Total spending grew 0.9% in June.

Jump in US jobless claims supports lowers US yields and US$; S&P500 back in bull market

A jump in weekly US jobless claims together with a sharp fall in oil prices have done little to near term Fed policy pricing but have pulled bond yields down – including at 2-years – and given momentum to a USD downdraft that was underway ahead of the news. This sees AUD/USD regain the foothold above 0.67 it had only briefly established on Wednesday. The US equity market likes the lower yield story (ex- Energy and one or two other sub-sectors) with the S&P500 back in bull market territory and closing up 0.6% on the day, the NASDAQ a bigger 1.0%.

US weekly jobless claims , recently distorted by the discovery of fraudulent claims in some parts of the country, jumped to 261k last week, up from 233k the prior week. Its possible the Memorial Day holiday last Monday has distorted the figures, though the numbers are certainly consistent the normally lagged impact of other lead indictors of the labour market such as Challenger lay-offs. Early days, but the June non-farm payrolls report is building to be a particularly interesting.one – on the wages front in particular – given that money markets continue to price some 21bps of Fed tightening over the combined June and July FOMC meetings.

The other big news story overnight is oil, with WTI crude off around $2 to just over $71 and Brent $1.50, following local media reports Iran and the US have made progress in talks over Iran’s nuclear program. A deal would, on some estimates, potentially see an extra million barrels or so of oil added to global supply. WTI had fallen as much as 4.8% (low of $69.0) before paring losses, after a US State Department spokesman said, “Any reports of an interim deal are false.”

US jobless claims aside, economic news flow had been pretty light. Of some note Eurozone Q1 GDP was revised down to -0.1% from 0.1% (0.0% had been expected). This follows earlier downward revisions to German GDP and means that both Germany and the broader region have now recorded back-to-back negative quarters of growth and so a ‘technical recession’ (Eurozone GDP was also -0.1% in Q4). Earlier Thursday Japan Q1 GDP was revised up to 0.7% from 0.5% (2.7% annualised) though the breakdown was not so flash, coming mostly on higher inventories with Household Consumption revised down by 1/10%.

In equities the 0.6% gain for the S&P500 mean that on a closing basis, the index is now more than 20% up on its 3,577 12 October 2022 close (20.3%) so ‘officially’ back in a bull market. The NASDAQ’s 1.0% gain leaves it a little shy of its high earlier in the week – it is currently 29.5% up on its 28 December ’22 low. Consumer discretionaries have actually been the biggest percentage contributor to the S&Ps gains (+1.6%) followed by IT (1.20%). Earlier Thursday European stocks closed narrowly mixed, e, g, Eurostoxx 600 unchanged, FTSE100 -0.3%.

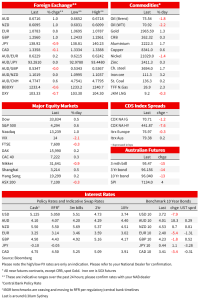

Bond markets see lower 10-year yields in all major jurisdictions, including a ~5bps decline in futures-implied 10-year Aussie yields since Thursday’s local close and, to the nearest half a basis point, 10-year Treasuries 8.5bps down, Bunds -5.5bp, BTPs -10bps and Gilts -2bps.

Amongst G10 currencies, the NOK had fared best on day when oil prices are smartly lower – go figure (note to self – never trade NOK). USD/CAD has performed more in accordance with its fundamentals, at 0.1% the poorest performing G10 currency on a day when the USD and oil prices are both lower. A crowded leader board has, NOK aside, CHF, NZD, GBP, AUD and JPY all showing gains of 1.0% plus or minus a little bit (lower Treasury yields the main contributor to the latter). AUD/USD has finished in New York at 0.6716, its highest close since 10 May.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.