Firmer consumer and steady outlook

Insight

Fed's Waller inches open the US rate cut door

Events round-up

GE: GfK consumer confidence, Dec: -27.8 vs. -28.2 exp.

US: Conf. Board consumer confid., Nov: 102 vs. 101 exp.

BN: Fed’s Waller says he’s more confident policy is well positioned

US: 7Y notes draw 4.399% vs 4.378% pre-sale when-issued, bid/cover ratio 2.44 from 2.70; indirect bidding 63.9% from 70.6%

Road to Damascus conversions don’t get any bigger then former Fed hawk Governor Waller who today opened up the possibility of rate cuts in three to five months’ time if inflation continues its trend down (If inflation continues to cool “for several more months — I don’t know how long that might be — three months, four months, five months — that we feel confident that inflation is really down and on its way, that you could then start lowering the policy rate just because inflation is lower”…“It has nothing to do with trying to save the economy or recession.”

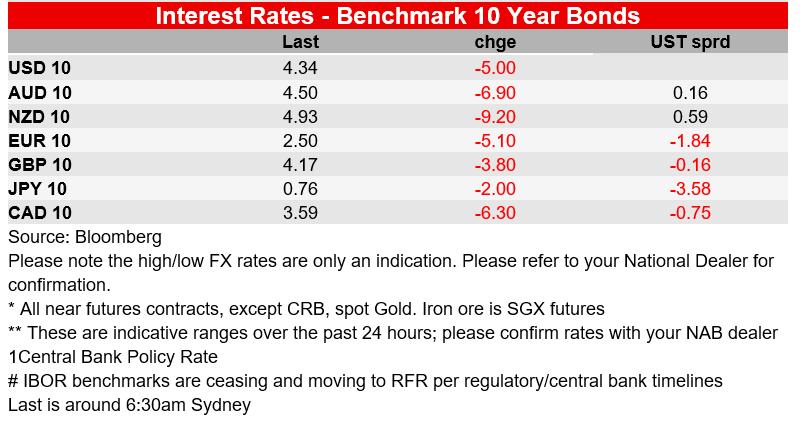

US 2yr yields fell sharply in response, moving -13.8bps to 4.75% in response (low 4.75%; high 4.89%). The curve bull steepened with a smaller fall in 10yr yield of -4.8bps to 4.34% (low 4.33%; high 4.42%). Driving some move off the lows in longer-term yields was a poor 7yr auction of $39bn which was awarded at 4.399% vs 4.378%, giving a tail of 2.1bps. Equities are mixed with the S&P500 -0.0% heading into the last half hour of trade, along with the NASDAQ. The USD is down -0.4% on the DXY and BBDXY.

Fed Funds Futures imply around 100bps worth of cuts in 2024, up from 92bps of cuts yesterday. Fed Governor Bowman also spoke and favoured higher rates, but the market clearly moved on Governor Waller’s opening up the possibility of cuts, which echoes what Williams and Powell said earlier in the year about cutting rates before you got to 2% in order to keep the same level of restriction (i.e. stop real rates from rising). Waller also noted “I am increasingly confident that policy is currently well-positioned to slow the economy and get inflation back to 2%”.

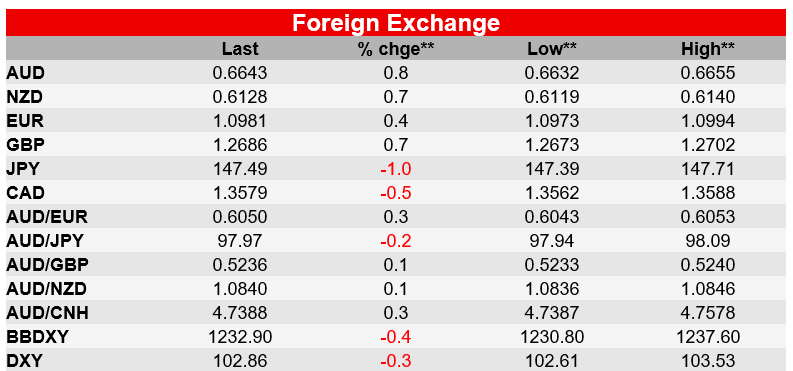

In FX it has been a story of ongoing USD weakness. DXY is -0.4% and most pairs are higher. Yen is outperforming with USD/JPY -1.0% to 147.51, as is the AUD +0.8% to 0.6643 and NZD +0.7% to 0.6128. Smaller increases were seen in EUR +0.4% to 1.0980 and GBP +0.6% to 1.2685. The USD (DXY) since its October highs is now -4.2%, with all that coming in the context of markets seeing the US Fed as being done in this cycle, with cuts now on the agenda.

In that context, my NZ colleague notes JP Morgan’s Treasury client survey for the week ended 27 November showed that the most active investors in the US Treasury market are the most bullish they have been in the history of the survey, which dates back to 1991. Some 78% of active clients were long US Treasuries relative to benchmark, up from 56% the previous week, none were short, and the rest were neutral.

The data calendar has remained light and not a factor. US consumer confidence on the Conference Board measure rose for the first time in four months to 102.0 in November, close to expectations, albeit from a downwardly revised 99.1, supported by falling gasoline prices and rising stock prices. The labour market indicator based on the difference between those saying jobs were hard to get and those saying jobs were plentiful, was little changed, although this indicator of labour market pressures has been easing through most of this year.

Finally in Australia, yesterday’s October Retail Sales isn’t likely to influence the RBA given the shifting seasonality associated with November’s Black Friday/Cyber Monday. Instead of more interest was RBA Governor Bullock’s remarks at the BIS-HKMA conference. Here Bullock again re-iterated Australia’s inflation challenge was now more domestic. Ms Bullock also was more explicit around the mid-point of the 2-3%, which to us reinforces the RBA is likely to lag the global easing cycle given the RBA only forecasts core inflation at the very top of the 2-3% band by the end of 2025. NAB continues to see the RBA lifting rates again in February.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.