NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The Fed’s board continues to talk down the prospect of tapering, pushing the argument that price rises will be transitory.

https://soundcloud.com/user-291029717/will-the-bank-of-england-taper-before-the-fed?in=user-291029717/sets/the-morning-call

It’s gettin’ hot in here (So hot)

So take off all your clothes (Ohh) – Nelly

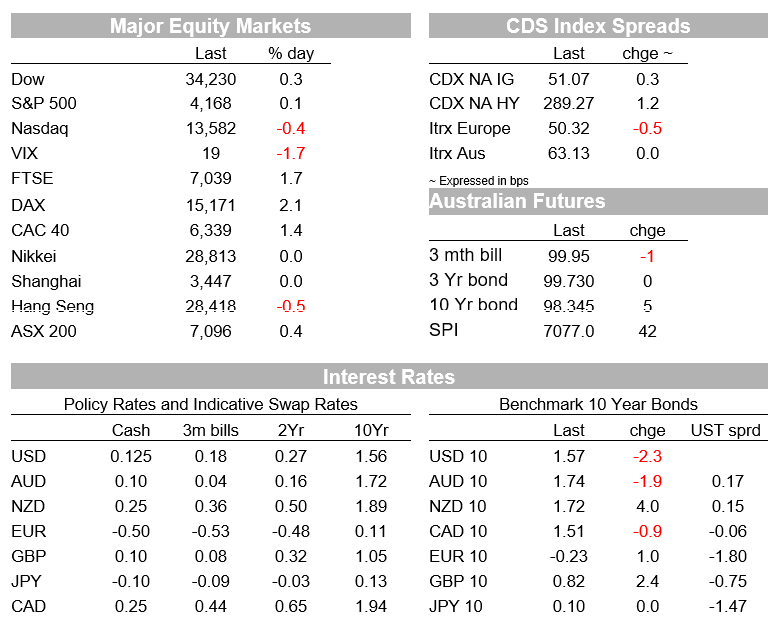

Procyclical sectors led a decent rally in European equities against a backdrop rising inflation expectations and firm commodity prices. US equities closed mixed with the NASDAQ struggling again. The ISM Services index ease from record levels but prices paid rose again. Ahead payrolls tomorrow, the USD is little changed, but AUD and NZD outperform.

The performance board reveals contrasting fortunes between European and US equities . Procyclical sectors have led a decent rally in Europe with the Stoxx Europe 600 Index up 1.8%. Miners spearheaded the charge, jumping 4.7% while Energy shares climbed 2.89% and IT added 2.73%. On the other side of the Atlantic, the S&P 500 shows modest gains (+0.07%) with Energy (3.33%) and Materials (1.32%) up, but Utilities and Real Estate the big struggles, down 1.71% and 1.52% respectively. Meanwhile the NASDAQ has closed in negative territory for a fourth consecutive day, down 0.37%

The April ISM Services was the data release to watch overnight and although it came below expectations, printing at 62.7 vs. 64.1 expected, the index remains at exceptionally strong levels (the second highest on record). Market reaction to the survey release was rather muted, details showed the April drop was due to declines in orders, down 4.0 points, and business activity, down 6.7 points. However, Prices Paid continue to increase at a faster pace ( 76.8 in April from 74 from March) while in the same vein as increased prices, supplier deliveries continue to lengthen and boost the overall ISM reading (but in a negative way) at 66.1 from 61, reflecting supply disruptions.

Ahead of payrolls tomorrow, movements in nominal UST yields have remained fairly subdued with the 5y and 10y tenors easing just over 2bps to 0.792% and 2.5695% respectively. Of more interest however, the breakeven components have continued to edge higher with the 5y and 10 BEIs up around 4bps over the past 24 hours. The 5y BEI now trades at 2.71% a level not seen since 2008 while it only seems to be a matter of time for the 10y BEI to reach 2.50%, now at 2.4744%. The flip side to all these moves is that the decline real UST yields which began at the start of April is now accelerating at the start of May. This real yield decline has coincided with a reversal in fortunes for the USD, the 10y real yield started April at -0.63%, began May at 0.77% and now trades at -0.90%.

