Confidence and Conditions Lift

Insight

Rise in 1y ahead US inflation expectations spooks markets

Weekend Headlines

Coming up:

Events Round-Up

NZ: BNZ Manufacturing PMI, Sep: 52 vs. 54.8 prev.

CH: PPI (y/y%), Sep: 0.9 vs. 1 exp.

CH: CPI (y/y%), Sep: 2.8 vs. 2.9 exp.

US: Retail sales ex auto, gas (m/m%), Sep: 0.3 vs. 0.2 exp.

US: Retail sales control group (m/m%), Sep: 0.4 vs. 0.3 exp.

US: Uni. Michigan consumer sentiment, Sep: 59.8 vs. 58.8 exp.

US: Uni. Mich. 1y inflation expectations.: 5.1 vs 4.6 exp.

US: Uni. Mich. 5-10y inflation expectations.: 2.9 vs 2.8 exp.

Volatility in markets remained elevated on Friday with an unexpected rise in US inflation expectations alongside ongoing UK political drama keeping investors nervous. US equities ended the day sharply lower, erasing a good chunk of Thursday’s post-CPI rebound. The UST curve bear steepened while Fed’s terminal rate expectations edge up toward 5% next year. UK assets also endured a volatile Friday after PM Truss fires her Chancellor and makes a U-turns on corporate tax rate. King Dollar remains in charge, up on Friday and the week while the AUD is the whipping boy, staying true to its risk sensitivity. JPY is the other underperformer with not signs of intervention, GBP also underperforms on Friday, but is the outperformer on the week. Over the weekend new UK Chancellor Hunt promises further fiscal U-turns while China’s president warns of “dangerous storms ahead” and reaffirms Taiwan reunification without doubt.

The UK political drama took centre stage again on Friday . Against a backdrop of huge pressure from nervous markets, her own party, and the Bank of England, PM Truss sacked Kwasi Kwarteng her trusted friend and Chancellor. Following the previous week’s U-turn on the top tax rate, Truss `then announced that the government would go ahead with raising the corporate tax rate from 19% to 25%. The U-turn on the corporate tax rate will save an estimated £18b per year (from the initial tax cut package of ~£45b), the PM also announced Jeremy Hunt as the new Chancellor and promised spending cuts in a desperate bid to restore credibility.

Market reaction to the news was not a positive one, suggesting investors were clearly not impressed by PM Truss unconvincing 8 minute speech. Even after the u turn on the Corporate tax, Bloomberg estimated that an additional £24bn ($27bn) of savings were still needed to get the UK public finances on a sustainable footing. 30y UK Gilts traded in a 58.6bps range on Friday, initially falling to a low of 4.25% then shooting up and ending the week at 4.78%. Investors are clearly concern over the need for pension funds to de-risk amid a lack of clarity in terms of how much unfunded spending the UK government plans to implement, bearing in mind too that the BoE ended its emergency bond buying programme on Friday.

Late on Friday media reports suggested PM Truss had struck an agreement with the new chancellor that he wouldn’t abandon any more of her agenda. But speaking to several media outlets over the weekend, the Hunts message couldn’t have been any different, stressing “Spending will not go up as much as people want and there’ll be more efficiencies to find.” while also noting “We won’t have the speed of tax cuts we’re hoping for and some taxes will have to go up”.

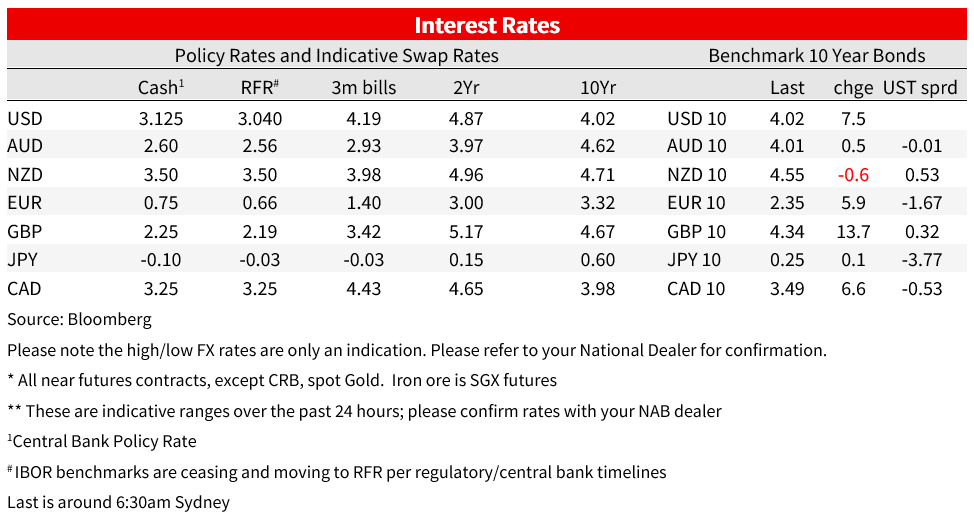

Also, over the weekend, BoE Governor Bailey gave his seal of approval to the corporate tax U-turn but said the fiscal measures announced to date (including the expensive energy price cap) “will require a stronger response than we perhaps thought in August”, possibly foreshadowing a big rate hike come the November meeting (the market is pricing a hike on the order of 100bps). The BoE meeting takes place after Hunt’s medium-term fiscal statement, so the Bank will be able to factor in any changes to the fiscal package when it makes its rate decision and updates its economic forecasts.

