Coming in for landing in a heavy cross wind

Insight

European and US PMIs were the main data flow overnight.

NZ: Performance of services index, Dec: 52.1 vs. 53.8 prev.

AU: NAB business conditions, Dec: 12 vs. 30 prev.

GE: GfK consumer confidence, Feb: -33.9 vs. -33.0 exp.

GE: Manufacturing PMI, Jan: 47.0 vs. 48.0 exp.

GE: Services PMI, Jan: 50.4 vs. 49.5 exp.

EA: Manufacturing PMI, Jan: 48.8 vs. 48.5 exp.

EA: Services PMI, Jan: 50.7 vs.50.2 exp.

UK: Manufacturing PMI, Jan: 46.7 vs. 45.4 exp.

UK: Services PMI, Jan: 48.0 vs. 49.5 exp.

US: Manufacturing PMI, Jan: 46.8 vs. 46.0 exp.

US: Services PMI, Jan: 46.6 vs. 45.0 exp.

US: Richmond Fed manu. Index, Jan: -11 vs. 1 prev.

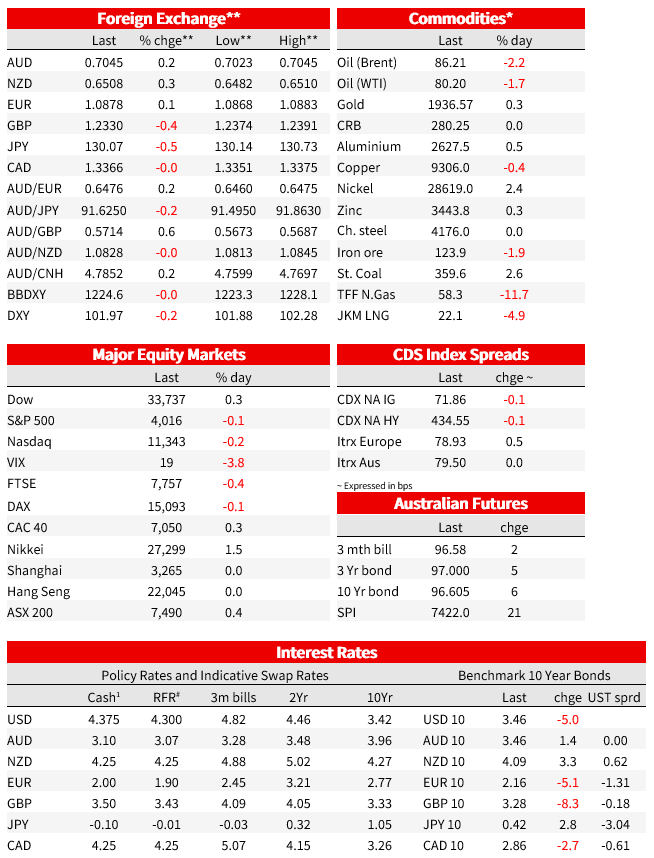

US and Euro area PMIs improved, while the theme of relative resilience in EZ data continued with the EZ composite PMI back (just) above 50 at 50.2. US equities are tracking little changed on the day after a 3% rally over the past two days. Currency moves have been modest, with the dollar down 0.2% on the DXY.

In equities, some NYSE trading issues early in the session were a source of volatility and dozens of shares saw trading halts after large swings, though the S&P500 is currently little changed , with equities mostly holding onto their 3.1% rally over the past two days. The S&P500 is tracking down -0.1%. 3M Co. was down 6% after reporting a slowdown in sales and said the company plans to cut 2500 jobs. GE topped revenue and profit expectations, with early losses reversed to small gains over the session. Earnings season continued but focus is on Microsoft earnings, due after the bell and the first of the tech giants to report this season. In other tech news, the US and eight states are suing Google, seeking a break up of its ads business. European bourses were mixed. The Euro Stoxx 50 gained 0.1%, while the FTSE100 lost 0.4%.

In other market moves, yields were generally lower globally. The US 10yr was down 5bp to 3.46%, that’s after pushing up to an intraday high of 3.55%. That intraday peak was seen after a 2-3bps boost from the US PMIs that also supported the USD, before the moves were fully unwound. Aiding the retracement, the Richmond manufacturing index fell to its lowest level in over 2½ years at -11 after +1 in December. German 10yr yields were 5bp lower at 2.16%, while 10yr gilt yields were 8bp lower at 3.28%.

FX moves were relatively muted. UK PMI data on the weak side of both expectations and their continental counterparts saw the pound underperform. The GBP was 0.4% lower against the dollar at 1.233 after paring losses from an intraday low of 1.2264, while the euro was up 0.1% 1.0878. The AUD gained 0.2% against the dollar and is currently around 0.7046. The yen gained, with USD/JPY losing 0.5%.

As for the detail of the PMIs, they reinforced the themes of a more-resilient-than-feared Europe against relatively slower, if improving, US momentum. The US PMIs were a little stronger than expected, with the composite at 46.6 from 45.0 and 46.4 expected. The Services PMI, enjoying a little more focus than usual after the more closely watched ISM measure last month dipped towards the weaker PMI indicator, jumped to 46.6 from 44.7 and 45.0 expected.

The Eurozone reading suggested the Eurozone economy was doing no worse than flatlining with the Composite PMI rising to 50.2 from 49.3 and 49.8 expected to edge back above 50. The important services index rose to 50.7 from 49.8 and 50.1 expected. A plunge in gas prices alongside a mild winter is a key support, reflected in cooling input cost pressures, though selling price inflation ticked higher. In contrast, the UK services index fell by more than expected to 48.0, its lowest level in a year. The report noted pressures from industrial disputes, staff shortages, export losses, rising cost of living and higher interest rates.

There was more commentary from ECB speakers . Markets price 49bp at the 2 February meeting, and there appears to be little disagreement about 50 at that meeting, but some divergence views thereafter even as Lagarde pointed to “significant” interest-rate increases at coming meetings” on Monday. Overnight, hawk Simkus pointed to still high core inflation and wage growth set to beat historical averages as he said the ECB should continue with half point increases and that a peak may be unlikely before Summer. For the more dovish perspective, Panetta said that “We can afford to be ‘anxiously optimistic,’ ” and said the ECB should firmly commit to rate moves beyond February. New projections in March should instead be an opportunity to reassess the situation.

In Australian data yesterday, the NAB Survey showed Business Conditions down 8pts to +12 . That’s a third successive decline, but despite the recent falls is still comfortably above long run averages, reflecting just how exceptionally strong business conditions had been through much of 2022. Confidence rose 3pts to -1 in December to remain below average. Ahead of Q4 CPI data today expected to show a peak in year-ended inflation, there were also signs of easing inflation pressures evident across pricing and cost indicators that add weight to the outlook for disinflation. While still elevated generally fell further from recent peaks.

Also on the calendar are the German IFO survey and US Mortgage applications.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.