Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Equities in the US spent most of the session rising, driven by the news that Pfizer and BioNTech’s experimental vaccine has being fast tracked in the US.

https://soundcloud.com/user-291029717/shares-rise-on-vaccine-hopes-then-fall-on-china-tensions?in=user-291029717/sets/the-morning-call

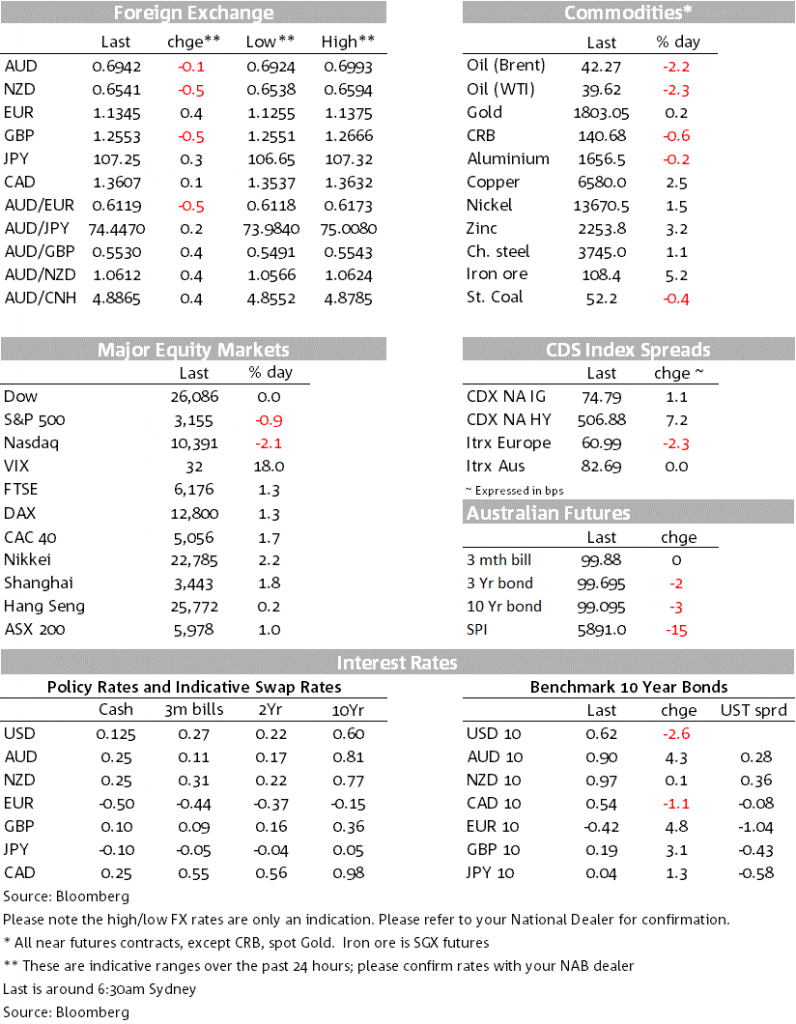

US equities started the new week on a positive note with the S&P 500 trading to a new a COVID-19 high early in the session. But mixed US virus news and renewed heightening US-China tensions soured the mood in the US afternoon with both the S&P 500 and NASDAQ ending the day in the red. AUD and NZD continue to find resistance at 70c and 66c respectively and end the day a tad softer.

European equities had embraced the positive lead from Asia and both the S&P 500 and NASDAQ were enjoying a good start to the new week, up close to 1.5%. This meant that the S&P briefly traded to a new COVID-19 high of 3235 and the NASDAQ was also printing a new record high. Tesla, the new darling in the US equity, was also on a tear, up 16% , after gaining 11% on Friday.

With PepsiCo reporting better-than-expected earnings and revenue for Q2. Earnings for the S&P 500 are expected to fall 44.6% in Q2 from a year ago (-55% for the Eurostoxx), although analysts have been revising their expectations higher over recent weeks. With investors already well-conditioned for a big fall in earnings in Q2, a lot of the focus is expected to be on the earnings outlook and guidance from company executives as the global economy reopens. JP Morgan, Citi and Wells Fargo report tomorrow

It is hard to attribute a specific trigger for the turn in sentiment that followed in the US afternoon trading session, but it seems that California virus news and US China tensions were the main culprits.

With Pfizer and BioNTech’s experimental vaccines granted fast track designation by the US regulator and phase three trials are now expected to commence later this month. Florida reported over 12,000 new cases on Monday, but the proportion of people testing positive with the virus continued to drift lower (to 11.5%, a two-week low). The spread of COVID-19 also looks to have peaked in another of the US hotspots, Arizona, which reported its lowest level of new cases in a fortnight (1,357). In New York City there were no COVID-19-related deaths reported on Saturday, the first time for months.

Virus statistics in California were disappointing. After reporting record daily levels of infection on Saturday, California Gov. Gavin Newsom ordered the entire state to close indoor activities in restaurants, bars, museums, zoos and movie theatres. He enacted further restrictions on activities in counties that are on the state’s monitoring list, which has grown to include 80% of the state’s population. California accounts for about 15% of the US economy, so the introduction of containment measures is likely to have a hindering effect on the recent improvement in US economic activity readings.

Yesterday China announced sanctions on several US officials, including senators Rubio and Cruz, following the US imposed sanctions on Chinese officials last week. Also in a significant change of position, late in the US session, US Secretary of State Michael Pompeo released a statement rejecting China’s expansive claims in the South China Sea. Pompeo’s statement noted that “We are making clear: Beijing’s claims to offshore resources across most of the South China Sea are completely unlawful, as is its campaign of bullying to control them,”. In the past the US has called for protecting “freedom of navigation” in the South China Sea, the overnight statement is now taking a position against China on the territorial disputes in the region.

Which saw the VIX index jump from 27.39 to 32.19 in the overnight session. The US 10-year Treasury yield closed the sessions at 0.6184%, about 2.5bps lower relative to Friday’s closing levels and remains firmly contained within its 0.55% – 0.75% trading range.

The USD index (BBDXY) reached a one-month low, but a reversal in the equity market triggered a safe haven bid helping the greenback recover almost across the board. The Euro and Danish Krone, were the exception up 0.39 and 0.43% respectively. Gains in the euro have come ahead of the EU leaders’ summit at the end of the week, where countries will try to find agreement over the proposed EU recovery fund. The proposal is for the bulk of the €750b fund to be distributed as grants, rather than loans, to the worst-affected (and already debt-saddled) countries in the region, like Italy, although there is reportedly opposition from several Northern European countries. The JPY and GBP are both lower on the day ( -0.41% and -0.55% respectively), with the latter possibly affected by market concern over the lack of progress in Brexit negotiations.

Overnight both pairs came close to trading above their respective big figures, but true to form the negative turn in equity sentiment weighed on both antipodean currencies. AUD now trades at 0.6940, down -0.14% over the past 24 hours and NZD trades at 0.6545, down 0.53%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.