NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

It has been a volatile session overnight driven by differing headlines around vaccine efficacy, capped off by very significant hawkish tilt by US Fed Chair Powell in Senate Testimony.

https://soundcloud.com/user-291029717/who-are-you-and-what-have-you-done-with-jerome-powell?in=user-291029717/sets/the-morning-call

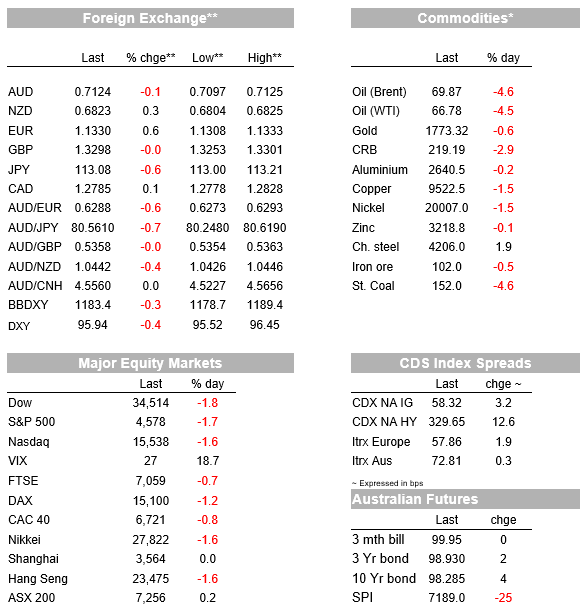

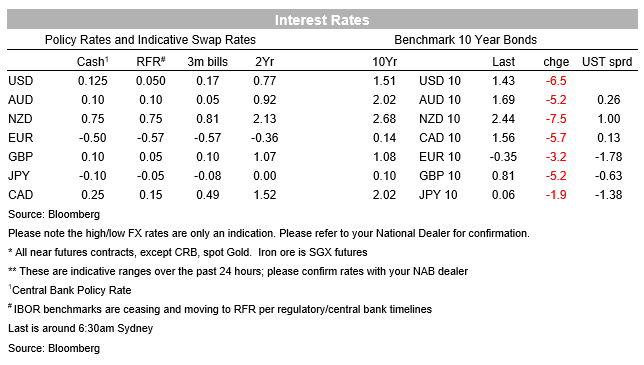

It has been a volatile session overnight driven by differing headlines around vaccine efficacy, capped off by very significant hawkish tilt by US Fed Chair Powell in Senate Testimony. Of importance, Chair Powell said it was time to “retire that word [transitory]” and with “inflation pressures are high” will “consider wrapping up the taper of our asset purchases…perhaps a few months sooner ”. An accelerated taper profile that ends in say March 2022 (rather than June) would open up the possibility of more than 2 rate hikes in 2022. Curves quickly flattened with the 2/10s falling -9.2bps to 91.16bps, driven by higher 2 year yields and a lower 10yr yield (-5.8bps to 1.44%). The move in nominals outpaced TIPs, meaning the 10yr implied inflation breakeven fell -4.6bps to 2.51%. A more hawkish Fed may also mean the Fed does not need to raise rates as far with the 5Y1Y OIS terminal rate proxy -11.3bps to 1.49%.

Equity markets are down sharply with the S&P500 so far down -1.6%. Around 0.8 percentage points of that decline came from the headlines around Moderna, with a decent recovery of 0.6 percentage points after more hopeful comments by BioNTech, before falling sharply by 1.5 percentage points after US Fed Chair Powell’s hawkish comments (see below for the vaccine headline details). Powell’s “Road to Damascus” conversion on inflation is significant, with the Fed turning hawkish given inflation has persisted far longer than they had thought. Powell also noted as we had with the rise in the Dallas Fed’s Trimmed Mean PCE, that “…it’s also the case that pricing increases have spread much more broadly ” in recent months. It’s no surprise then to see the tech sector being hit to a similar degree to the rest of the index (NASDAQ -1.5%)

As for vaccine headlines, it was clearly risk-off at the end of Asia yesterday after Moderna’s CEO sounded caution on the likely efficacy of vaccines against the Omicron variant: “There is no world, I think, where [the effectiveness] is the same level . . . we had with [the] Delta [variant],” and “I think it’s going to be a material drop. I just don’t know how much because we need to wait for the data. But all the scientists I’ve talked to . . . are like, ‘This is not going to be good’.” (see FT Interview with Moderna’s CEO). That risk-off sentiment though stabilised in early New York trade with BioNTech’s CEO taking a more hopeful: “Our belief [that the vaccines work against Omicron] is rooted in science: If a virus achieves immune escape, it achieves it against antibodies, but there is the second level of immune response that protects from severe disease—the T-cells,” (see WSJ: Omicron Unlikely to Cause Severe Illness in Vaccinated People).

We will have to wait for two weeks to get data on how the existing vaccines perform against the new variant, and also to make some assessment on the severity of the disease. Data so far is mixed. COVID-19 antibody drugs by Regeneron lose effectiveness against Omicron according to preliminary testing (see WSJ: Covid-19 Antibody Drugs Are Challenged by Omicron, Preliminary Testing Indicates ). While in South Africa hospitalisations are acting like prior waves, but the split between vaccinated/unvaccinated is favourable with 88% being unvaccinated so far. There are though some concerns around elevated cases for children, particularly under 2 years, but there is nothing concreate so far. As for economic implications, Fed Chair Powell downplayed the risk, saying that “I’m not thinking that the effects on the economy will be remotely comparable to what happened last March”.

FX moves have been mixed. Heading into Powell’s Senate hearing, the USD was on a weaker footing. The USD strengthened after Powell spoke, but the BBDXY USD has pared some of that recovery and is now slightly lower for the day to be -0.2%. A cautious risk-off tone clearly remains with USD/Yen -0.5% to 113.18 and USD/CHF -0.6% to 0.9186, while EUR appears to have got some support +0.4% to 1.1312. Commodity currencies have been amongst the worst performing overnight, but have come off their lows. On a 24 hour view point the AUD is down -0.2% to 0.71 after having printed a fresh low for the year of 0.7063. The NZD is up 0.2% overnight to 0.6810, essentially back to where it was this time yesterday, after printing a fresh low for the year of 0.6773 in the aftermath of Powell’s comments.

Data overnight was mixed, but not market moving. Eurozone inflation printed hotter than expected with Core HICP at 2.6% y/y against 2.3% expected. The US Conference Board’s Consumer Confidence Index printed slightly weaker at 109.5 against 110.9 expected, but overall remains much higher than the alternative University of Michigan Consumer Sentiment survey. The Chicago PMI, the last regional survey before the much more important ISM, also disappointed at 61.8 against 67.0 expected. MNI who sponsor the Chicago PMI noted it was the lowest reading since February with a slowdown in new orders being seen, though new orders overall remains very healthy at 58.2. Canada’s GDP bounced back a stronger than expected 5.4% annualised in Q3 (consensus 3.0%) on the economic re-opening, but this followed a downwardly revised 3.2% contraction in Q2 from the initial estimate of -1.1%. China PMIs reported yesterday also came in slightly ahead of expectations.

Omicron headlines to dominate risk sentiment. In terms of data Australia has Q3 GDP figures which will likely be ignored given that references a period in which NSW, VIC and the ACT were in lockdown. Offshore the most interesting pieces are in the US where there is a quadruple of events which include ADP Payrolls, ISM Manufacturing, Beige Book & Fed Chair Powell giving his second round of congressional testimony. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.