Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Newsletter

Another day spent in anticipation of Powell’s speech tonight

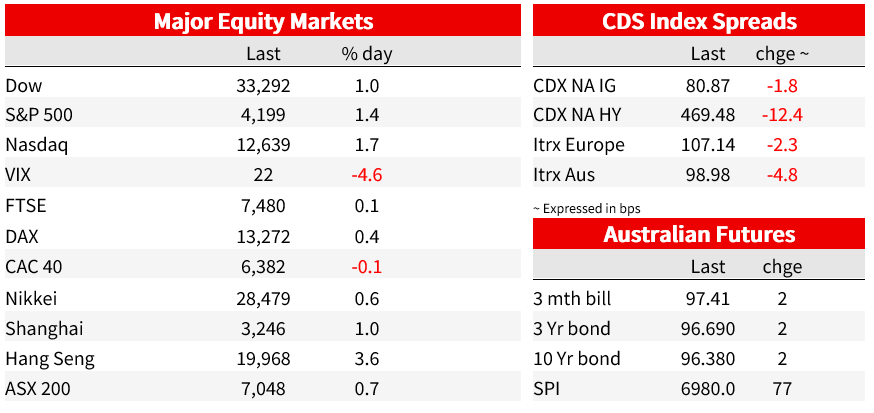

Hawkish commentary out of a cast of Fed speakers overnight was of little consequence as markets await Powell’s keynote at Jackson Hole this evening. US equities were higher. The S&P500 was 1.4% higher and the NASDAQ up 1.7%, much of that coming in the last hour of power and unwinding some of the declines seen earlier in the week. European equities were mixed, the Euro Stoxx 50 up 0.2%. US yields were lower, led by the longer end.

Fed speakers interviewed ahead of the Jackson Hole conference were on message that the inflation fighting task is not yet done and that rates need to go into restrictive territory. Kansas Fed’s George said there is “more room to go” and that “I think we will have to hold — it could be over 4%. I don’t think that’s out of the question.” Those comments were mirrored by Philadelphia’s Harker, who said “I think we get up to a restrictive stance, sit for a little while, let things play out” and not overreact to shifting data ” Atlanta Fed’s Bostic said it was a coin toss at this point between 50bp and 75bp for September, noting he would want to see the CPI data and also echoed George’s message that a fed funds rate at current levels was not yet restrictive. He sees a neutral closer to 3. St Louis President Bullard repeated that he wants to get rates to 3.75-4 by the end of the year and said that “a baseline would be that probably inflation would be more persistent than what many on Wall Street expect,” a risk he sees as underpriced by markets.

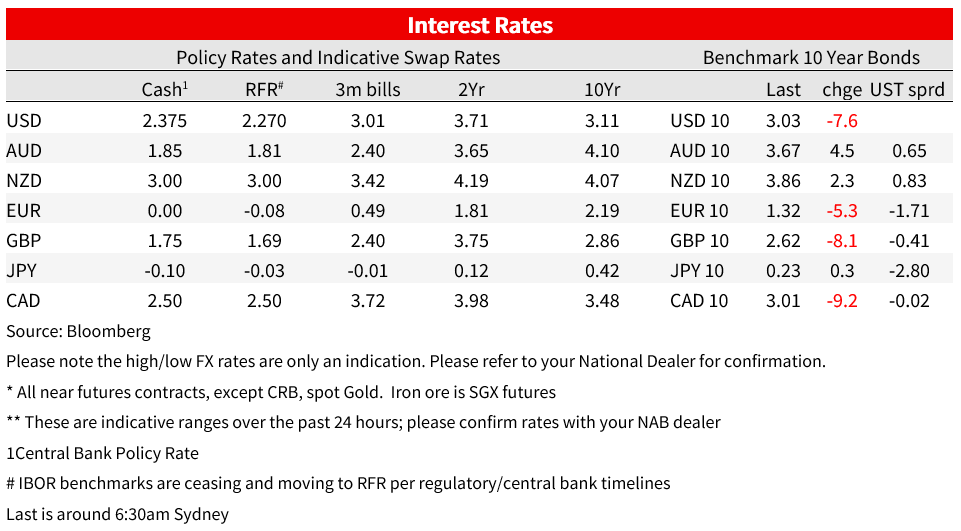

Despite those messages, US yields have fallen back. 10yr yields are 8bp lower, more than reversing yesterday’s move but remaining above 3% at 3.03%. Curves flattened, with the 2yr down 2bp to 3.37%. The 2s10s moving deeper into inversion at 35bp, back to levels seen a week ago. Some investors closing short positions ahead of Powell’s remarks likely helped the rally in rates, while a 7yr bond auction saw strong demand.