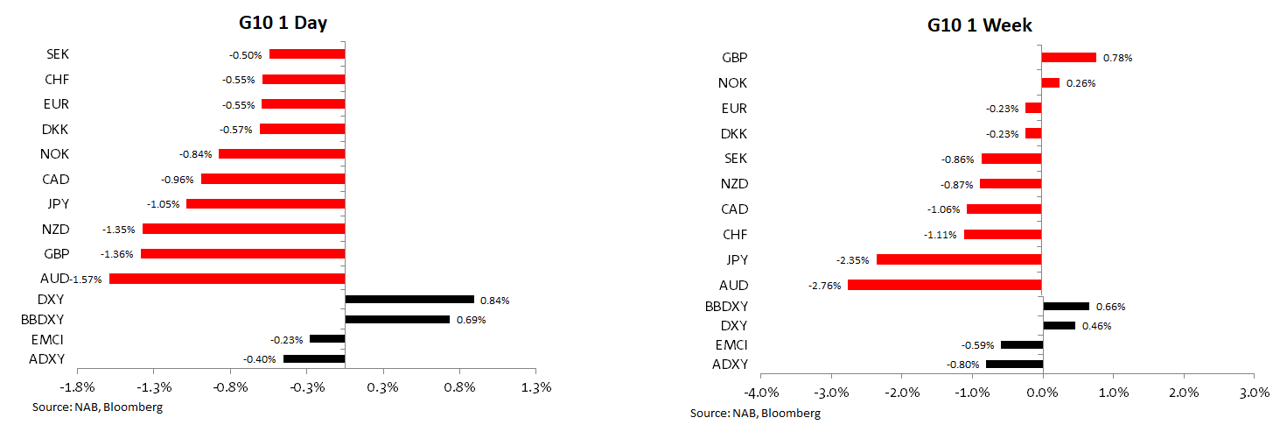

The new Chancellor’s comments alongside BoE Governor Bailey observations over the weekend should help appease UK markets on Monday, although PM Truss position is looking increasingly unattainable. GBP was also volatile on Friday, closing the day down ~1.4%, reversing some of the gains in previous day, indeed GBP was still the best performing G10 over the week, up 0.78%. This morning GBP is up 0.6% to 1.1252, reflecting a sense of approval to official commentary over the weekend.

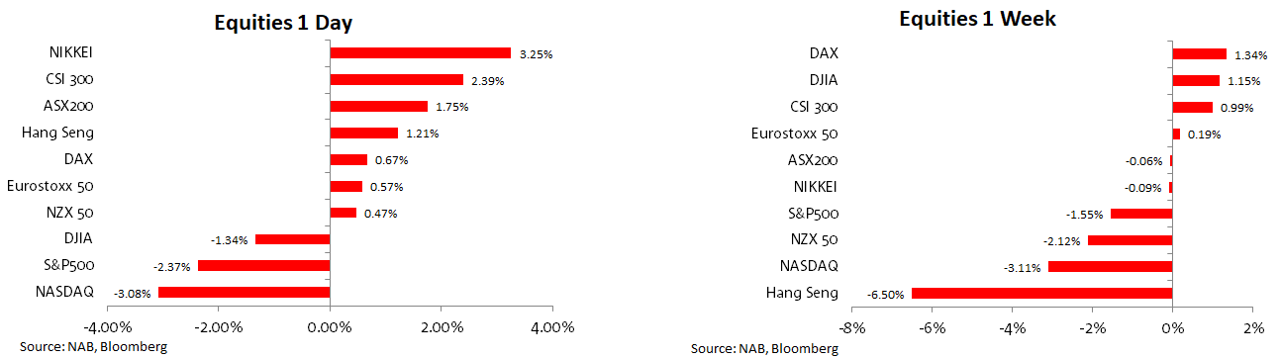

Moving onto the US equity market, it seems that after some short covering on Thursday, US equity investors came around to the idea that higher inflation does mean the Fed needs to remain aggressive with its policy tightening approach. The release of the University of Michigan survey on Friday also served as a reminder with both the 1y and the 5 to 10y inflation expectation readings rising against expectations for small declines.

