Coming in for landing in a heavy cross wind

Insight

Australia has become the latest nation to express concern about the use of the Astra Zeneca vaccines on young people, except here young is anyone under 50.

https://soundcloud.com/user-291029717/job-confusion-yield-consolidation-vaccine-concerns?in=user-291029717/sets/the-morning-call

“Cause I don’t care when I’m with my baby, yeah; All the bad things disappear; And you’re making me feel like maybe I am somebody”, Ed Sheeran and Justin Bieber 2019

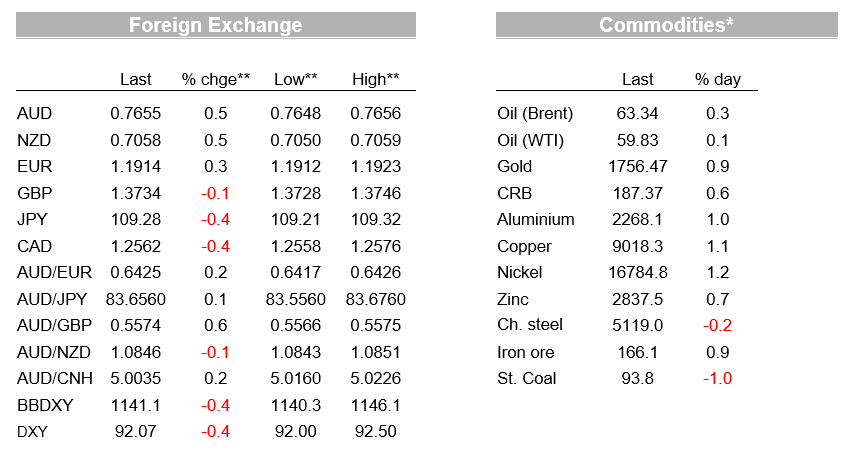

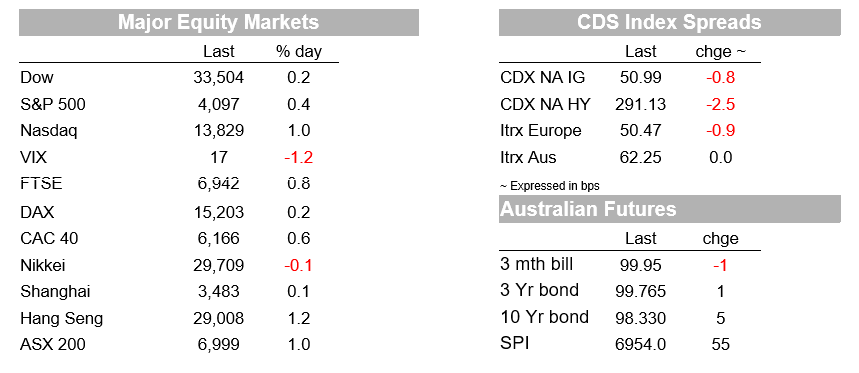

Markets continue to brush off delays around the global vaccine rollout, still very much pricing the other side of the recovery. Overnight there was a dearth of any significant news to add to this backdrop, while yields (US 10yr -4.6bps to 1.62%) consolidated with the Fed’s Powell re-stating existing guidance around rates and asset purchases likely adding. The move lower in yields over the past week has seen a tilt back towards growth/IT stocks – overnight S&P500 +0.4% and NASDAQ +1.0%. A larger than expected increase in US Jobless Claims was largely ignored given strong labour market indicators recently. The USD has also fallen across most G10 FX with the DXY -0.4% overnight and the lowest in two weeks. The AUD is up 0.4%, broadly in line with USD weakness. Australia’s decision to restrict the AstraZeneca vaccine to those over 50 years has had little impact given extensive virus control in Australia, though could delay the vaccine timeline into 2022.

The rally in equities and the move lower in yields came before the dovish comments from Fed Chair Powell, though his comments likely reinforced the theme. Chair Powell noted that “the recovery remains uneven and incomplete”, adding that, while the March nonfarm payrolls report was pleasing, the Fed wanted to see “a string of months like that” before it could feel confident the recovery was making progress. Powell also reinforced that spare capacity in the US economy remains extensive, noting that his commute home take him past a “ substantial tent city”. The Fed’s Bullard who sits on the other side of the dove-hawk spectrum also noted we need to see a clearer end to the pandemic before assessing a tapering of asset purchases. Bullard though was confident that full employment could be achieved within a year.

