NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The negative vibes from our APAC session extended overnight with softer than expected US data releases not helping the cause. US retail sales were broadly softer, and the NAHB housing market index also came in weaker than expected.

https://soundcloud.com/user-291029717/will-rbnz-still-hike-rates-today-even-in-a-lockdown?in=user-291029717/sets/the-morning-call

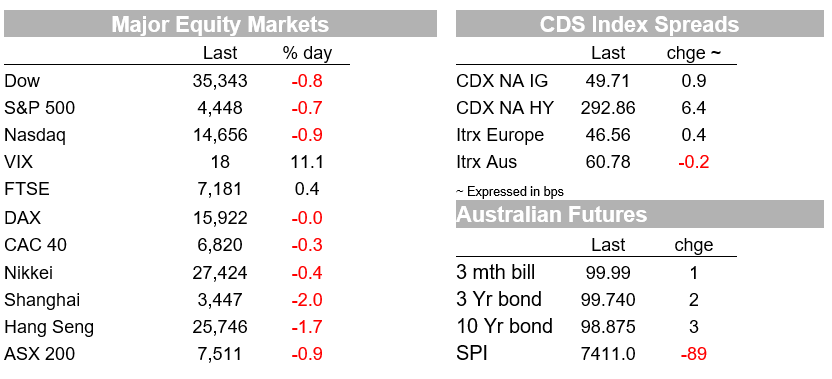

The negative vibes from our APAC session extended overnight with softer than expected US data releases not helping the cause. US retail sales were broadly softer, and the NAHB housing market index also came in weaker than expected. US equities end the day sharply lower while the US bond market was seemingly more prepared for the softer number with the 10y UST yield edging higher after the data releases. A safe-haven bid boosted the USD across the board with the kiwi leading the G10 decline over the past 24 hours, following yesterday’s news of a covid outbreak and lockdowns announcement, leaving today’s RBNZ policy decision poisely balanced, will the stay or will they go? NZD has found a base just above 69c while the AUD makes a new YTD low.

Yesterday, market sentiment was showing signs of strain with China’s equity market leading the declines in our APAC regions. The CSI 300 index ended the day 2.10% lower with industrial stocks reflecting concerns over the slowdown in activity while the tech sector was also under pressure following China’s market regulator issuance of draft rules on unfair competition on the internet.

European equities ended the day marginally lower (FTSE 100 the exception up,0.38%) while US equities endured a sharper decline. The softer than expected July retail figures set the tone at the NY open, but the US equity slide extended into the afternoon session ahead of a small recovery before the close. The S&P 500 ended the day 0.71% lower, after losing almost 1.40% intraday. The NASDAQ closed -0.9% while the Dow was -0.79%.

US retail sales for July undershot market expectations, with the headline figure down 1.1%, dragged lower by auto sales, while the ex-autos figure was also weak, down 0.4%. The fall in sales was led by a decline in spending on homes and cars, following a rise in the previous month. Sales of cars and auto parts were down 2% in July, as the prices of used and new cars continued to climb amid higher demand and lower supply of vehicles. Meanwhile, sales of furniture, sporting goods and building materials declined as home prices continued to rise. Of note, however and in contrast to the decline in consumer confidence reading released on Friday, the increase in US covid infections did not stop the US consumer from going out with sales at restaurants and bars increasing in July. That said the turn in consumer confidence may by a sign of what is yet to come and with fall also approaching, diners could turn more reluctant to eat outside.

Adding to the gloom, the NAHB housing market index also came in weaker than expected , unexpectedly dropping to a 13-month of 75, even though mortgage applications data have been pointing to a significant housing market slowdown for some time. A weaker than expected result Home Depot didn’t help either, a further indication of some housing market softness. NAHB’s chief economist pointed to higher costs and material access issues holding back home sales.

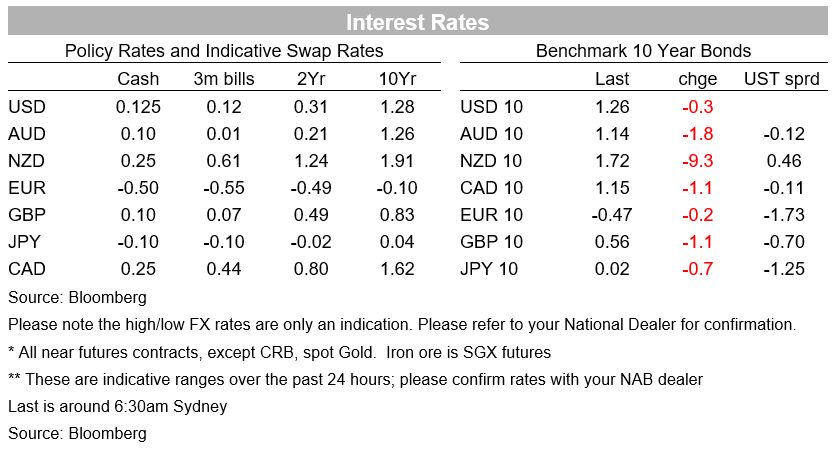

The rates markets reaction to the softer than expected US data flow was somewhat surprising. 10y UST yields jumped higher after the retail sales report, suggesting bond investors were well prepared for a soft number following the plunge in consumer sentiment. Trading at their low for the day of 1.22% ahead of the release, the yield jumped as high as 1.27% and is currently 1.26%, barely lower for the day. Fed Chair Powell spoke to educators at a town hall meeting but his opening address didn’t touch on the economy or monetary policy. Some Q&A touched on the economy, but nothing of note for the market.

Meanwhile in FX land, the USD enjoyed a safe haven bid on the back of softer US data releases and risk off reaction evident in the equity markets . The greenback recorded gains across the board with the both the DXY and BBDXY indices up around 0.55% over the past 24 hours. Looking at majors, the Euro fell around 0.6%, trading to an overnight low of 1.1706 (now at 1.1710) while GBP fell 0.8% to 1.3741. A stronger UK labour market report didn’t elicit much of a market reaction, numbers need to be taken with a pinch of cautiousness given the furlough scheme runs to the end of September with over 1 million still on the scheme. Market is waiting for the new quarter figures to get a better feel of the state of the UK labour market.

Yesterday the announcement of a community case of COVID19 in Auckland triggered an outsized market reaction, with an immediate fall in the NZD and rates , cumulating to a 14bps plunge in the 2-year swap rate from 1.40% (having nudged higher earlier in the day) to 1.26%, with the market dialling back its expectations of near-term OCR hikes. The NZD traded from 0.7029 early yesterday to an overnight low of 69c, and ahed of the RBNZ today the pair appears to have found a base just above the figure, now trading at 0.6919.

My BNZ colleague Jason Wong notes the timing of the COVID19 case couldn’t come at a worst time for the RBNZ, one day ahead of its MPS , most of which would have been already written. Importantly, the MPC still has time to reassess any initial judgements, including the important rate decision. August OIS closed at 0.44%, implying 19bps of hikes priced for the meeting, down from the 30bps of hikes priced earlier in the day, but the market close was before the country-wide level 4 lockdown was announced, so rate hike expectations have likely been reassessed downwards since (see more below).

The AUD has trended lower, showing some weakness after the RBA minutes were released, with the market latching onto the headline that said “the Board would be prepared to act in response to further bad news on the health front should that lead to a more significant setback for the economic recovery”. The currency has traded to a fresh low of 0.7243 overnight and now trades 10bps higher at 0.7253.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.