We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

The risk off mood is being driven by increasing inflation concerns.

https://soundcloud.com/user-291029717/vertigo-and-inflation-fears?in=user-291029717/sets/the-morning-call

We’re tumbling down, We’re spiralling

Tied up to the ground, We’re spiralling – Keane

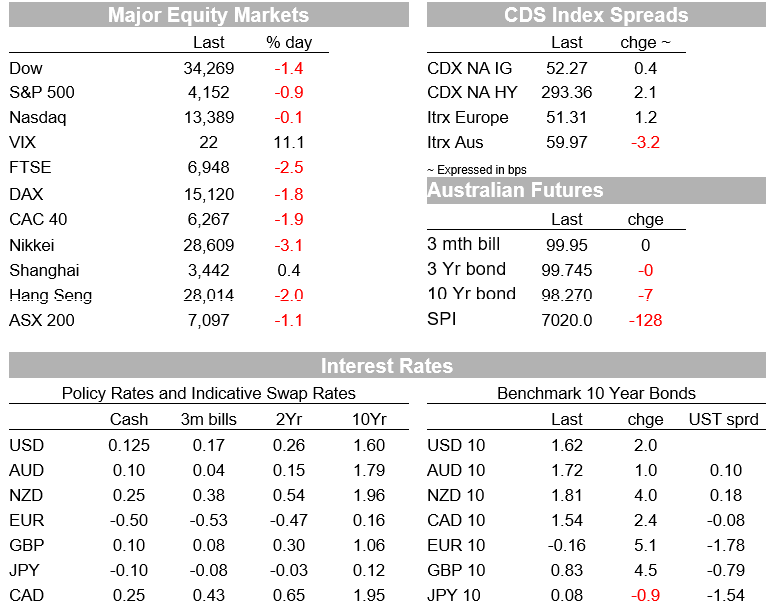

The tech led equity rout that began on Monday’s US trading session extended into our APAC region yesterday and overnight Europe joint the retreat with some heavy losses. US equities are down again, but this time the declines have been led by cyclical sectors. UST yields have edged a little bit higher with longer dated tenors leading the move up while the FX market continues to watch from the sidelines. The USD is still lingering close to year to date lows while the AUD and NZD range trade.

Inflation concerns against a backdrop of higher commodity prices was identified as the reason for the US technology led equity sell-off on Monday night. So, looking at the culprits, commodities had another decent night with copper up 1.3%, but iron ore, the recent big mover was steady (-0.42%) while oil prices were also little changed. Meanwhile, breakevens also had a steady night with the 10y UST breakeven up 1bps to 2.54%.

That said looking at the data releases over the past 24 hours, one could argue that we had at least one more new evidence that inflation is on the rise. Yesterday we learned that China PPI rose 6.8% yoy, its fastest pace since October 2017, following a 4.4% gain in March . The median forecast was for a 6.5% increase. Looking at China’s PPI and CPI in one chart there is certainly a historical relationship that shows a rise in producer prices does eventually get passed onto the consumer. China consumer prices increased 0.9% yoy, slightly below the 1% gain projected by economists.

Hence, with the tech selloff perpetrators still lurking in the background, yesterday’s APAC equity indices took a beating with tech heavy indices such as Taiwan’s TAIEX leading the decline, down 3.79% while the Nikke was not too far behind, down 3.08% ( IT and communication sectors down 3.83% and 4.64% respectively).

Looking at the overnight price action, the equity narrative has worsened with the rout becoming broader and more intense. The Stoxx Europe 600 Index fell 2%, its worst drop since December 21, all sector recorded loses and the biggest declines came from pro cyclical sectors such as industrials, consumer discretionary and energy, all down between 2.20% and 2.4%.

US equities show a similar pattern with the Dow leading the declines, down 1.36%. The S&P 500 has ended the day -0.87% with industrials, financials and energy at the bottom of the pile with the IT sector “only” down -0.24%. It seems that the tech led equity rout has now given investors the excuse the clear the deck across the board after decent year to date gains.

Moving onto economic news, US job openings surged to March to a record high of 8.12 million in March and the number of vacancies exceeded hires by over 2.1 million. The report noted employers saying that they are unable to fill positions because of ongoing fears of catching COVID19, child-care responsibilities and generous unemployment benefits. Analysts noted these same factors after Friday’s very poor jobs report, which highlighted that supply (of labour) factors are a much more important constraint on the labour market than demand – something that monetary policy is ill-equipped to deal with.

