Long-term signal vs. Short-term noise

Insight

Solid US PPI cements apprehension ahead of the US CPI & FOMC

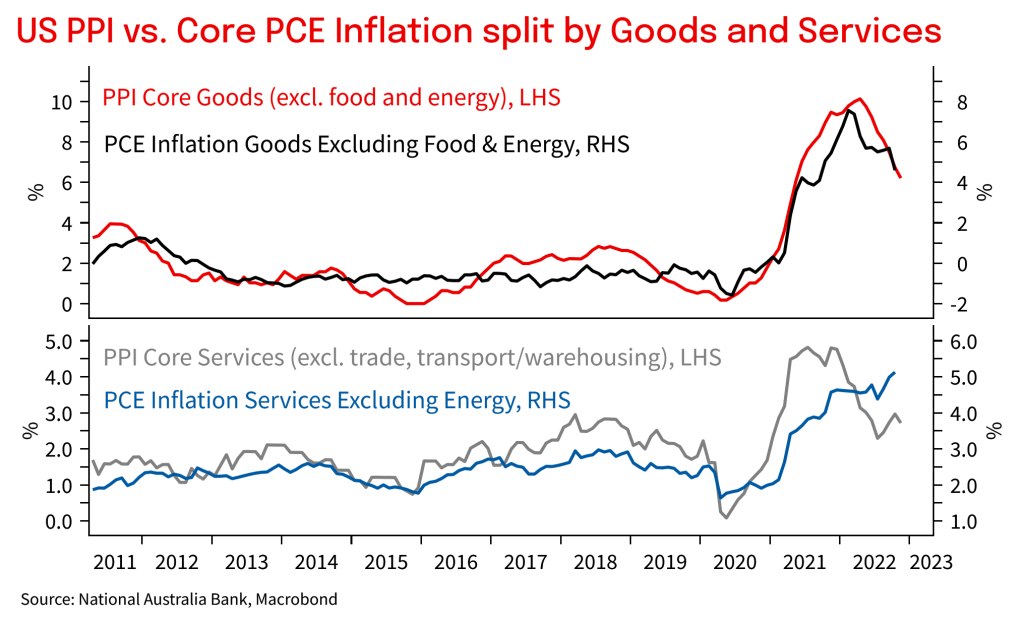

Apprehension ahead of the key risk events this week (US CPI, FOMC, ECB and BoE) was evident on Friday with both yields higher and equities lower following higher than expected US PPI figures. A stronger than expected consumer confidence print also helped fuel the sell-off later in the session. Core PPI (excl. food and energy) was 0.4% m/m against 0.2% expected, highlighting the risk that while inflation is starting to ease, it may not ease as quickly as markets expect. On the positive side the 1yr inflation expectation out of the University of Michigan survey fell to 4.6% from 4.9%, its lowest since September 2021 and no doubt reflective of the fall in oil prices recently. The only other piece of interesting news from Friday and the weekend was one Chinese official calling the mortality rate of Omicron as flu like at 0.1% and that most people recover within 7-10 days. This hints that China is moving a little quicker in its pivot to starting to live with Omicron, which should be positive for countries exposed to Chinese demand.

