Coming in for landing in a heavy cross wind

Insight

Last week will be marked out as one of the more tumultuous for financial markets since the early days of the pandemic, says NAB's Ray Attrill.

Data round up:

UK August Retail Sales -1.6% (-0.5% expected)

UK Retail sales ex auto fuel -1.6% (-0.7% expected)

Final August Eurozone unchanged at 9.1%, HICP 9.1% up from 9.0 prelim.

University of Michigan Sep Consumer Sentiment 59.5 from 58.2 (60.0 expected)

University of Michigan 5-10yr inflation expectations 2.8% from 2.9% (2.9% expected)

Good Morning

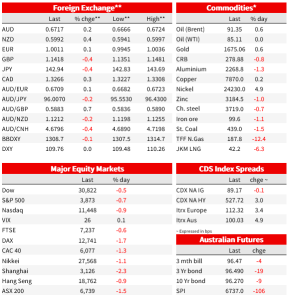

Friday ended with more of whimper than a bang, but last week will still be marked out as one of the more tumultuous for financial markets since the early days of the pandemic. It encompassed an almost 8% high to low swing in the NASDAQ (6% for the S&P500), 43bps low to high range for the US 2-year Treasury yield (23bps for the 10-year) and 2.4% ranges for both the DXY USD index and AUD/USD, the latter recording a new 2-year low on Friday of 0.6670.

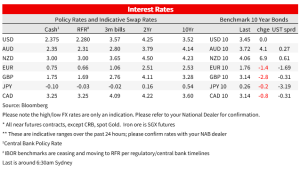

That’s a 0.3% upside surprise on US August core CPI for you, a related result of which was to see US money markets lifting their pricing for the implied terminal fed funds rate to 4.4%, in Q1 next year, a rise on the week just shy of 50bps. This week sees the Fed, Bank of England, and Bank of Japan and SNB in action, in what is a very holiday-impacted week, including Japan, the UK and Canada Monday, the day of the Queen’s funeral.

As for the Fed, a poll of leading academic economists by the Financial Times in conjunction with the University of Chicago and published on Saturday shows nearly 70% of the 44 academics polled expecting the Fund rate to peak between 4% and 5% with 20% of them seeing a peak above 5%. Whatever the peak, 68% of those polled do not see a reduction until 2024 at the earliest.

As for market participants, a poll of 120 of them by Macropolicy Perspectives published Saturday shows 87% expecting a 75bps funds rate rise this Wednesday (10% expect a 100bps move) larger, with the median respondent expecting the median funds rate path in the “dot plot” to feature a year-end rate of 3.875% which if the Fed hikes 75bps in September as expected would imply a total of 75bps in hikes over the November and December meetings. Our median respondent then expects a median 2023 “dot” of 4.125% followed by 3.625% in 2024 and 3.0% in 2025.

There was no Fed speak on Friday nor at the weekend with FOMC official in their pre-meeting cone of silence. Not so at the ECB, where Bundesbank President Nagel speaking Saturday said, “We’re still very far away from interest rates that are at a level that is appropriate given the current state of inflation”. “More needs to happen, rates have to go up — by how much is still to be determined,” he said. “We’re still a good way off” from the neutral rate. ECB chief economist Lane meanwhile told Irish broadcaster RTE the ECB will raise interest rates several more times and that a mild recession in the euro area can’t be ruled out, comments which add nothing to what we heard on the day of the 75bps rate rise earlier this month.

Two economic data points of note Friday were for UK retail sales and US consumer sentiment. UK August retail sales came in at -1.6% on both the headline and ex-auto fall measures, well below the -0.5% and -0.7% expected respectively data which saw the GBP/USD exchange rate fall to a new post-1985 low of $1.1350. the University of Michigan’s preliminary September Consumer Sentiment index rise to a still depressed 59.5 from 58.2. More significant were the inflation expectations readings, in the case of the 1-year rate, down to 2.8% from 2.9% (lower petrol prices a factor) and the more closely scrutinised (by the Fed) 5-10 year reading to 2.8% from 2.9%, its lowest since April 2021 and against peak of 3.1% in June and January this year. Pre-pandemic, they averaged 2.5%.

