Coming in for landing in a heavy cross wind

Insight

In a positive development the OBR will provide preliminary costings of the UK’s fiscal package on 7 October, instead of the previously signalled deadline of November 23 (the same day as the Budget).

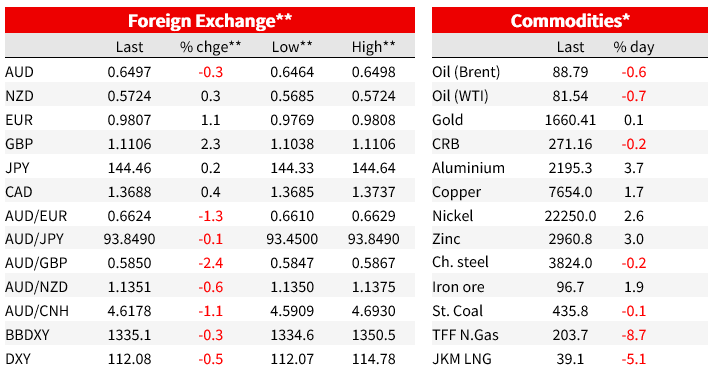

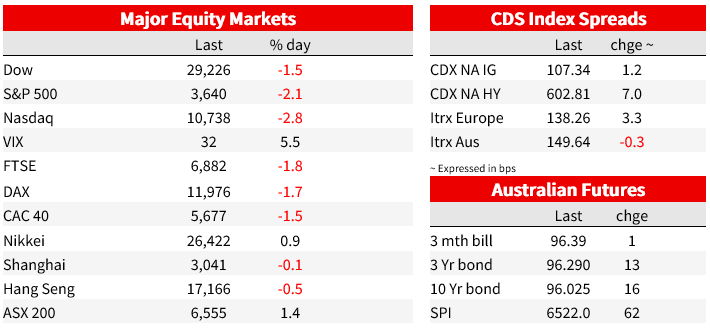

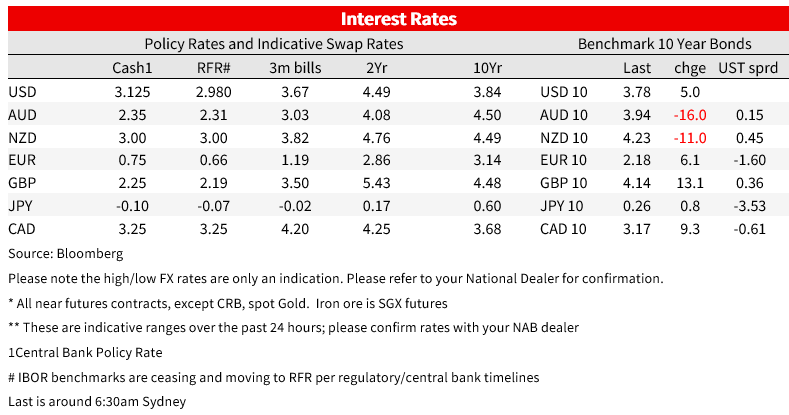

A hot German CPI print (10.9% y/y vs. 10.2% expected) yesterday served as a reminder that central banks need to remain hawkish and that the BoE’s decision on Wednesday to purchase bonds should not be read as a pivot and/or put by markets. The BoE’s Pill reinforced this view, noting purchases are “not intended…to offer more favourable underlying financing conditions…than would have prevailed in an orderly market environment” and that the fiscal package “…will prompt a significant and necessary monetary policy response in November ”. On the positive side, the UK’s OBR has said it will provide preliminary costings on the UK’s fiscal package on 7 October, alleviating fears within the markets of the so far uncosted fiscal package, helping support GBP which is up 2.3% to 1.1106. Also in the background is a notion that the UK is not alone in its fiscal ramp with Germany also unveiling a plan overnight to cap energy costs and also reverse tax rises, which is estimated to cost around 5% of GDP (or €200bn). Economic data was mixed, but in ‘good news is bad news’ US Jobless Claims fell to their lowest levels since April at 193k vs. 215k expected. No surprise then to see risk assets under pressure with the S&P500 -2.1% and more notably capitulation within mega tech with Apple -4.9% and Tesla -6.8%. Yields are up with US 10yr +5bps to 3.78%, German 10yr +6.1bps to 2.18% and UK 10yr +13.1bps to 4.14%.

First to the UK situation. In a positive development the OBR (Office for Budget Responsibility) will provide preliminary costings of the UK’s fiscal package on 7 October, instead of the previously signalled deadline of November 23 (the same day as the Budget). A full set of costings will still be made available by the end of October and importantly will also be available before the BoE meets on 3 November. This has helped alleviate some fears within markets given the initial optics of an uncosted large fiscal package. In this environment GBP has risen sharply overnight (likely positioning related given the heavy short Sterling sentiment) with GBP up 2.3% to 1.1106 and is well off its intra-day panic low of 1.0350 seen on Monday. Despite the controversy around the fiscal package, PM Truss has given no indication she was a woman for turning despite the market moves seen over the past week. Politics will ultimately dictate whether there are any changes and it is worth noting here YouGov puts the opposition Labour 33 points ahead of the governing Tory party. As for the BoE’s emergency bond buying program itself which continues until 14 October, BoE Chief Economist Pill said the purchases “…are not intended to cap or control longer-term interest rates or to offer more favourable underlying financing conditions to the institutions involved – or, for that matter, to the government – than would have prevailed in an orderly market environment”.