Despite constant reassurances from Yellen and an array of Fed officials that the coming increase in inflation will prove ‘transitory’ (Chicago Fed President Evans overnight said he thought the risk of a major inflation overshoot was “remote ”), markets are evidently a bit more worried. Options prices indicate that the market see a greater than one-in-three chance than US CPI could average more than 3% over the coming five years.

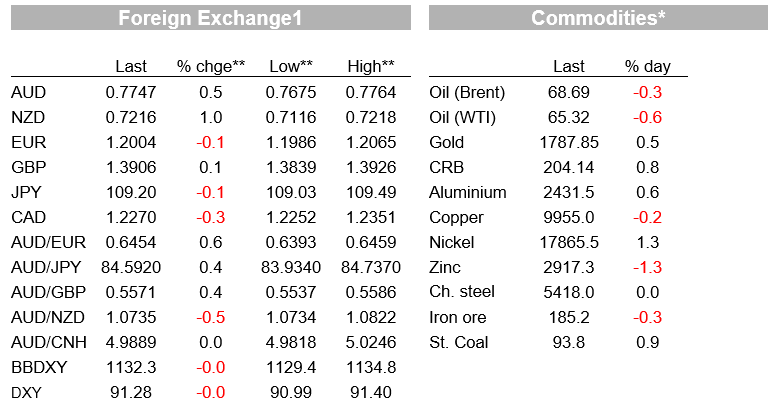

Strong commodity prices have been a factor that has helped to lift inflation expectations . The Bloomberg Commodity index reached its highest level since 2011 yesterday. Copper prices traded above $10,000 again overnight while oil prices retained most of their gains from the previous session after US DOE data showed a much larger than expected oil inventory drawdown (almost 8 million barrels). The Energy and Materials sectors have led gains on the S&P500 overnight.

Moving onto currencies, the USD is little changed with the DXY index at 91.26 while the BBDXY index is at 1132.25. Commodity linked currencies have made same gains against the USD with NZD leading the charge, up 1% and now trading at 0.7216 . Yesterday’s solid labour market has helped the kiwis fly. NZ’s Q1 labour market report showed a fall in the unemployment rate from 4.9% to 4.7% (lower than both the RBNZ’s and the market’s expectations) and stronger-than-expected employment growth of 0.6% in Q1. Wage growth remains relatively modest, for now, with the labour cost index increasing just 0.4% on the quarter and 1.6% on a year ago.

My BNZ colleague Nick Smyth notes that the RBNZ will no doubt argue that employment is still some way from its maximum sustainable level, it’s closer than what it was and appears to be moving in the right direction. BNZ thinks the unemployment rate is likely to keep declining amidst robust business hiring intentions and, in combination with rising inflation pressures, this will likely see the RBNZ start to raise the OCR next year.

The firm commodity backdrop has also helped the AUD perform, up 0.5% and now trading at 0.7742, around the middle of the 0.7675 to 0.7818 range that has confined the pair since mid-April. Our fair value models continue to suggest the AUD is starting to look undervalued at current levels, favouring our view for the pair to test the 80c level around mid year.

Looking at other G10 pairs, CAD is up 0.33% while other pairs most other currencies are +/-0.2% from this time yesterday. GBP is the one to watch tonight with the BoE policy meeting and the Scottish Parliament election. The BBC notes opinion polls suggest support for independence rose above 50% to its highest ever level last year. It has since fallen back somewhat but there are clearly underlying reasons why so many voters still want to leave the UK.

In other news President Joe Biden’s chief trade negotiator, Katherine Tai, said the Biden administration respects the continuity of the so-called China phase-one agreement. The US can’t shy away from being tough on China, but must be fair adding that the relationship between the nations is likely to be a mix of competition, cooperation and confrontation, with the US looking to work collaboratively with Beijing on climate issues for instance.

In a positive step for EM nations fighting the pandemic, Tai also said the US will support a proposal to waive intellectual-property protections for Covid-19 vaccines, aimed at increasing global supply and access to the life-saving shots as the gap between rich and poor nations widens. However, she acknowledged the talks will take time and “will not be easy,” given the complexity of the issue and the fact that WTO is a member-driven organisation that can only make decisions based on consensus.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.