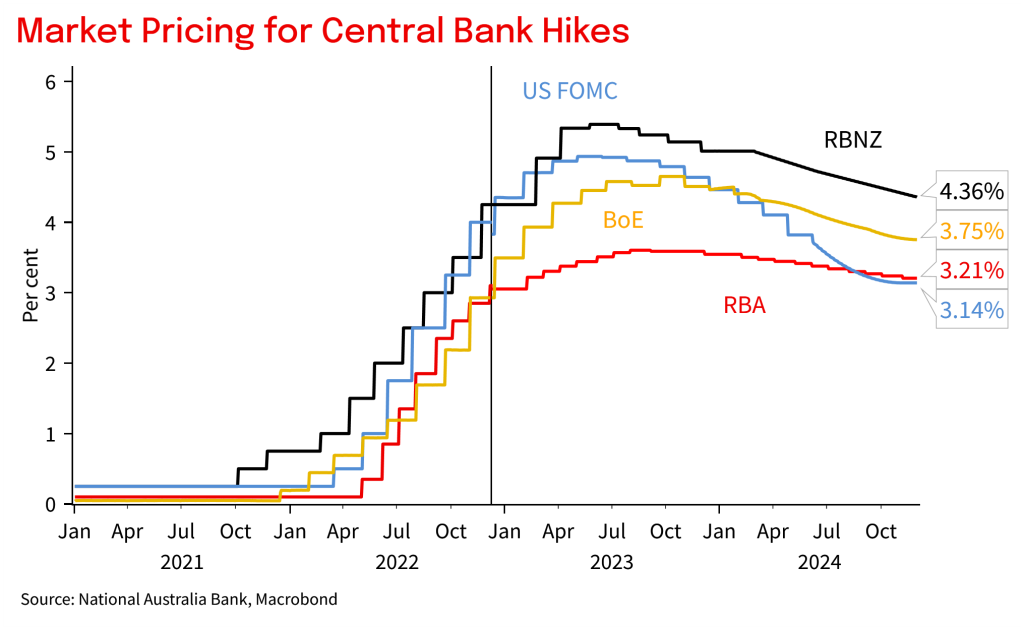

Markets moves were choppy. The S&P500 fell -0.7% and for the week is down -3.4%. The NASDAQ was similar at -0.7% and is down by -4.0% on the week. Terminal Fed Funds pricing edged slightly higher to 4.96% by mid-2023 from 4.95% on Thursday, and pricing for cuts eased very slightly to 43bps worth of cuts in H2 2023 from 46bps on Thursday. The US 10yr yield rose 9.6bps to 3.58%, and the 2yr was up less by 3.4bps to 4.34%. The 2/10s curve steepened slightly to -77.3bps. Despite the PPI printing higher than expected, implied inflation break evens fell with the 10yr breakeven -3.1bps to 2.28%. Instead, moves in nominals were reflected in real yields with the 10yr TIP yields +12.0bps to 1.30%. The USD was choppy and finished Friday broadly steady with DXY +0.1% and BBDXY unchanged. Commodity currencies were mixed with the AUD and NZD both +0.5%, but USD/CAD +0.5%. Only moderate moves were seen in the other majors with EUR -0.2% and GBP +0.2% and USD/JPY was unchanged at 136.60. The one commodity worth noting is oil, with WTI falling -0.6% to $71.02 and over the week is down some 11%.

The US PPI was the main data point on Friday. It printed higher than expected with Core PPI excl. food and energy at 0.4% m/m against 0.2% expected. Importantly the y/y figures continue to ease, suggesting inflation pressures are easing, but just not as quickly as hoped for. The print will also validate Chair Powell’s recent speech that while the October inflation numbers were encouraging, it will take substantially more progress to bring inflation down. The PPI isn’t usually a market mover, but markets are jittery ahead of key risk events this week. With PPI printing a little hotter, attention now turns to the CPI data on Tuesday, ahead of the FOMC decision on Wednesday. Also out on Friday was the University of Michigan Consumer Confidence measure which was a little stronger than expected at 59.1 vs. 57.0 and 56.9 previously. Encouragingly the 1yr inflation expectation fell to 4.6% from 4.9%, the lowest since September 2021 and likely reflective of lower petrol prices. The 5-10yr inflation expectation remained at 3.0%.

The main news headline worth highlighting is from China. One official was quoted as saying the mortality rate from Omicron is around 0.1%, similar to the common flu and that most people recover within 7-10 days. The change in language continues to tentative pivot from China over the past few weeks, both in rhetoric around the virus, and also in the easing of restrictions. The FT also reported authorities had loosened Covid testing and quarantine rules for transport workers, a move which might help ease supply chain bottlenecks (although some disruption is almost guaranteed in the short term as Covid spreads more widely). A more comprehensive re-opening probably still isn’t likely until after the winter, though in the first article the Chinese official did point to movement of people during the Lunar New Year holidays (“ It’s unlikely people will stay put for the 2023 Lunar New Year holiday so I advise those who will travel home to get booster shots so that even if they are infected, symptoms will be mild”).

Finally, in Australia on Friday the government unveiled its energy plan with passage contingent on getting The Greens and Independent Senator Pocock on board. Three key components of the plan were to cap domestic gas at $12 a gigajoule, which is a large step down from the average price so far this year of $41 a gigajoule. Cap he price of domestic thermal coal at $125 a tonne for uncontracted coal (coal was being sold at $300 a tonne at one stage), and provide $1.5bn in Commonwealth funding – matched by the states – to reduce energy bills for vulnerable households. Note household power bills have risen by 20-30% in many parts of Australia, and the government’s October Budget had forecast them to rise another 56% over the next two years (see ABC News for details).

A busy week where most focus is offshore with the US CPI on Tuesday, followed by three central bank meetings within 24 hours with the FOMC (Wednesday), followed by the ECB and BoE on Thursday. We expect all three to hike by 50bps. Bookending an important week is the Global PMIs on Friday. As for domestic focus, Employment for November is on Thursday, while across the ditch in NZ Q3 GDP figures are on Thursday. More details below:

An extremely quiet day ahead of major risk events later in the week. More details below:

Macro chart of the day – US PPI was stronger than expected, though on the goods side it is still pointing to an easing of inflation pressures

Markets chart of the day – central bank pricing is starting to divergence. Although more near-term hikes are expected, the market is also pricing hefty cuts by the US Fed in H2 2023 and 2024

NAB Markets Research Disclaimer

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.