The median price for a single-family home in the US rose the most on record in the first quarter, lack of inventory against a surge in demand is pushing prices higher. The median price is 16.2% higher from a year earlier to a record high of $319,200. So again more evidence of asset price inflation fro ultra-easy monetary policy.

The April NFIB index of small business activity and sentiment rose to 99.8 from 98.2, below the consensus, 101.0. The April headline was lifted by a seven-point increase in the earnings expectations measure. The April rebound leaves the index just three points short of its pre-Covid peak and consistent, if sustained, with robust growth in business fixed investment.

Against a backdrop of broadly lower equity returns, stronger US data releases were a bigger influence on UST yields with the curve extending its recent bear steeping as longer dated tenors led the move up in yields. The 10y Note edged up 1.8bps to 1.62% while the 30y Bond climbed 2bs to 2.348%.

Fed speakers were also out in force, staying with the narrative that more of the same is still needed with the US economy still far from the Fed’s goal . Influential Governor Lael Brainard said “Remaining patient through the transitory surge associated with reopening will help ensure that the underlying economic momentum that will be needed to reach our goals as some current tailwinds shift to headwinds is not curtailed by a premature tightening of financial condition.,”. Fed Bostic said the US labour market is still 8m jobs short of its pre-pandemic levels and the economy therefore requires ongoing Fed support.

Interestingly given the current market focus on Inflation, Fed Bullard noted that he expects 2021 inflation at 2.5% to 3%, adding that some, but not all, of the inflation is transitory and that he expects inflation likely at around 2.5% in 2022 . Thus, from his perspective, transitory higher inflation is not a story of a few months.

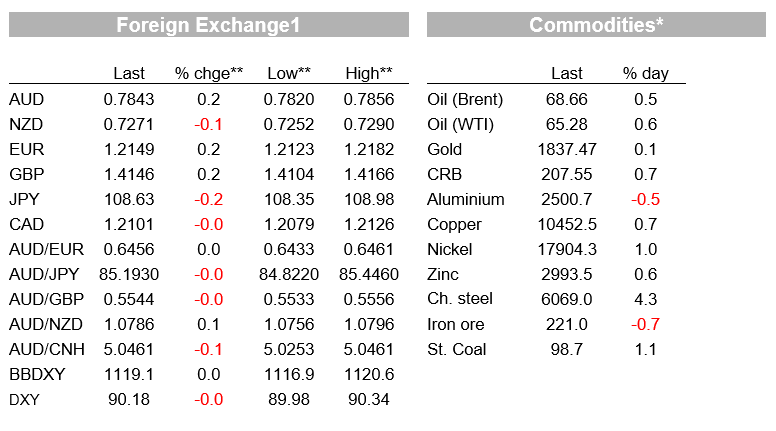

The FX markets has continued to watch the equity action form the sidelines with the USD little changed and still close to year to date lows on both DXY and BBDXY terms. European currencies are at the top of the G10 leader board, up around 0.20%, although SEK is the standout up 0.37%. The AUD and NZD have range traded and now trade at 0.7842 and 0.7275 respectively.

The AUD showed little reaction the big fiscal spending revealed on the federal budget . Last night the Treasurer unveiled a raft of new spending measures offsetting the cyclical improvements in the budget due to a better than expected economic outcome. So, budget repair is on hold for now with the main focus still on supporting the economy and maximum employment.

The 2021-22 deficit is pencilled in at $106.6bn, well above expectations of $80bn and little changed from December’s MYEFO of $108.5bn. The 2020-21 deficit is a little higher than expected at $161.0bn compared to the $152bn consensus, though is still well down on December’s MYEFO of $197.7bn. Importantly deficits are forecast all the way to 2031 22 with the structural budget balance replacing temporary fiscal measures in coming years.

In terms of spending the largest item was the aged care package – at around $17.7bn over the forward estimates. But there were other big spends in the areas of Infrastructure ($15bn) and NDIS ($13.2bn). The Low-and Middle-Income tax offset was extended a year ($7.8bn) and the Investment Asset Write Off also was extended. Other areas of focus included childcare, home ownership support and a number of tweaks to superannuation to ensure greater flexibility (as well as support for women).

Overall, our economists have no problem with the focus on maintaining the support for economic growth but note the scope for more structural / productivity enhancing measures to have been included. Cutting red tape, tax changes and greater support for alternative energy environment would have been preferred. That said, we are only getting a partial view of the likely budget outlook and much can and will probably change in the lead up to the election. See here and here for more from our economists.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.