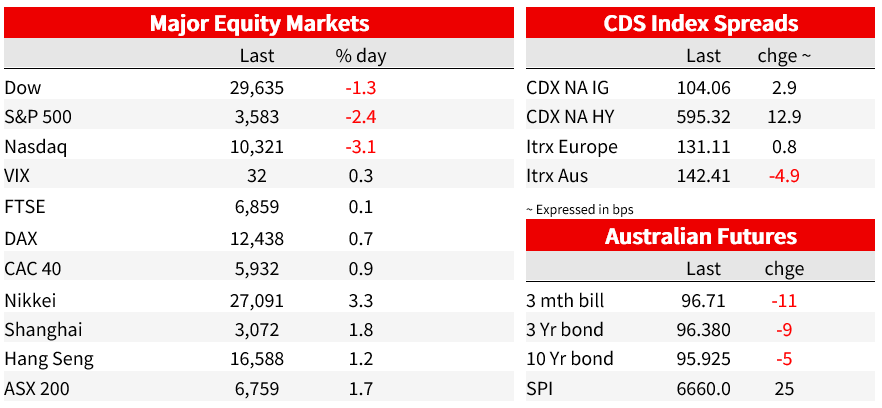

The S&P 500 Index fell 2.4% on Friday, ending the week with a 1.6% loss and reversing the entirety of last week’s rally. All 11 major industry groups were lower, led by the energy and consumer discretionary sectors. Big tech led the selloff, with Apple, Amazon and Tesla weighing the heaviest on the broad equities benchmark. The tech-heavy Nasdaq 100 Index slumped 3.1%, closing at its lowest since July 2020, while the blue-chip Dow Jones Industrial Average fell 1.3%.

US Banks’ earnings reports were also mixed on Friday, JPMorgan shares rose after the banking giant reported its highest quarterly net interest income ever while Morgan Stanley sank after top-line revenue came in worse than expected.

Earlier in Europe, the Stoxx 600 index closed 0.6% higher paring earlier gains of as much as 2.3%, weighed down by the decline in US equities after the University of Michigan survey release. The FTSE 250 rose as much as 2.5% before trimming its gains following PM Truss press conference, the index ended the day just 0.1% higher.

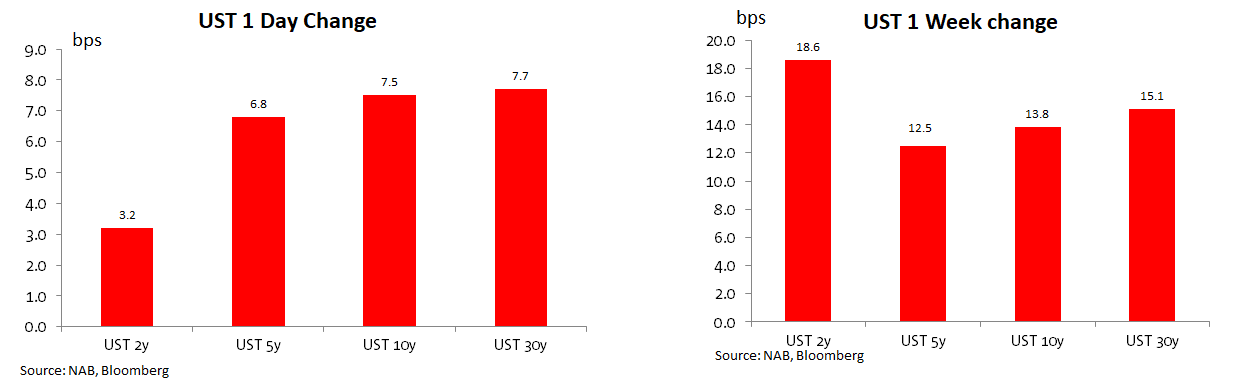

Moving onto the rates markets, the implications of the upside surprise to US CPI continue to sink in on Friday with the University of Michigan survey inflation expectations readings a trigger for the move up in UST yields on Friday ( Of note the year-ahead inflation expectations increase to 5.1% from 4.7% in October was the first increase since March). The UST curve bear steepened on the day with the 2y rate gaining 3bps to 4.497% while the 10y Note rose 7bps to 4.0184%.

The market is fully pricing a 75bps hike from the Fed next month and a slightly better-than-even chance of a follow up 75bps hike in December while pricing of the Fed’s terminal rate edge up 6bps to 4.96% in May next year . Even some of the more dovish Fed officials are flagging the possibility of a higher terminal cash rate than the most recent ‘dot plot’, with San Francisco Fed President Daly saying, after a “very disappointing” CPI release, that “the most likely outcome ” was a peak cash rate between 4.5% and 5%.