Questioned on inflation, Powell reiterated that the Fed expected a short-term bump higher, but it expected this to be transitory. He added that the Fed would be watching inflation expectations closely and in the unlikely event, in his view, that inflation expectations started moving uncomfortably high, the Fed “ have the tools to deal with that” (read: it would raise interest rates). Separately, uber-dove Kashkari said he wouldn’t panic if inflation hit 4%, wanting to assess whether it was temporary or something more longer lasting. The rates market, which prices just over three Fed rate hikes by the end of 2023, shows that investors think the Fed will ultimately start its tightening cycle earlier than its current projections indicate. The market also remains less sanguine than the Fed about inflation risk. Inflation options show the market sees a 30% chance of CPI inflation averaging more than 3% over the coming

Data overnight was limited with a worse than expected US Jobless Claims brushed aside by the market given more positive labour market indicators. Initial Jobless Claims were 744k v. 680k expected and 728k previously for the w/e Apr 3rd . Note the higher than expected numbers come in the wake of a stellar payrolls report, while alternative real-time indicators such as job ads point to an ongoing surge in labour demand. Job postings on Indeed are now 16% above where they were in February 2020. It could be that filing backlogs for jobless claims are driving the high claims numbers.

The other news that markets are seemingly brushing aside is the delay in the vaccine rollouts following age limits being placed on the AstraZeneca vaccine by a number of countries. Overnight Australia restricted its use, recommending it not be used for those aged below 50 years and instead the Pfizer/BioNTech vaccine be used (note age limits have recently been put in place by Spain, Italy, France, Germany and the UK). The age limit in Australia has the potential to delay Australia’s vaccine rollout plan given AstraZeneca was to account for around two-thirds of vaccine supply this year. Australia also has also ordered 20m doses of the Pfizer/BioNTech vaccine, though the timeline for delivery is less clear and more will be needed given there are around 11.2m Australians aged between 18 to 49 years (two vaccine doses are required). For now the AstraZeneca rollout can continue for the 8.5m people aged 50 years and above. The concern globally is that vaccine hesitancy may rise given the extensive media coverage around AstraZeneca. Any delays to the global vaccine rollout will emphasise US outperformance given in the US 76% of the over 65 years population has received one vaccine dose and 57% have received the full two doses.

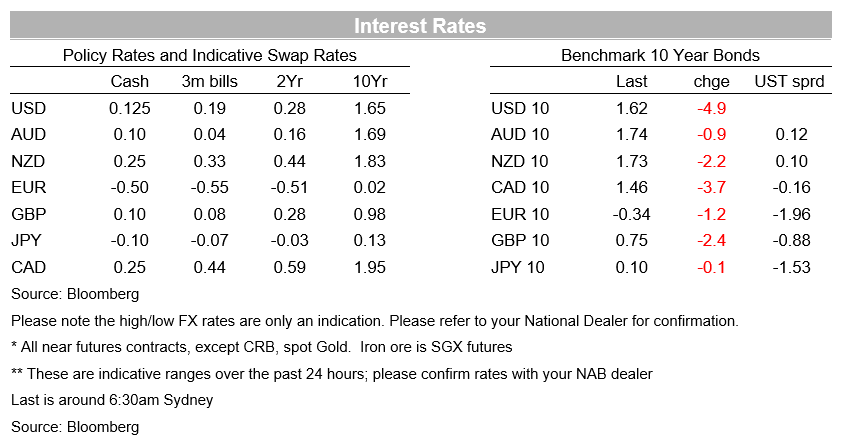

Bond yields overnight continued to drift lower, extending the moves seen over the previous few days. The 10-year Treasury yield is down 4.9bps overnight, at 1.62%, near its lowest level in a fortnight. The retracement in bond yields this month looks more like the market is entering a period of consolidation, after what had been a very big move in a short space of time, rather than a change to the market’s economic outlook. Across the pond, the ECB Minutes showed that the frontloading of asset purchases implemented at the meeting would be subject to a “quarterly joint assessment.” Notably, the minutes also said that perception of implicit yield curve control “had to be avoided.”

The USD has broadly followed the move in yields with the DXY down 0.4%. EUR has pushed above 1.19 (+0.4%), breaking above its 200-day moving average, while USD/JPY (-0.6%) has fallen towards 109 amidst the decline in Treasury yields. The GBP has underperformed again and is broadly unchanged despite broad-based USD weakness against other currencies. Growing concerns around the AstraZeneca vaccine, which the UK has relied on heavily for its speedy vaccine rollout, are likely weighing on the GBP.

The RBA’s Financial Stability Review is a highlight in what is another quiet day for Australia. It is also very quiet offshore with the only highlight being the RBNZ’s chief economist talking. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.