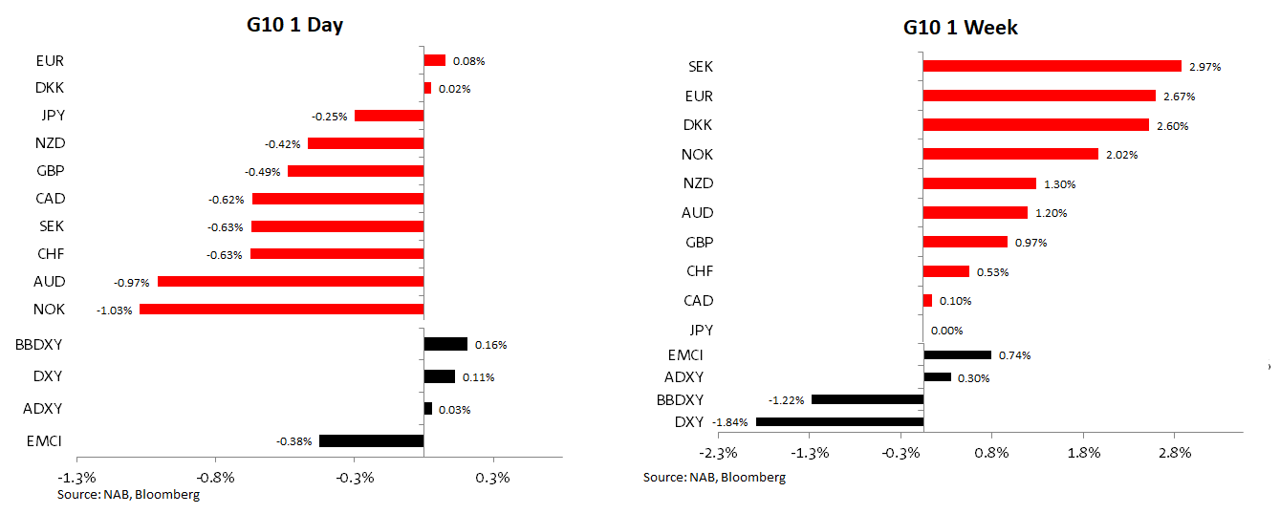

The USD was broadly stronger on Friday, but still lower on the week with the DXY index down 1.84% over the past five days and now testing the uptrend line support that has been in place since May last year. The euro retained its post ECB gains closing the week at 1.1463 while NOK and AUD were the main underperformers on Friday, falling 1.03% and 0.97% respectively. The AUD starts the new week at 0.7081, up 1.2% on the week. The rise in core global yields also included gains for AU rates with gains in commodities also supportive for the AUD.

The kiwi starts the new week at 0.6610, after losing 0.42% on Friday but gaining 1.30% on the week, the NZD remains unable to trade above 67c so far in February. CAD was little changed on Friday and down 0.29% on the week, Canada’s January labour market report was a big miss, unemployment rate jumped to 6.5% from 6%, and employment dropped by 200k, more than most economists were expecting. The surprise fall was attributed to the provincial governments reintroduction of restrictions aimed at limiting the spread the Omicron over the start of the new year.

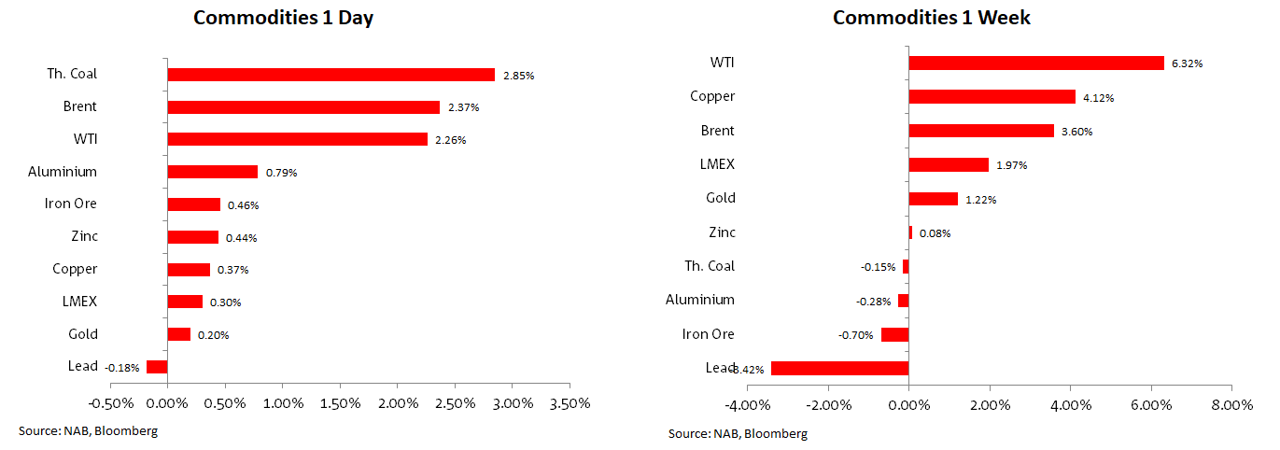

Commodities had a positive Friday and a solid week with both WTI and Brent closing the week above $90 .Copper was the other notable performer on the week ( up over 4%) with metal prices also eking out gains on the week while iron ore was little changed at $ 145.

In other news, overseas tourists could be back in Australia within two or three weeks , Australian media reported over the weekend and also suggested a government announcement could be made as soon as today. The news would be a positive outcome for the tourist industry and may also contribute to an increase in labour supply if backpacker come back in mass.

China and Russia declared a “no limits” partnership, backing each other over respective Taiwan and Ukraine tensions with the West , promising to collaborate more with each other and present a united front against the West. On a more positive note, French president Emmanuel Macron claimed that his negotiations with Russia are likely to avoid a military conflict, ahead of his visit to Moscow this week.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.