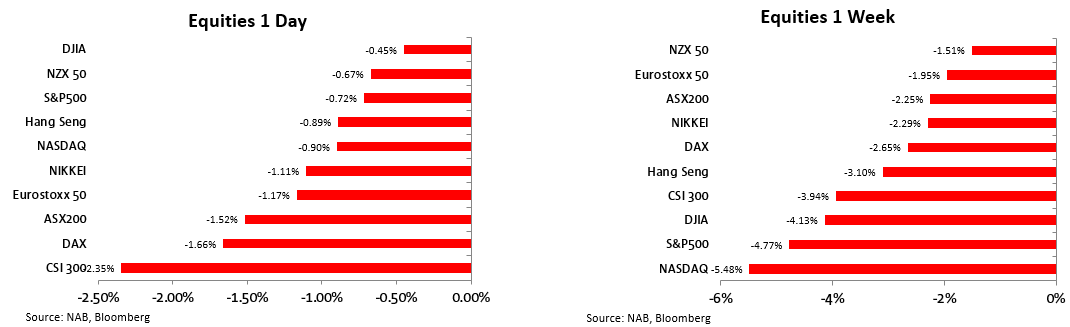

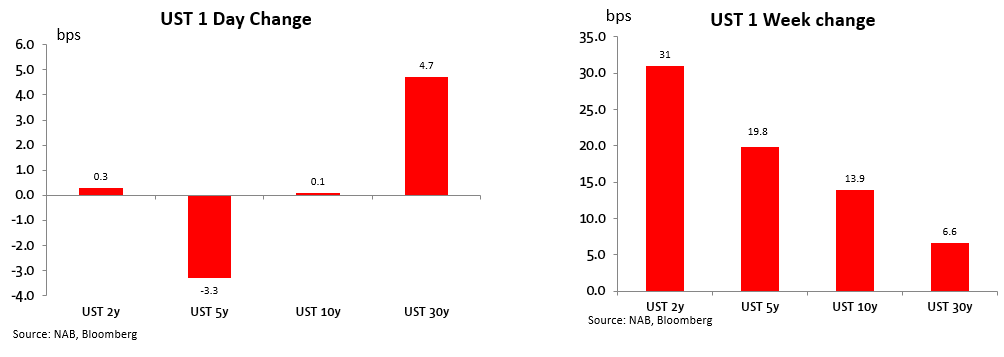

Market wise, Friday saw US equity loses extended, the S&P500 by another 0.7% for a 4.8% weekly loss and the NASDAQ on 0.9% for a 5.5% fall on the week – the worse performing major global stock market. Equity market losses came amid a mixed performance in bonds on Friday where both US 2s and 10s were little changed but this still left them with loss of 31bps on the week for the 2-year and 14bps for 10s. So, an 17bps additional 2/10s curve inversion over the course of the week to -42bps, re-approaching their early August -50bps extreme.

One contributor to US market weakness Friday was FedEx, its stock losing more than 20% following a post-Thursday close profit (and revenue) warning for the remainder of 2022 and with 2023 seen worse than this year. FedEx blamed “macroeconomic weakness” in Asia and “service challenges” in Europe for a $500 million revenue shortfall in these regions, while FedEx Ground is about $300 million below company forecasts, the company said.

A combination of the switch back from goods to services post pandemic, plus a weakening (global) economic backdrop, are evidently both at play here, but it is the latter that arguably not yet adequately priced into risk asset prices in an environment where markets are having to ratchet ever higher their view of terminal central bank policy pricing, with its direct read-through to interest rate sensitive sectors (hence NASDAQ being the worse performing major stock market last week).