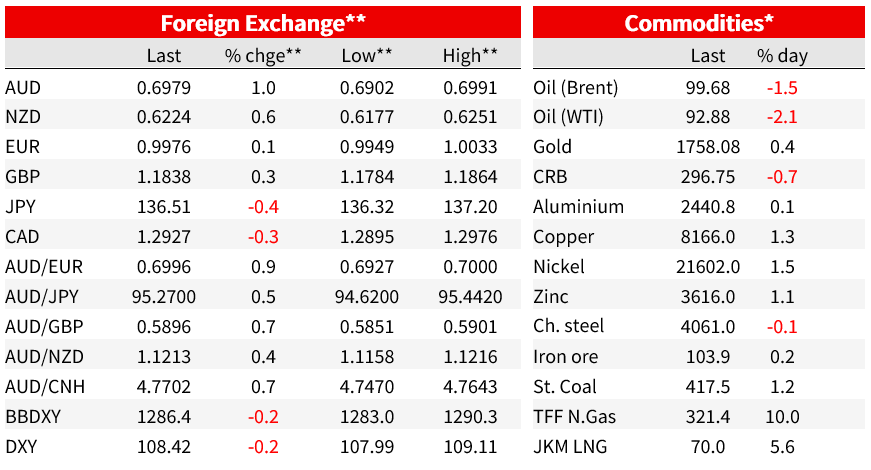

In currency markets, the USD was a little softer on the DXY, down 0.2%. The euro was little changed, up 0.1% to 0.9976 after testing briefly back above parity intraday at a high of 1.0033. The USD lost 0.5% against the yen amid the fall in US rates, while the AUD outperformed, rising 1.0% to 0.6979, hitting an intraday high of 0.6991.

In the data flow, initial jobless claims were a little stronger than expectations at 243k vs 252k expected from a downwardly revised 245 last month. With seasonal adjustment issues that have complicated the assessment recently fading, a flatter trend is emerging with claims off the April lows, but still around lows as a share of employment. The second estimate of US GDP for Q2 showed an upward revision to -0.6% q/q from -0.9% on the back of an upward revision to consumption, the revision largely signalled in advance by retail sales. The gap to the GDI measure, which should theoretically equal the GDP estimate, continued with the first estimate of GDI showing a 1.4% gain in Q2 after a 1.8% gain in Q1, leaving wide open the possibility that declines in Q1 and Q2 GDP are revised away come revisions in October and suggesting that activity was stronger through H1 than the GDP estimates imply.

The ECB account of the July meeting has largely been overtaken by events given the rapidly shifting energy cost outlook. For the record, some members preferred a smaller 25bp lift off, but a very large number supported the larger move, justified by “clear materialisation of upside risk since the previous meeting.” The ECB also noted a commitment to fighting inflation even in the face of slowing growth, “ It was argued that even a recession would not necessarily diminish upside risks (to inflation), especially if it was related to a gas cut-off or another supply shock implying a further increase in inflation.” On that note, the energy outlook in Europe remains fraught. German and French power have risen to fresh records on further nuclear reactor outages as benchmark natural gas futures jumped another 10%. On the data side, the German IFO index was not as bad as feared, largely unchanged in August at 88.5, still its weakest reading since mid-2020 and, before that, 2009. Markets are currently pricing around 100bp from the ECB over the next two meetings, including some chance that it could raise its cash rate by 75bps next month.

Across the ditch, NZ retail sales data for Q2 was sharply softer than expectations, with real sales falling 2.3% on the quarter, much weaker than the +1.7% market consensus. A policy-affected 5.8% fall in spending on vehicles didn’t help the cause, but our BNZ colleagues note the weakness went much deeper than this. Ex-auto retail trade, in real terms, slipped 1.6% in Q2. The down-cycle in the housing market looks to be having a bearing on overall spending trends, with notable declines in spending volumes on big ticket durable goods items over the quarter.

In other news, China’s State Council yesterday announced another ¥300n (~0.1%/GDP) of funding which state banks can use to fund infrastructure projects. That is only a modest step in the face of mounting economic headwinds and the readout from the meeting gave the impression there were limits to the amount of stimulus likely to be forthcoming amid concerns about leverage and difficulties stimulating credit amid the construction slowdown noting “no flooding of easing measures and no overborrowing from the future.”

Coming Up

NAB Markets Research Disclaimer

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Newsletter

We see our NAB commodity index falling substantially in 2024, despite higher forecasts for base metals and gold.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.