Fed Bullard spoke during the weekend (at the IMF/World Bank gathering) opening the door to the possibility the Fed would raise interest rates by 75 bps at each of its next two meetings in November and December, while saying it was too soon to make that call he expressed support for at least another 125 bps of hikes this year.

Bullard, who has been a leading voice in terms of Fed action before and during the current tightening cycle also said that “2022 is the year of frontloading but 2023 would be the year of data-dependence or ordinary monetary policy at this newer, higher level of the policy rate”. This means than in 2023 the Fed will be reacting to data “with possibly higher or possibly lower rates, while expressing support for another 125 basis points of hikes this year.

Consistent with our forecast, Fed Bullard also referred to the strength of the USD noting that the rapid Fed hikes contributed to the strength of the USD, but that may ease once the Fed reaches the point of pausing the hikes. We have pencilled this pivot around the turn of the year.

In economic data, US core retail sales (ex autos and gas) were stronger than expected, increasing 0.3% in September (with the prior month revised up too). Retail spending remains firm, supported of late by lower gas prices and households dipping into their large saving balances. The Atlanta Fed’s GDPNow measure suggests healthy annualised quarterly GDP growth of 2.8% in Q3.

The USD was back on the driving seat on Friday aided by the move up in Fed fund hiking expectations as well as the increase in uncertainty , evident by the ramp up in volatility across markets. Both the BBDXY (0.69%) and DXY (0.84%) advanced on Friday and close the week at higher levels than the previous week.

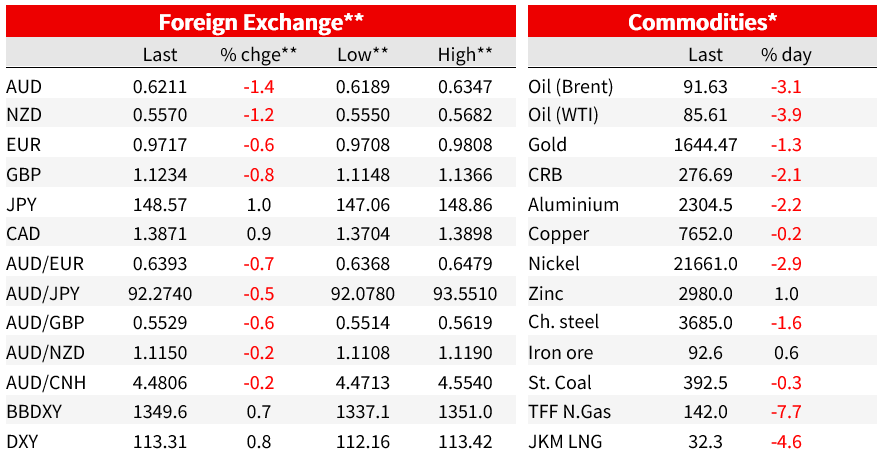

True to form the AUD was the whipping boy on Friday and indeed on the week. The AUD is one of the most liquid currencies in the world and given the prevalent risk aversion in the air, the AUD is proving yet again to be the weapon of choice to express risk aversion. The aussie was the G10 underperformer on Friday, down 1.57%, ending the day close its lows at 0.62. The move up in sterling this morning has given the AUD a small lift, now trading at 0.6212.

In addition to GBP mentioned above, NZD and JPY were the other notable underperformer, down 1.36 and 1.05% respectively. USD/JPY climbed above 148 on Friday (148.7 close) following the move up in UST yields. Talk of intervention has remained, but no action so far while fundamentally the yen is doing what it should given ultra-easy BoJ policy.

Finance Minister Shunichi Suzuki said Friday that Japan is “deeply concerned” about rapidly increasing volatility in the market and chief currency official Masato Kanda said authorities were prepared to take “bold action.”`. Meanwhile, speaking on Saturday, BoJ Governor Kuroda said “The BOJ considered it appropriate to continue with monetary easing, to support the economy, to ensure a shift in norms and to ensure the price stability target in a sustainable and stable manner,”

In other news, speaking at the 5-yearly National Congress of the Chinese Communist Party President Xi Jinping declared China’s global power had increased while warning of “dangerous storms” ahead. Xi defended China’s zero-covid policy, saying it protected the people and the economy, noted technology self-reliance is a key goal of the party and reaffirmed China’s commitment to gaining control over Taiwan, even forcefully if necessary.

Over the weekend the Australia’s Federal Government announced its pledge to spend A$9.6 billion ($6 billion) on infrastructure projects as part of its October 25 budget . Projects worth $2.6bn will be funded in the state of Victoria, while $1.5bn will be allocated to Queensland and New South Wales will get about $1bn. The AAP quoted Prime Minister Anthony Albanese saying on Sunday. “Sound and planned infrastructure investment in Australia creates jobs, builds opportunity and unlocks economic growth and productivity for our cities and our regions.”

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.