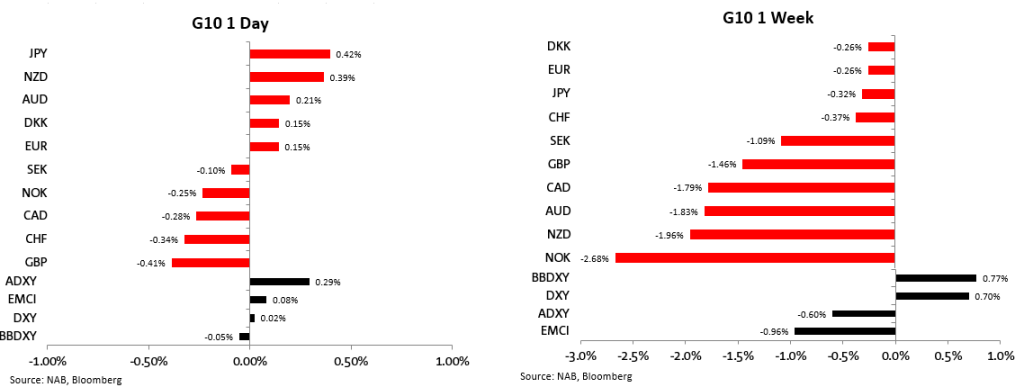

In currencies, it was the commodity/procyclical/most risk-sensitive ones that suffered the most last week, much more so than EUR/USD (-0.26%), the latter limiting the rise in the DXY USD index to 0.7% (to 109.76, 0.9% below its 7 September 20-year high). AUD and NZD moves lower were augmented by the run up in USD/CNH and USD/CNY though 7.0 on Thursday and Friday respectively. The AUD/USD 0.6670 low on Friday capped a 2.4% loss for the week, to its lowest since 1 June 2020. The NZD low of 0.5941 on Friday is its lowest since 18 May 2020.

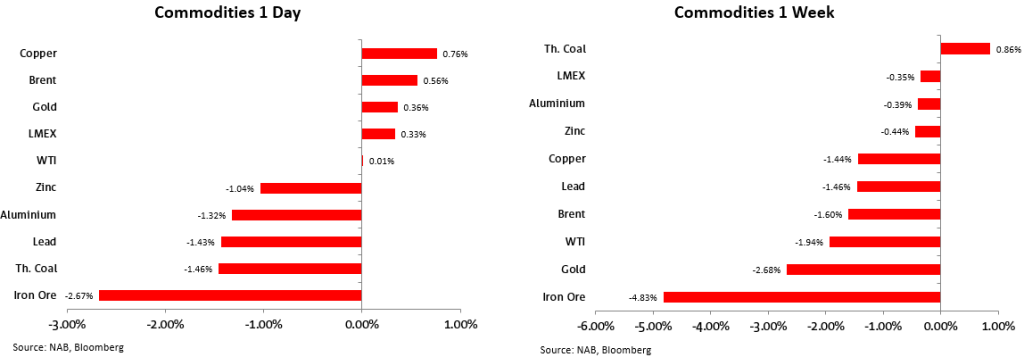

NOK fared worse on the week amongst G10 currencies in the context of lower oil prices. Brent crude pulled up a little on Friday (WTI was flat) but was still down 1.6% on the week. Iron ore was the worse performing major hard commodity off a cool 4.8%, but with some offset as far as Australia’s terms of trade is concerned by a 0.9% rise for thermal coal – the only hard commodity to be higher on the week.

NOK fared worse on the week amongst G10 currencies in the context of lower oil prices. Brent crude pulled up a little on Friday (WTI was flat) but was still down 1.6% on the week. Iron ore was the worse performing major hard commodity off a cool 4.8%, but with some offset as far as Australia’s terms of trade is concerned by a 0.9% rise for thermal coal – the only hard commodity to be higher on the week.

Coming Up

NAB Markets Research Disclaimer

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.