A full assessment will be made at the 3 November meeting and the MPC is still expected to hike rates aggressively in November. Pill noted: “It is hard to avoid the conclusion that the fiscal easing announced last week will prompt a significant and necessary monetary policy response in November”. Markets continue to price around a 150bp hike for that meeting. Despite the BoE downplaying asset purchases, a bigger issue remains. Asset purchases for financial stability considerations do not create new money on a lasting basis as long as the purchases are reversed quickly. However , it is unclear whether the BoE will be able to reverse these purchases quickly. With governments in Europe ramping up fiscal plans to insulate economies from the very large real income hits form energy prices (Germany the latest unveiling a 5% of GDP package or some €200bn; expect more European governments to announce packages), the financial needs of governments are likely to remain large. Such large financing needs may challenge the ability of central banks to undertake quantitative tightening, while financial stability concerns may also impact especially in a world given government bonds are extensively used as collateral. BoE Governor Bailey at Jackson Hole earlier in the year highlighted the issue of maintaining financial stability when hiking rates aggressively, noting then “…I think there is a very challenging question in a tightening monetary policy world, if we need to intervene for financial stability reasons. Because doing central bank asset purchases in a world where you’re tightening monetary policy is a very difficult message to get across to the outside world”.

A hot German CPI print (10.9% y/y vs. 10.2% expected) also serves as a reminder of the inflation situation in Europe (and globally) and that central banks need to remain hawkish. In such a light the BoE’s decision on Wednesday to purchase bonds should not be read as a pivot and/or put by markets. Hot inflation prints were also seen in Belgium which was an incredible 11.3% y/y, and while there is no market consensus it was up from 9.9% last month. Spain on the other hand bucked the trend with CPI of 9.3% y/y against 10.0% expected. The data comes ahead of the wider Eurozone report later tonight where upside risks are very likely given the Germany and Belgium reads. Across the pond, US economic data was strong. Initial jobless claims were 193k against 215k expected and the lowest since April. A final read on Q2 GDP was also out which was as expected at an unrevised -0.6%. That confirms the two consecutive quarters of negative growth story and it is worth noting the Atlanta Fed’s GDP Now pegs Q3 growth at just 0.3% so little improvement has occurred. One analyst also highlighted the GDP data had the profit share of the economy back towards an all time high which highlights that driving inflation has also been a profit-price spiral, as well as the well highlighted wages side. The stock market at least suggests the profit-price spiral is going to reverse.

There has been no let-up in the hawkish talk from the Fed. Cleveland Fed President Mester said inflation was “unacceptably high ” and importantly noted that despite 300bps worth of hikes “we’re still not even in restrictive territory on the funds rate” given how high inflation is. A very hawkish statement, though Mester also said her dot point was a little above the median FOMC one published in September. Mester also added the strong USD was helpful in dampening inflation, so market participants shouldn’t hold out any hope for a renewed Plaza Accord any time soon. St Louis Fed President Bullard gave a thumbs up to the market reaction after the FOMC meeting, concurring with the significant repricing in interest rate hike expectations over the next year. Across the bond ECB reheotric also remained hawkish with Simkus arguing for a 75bp hike at the next meeting.

In FX GBP has been the standout mover in the currency market, but the EUR has also made gains overnight, up around 1.1% to be 0.9807. USD/JPY continues to hover just below the 145 mark, with investors no doubt wary about the potential for further Japanese FX intervention. The fall in equities has weighed on the commodity currency complex, with the AUD -0.3% and USD/CAD +0.4%. The DXY is on the backfoot given EUR and GBP strength, -0.5%.

Finally in geopolitics it is widely expected that Russian President Vladimir Putin will announce Friday that the occupied regions are being annexed and becoming a part of the Russian Federation. There are widespread fears that Moscow could resort to using nuclear weapons to “defend” what it will then claim is its territory.

AU: Credit statistics: unlikely to be market moving with the consensus at 0.6% m/m after 0.7% last month.

NZ: ANZ consumer confidence:

JN: Jobless Rate & Retail Sales: The jobless rate is expected to fall a tenth to 2.5%, while retail sales growth is expected to be 0.2% m/m.

CH: Official PMIs and Caixin PMI: Manufacturing activity is expected to remain below 50 at 49.7 from 49.4. China’s zero-Covid strategy continues to hamper stimulus efforts. Non-manufacturing activity is expected to be 52.4 from 52.6.

EZ: CPI: Headline CPI is expected to 9.7 and core at 4.7%.

US: PCE, Chicago PM, Consumer Confidence: The PCE deflators are out with Core PCE expected to be 4.7% y/y. The Chicago PMI is expected to be at 51.8 while a final-read on the University of Michigan Consumer Sentiment is expected to be unchanged at 59.9.

NAB Markets Research Disclaimer

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.