Online retail sales growth slowed in May following a fairly strong April

Insight

It has been all about the ECB and Fed overnight with the former delivering a jumbo hike and hinting at more to come while Fed Chair Powell reiterates commitment to act forcefully against inflation

Events Round-Up

NZ: Manufacturing sales vol. (q/q%), Q2: -4.9 vs. -3.4 prev.

AU: Trade balance ($b), Jul: 8.7 vs. 14.7 exp.

EC: ECB deposit facility rate (%), Sep: 0.75 vs. 0.75 exp.

US: Initial jobless claims (k), 3-Sep: 222 vs. 235 exp.

It has been all about the ECB and Fed overnight with the former delivering a jumbo hike and hinting at more to come while Fed Chair Powell reiterates commitment to act forcefully against inflation. Equity markets take the CB news in their stride with EU and US indices posting modest gains. Europe leads rise in core global bond yields with Australian bonds the exception after RBA Governor Lowe makes the case for slower pace of rate hikes ahead. FX moves are relatively subdued, Euro recovers some ground post ECB, AUD and NZD range trade while JPY ignores threat of intervention.

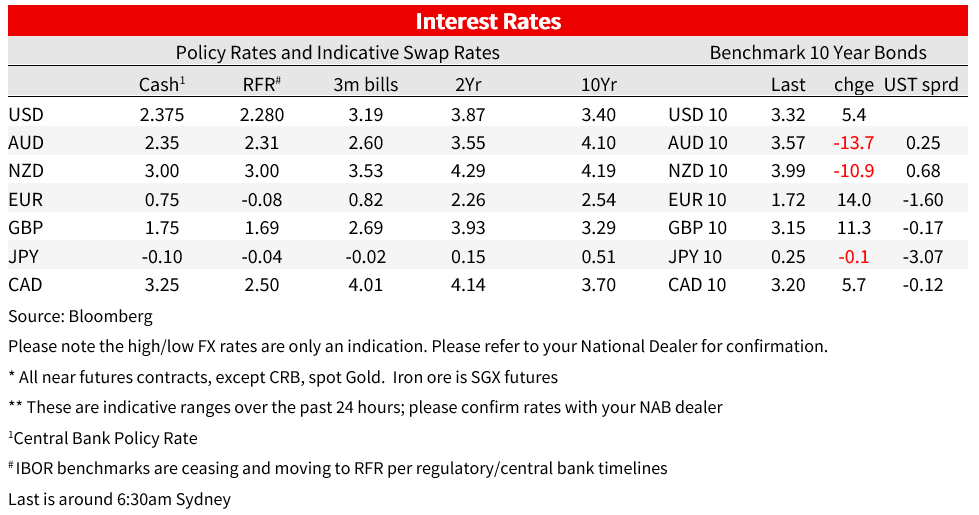

Overnight the ECB hiked its Deposit Rate and Main refinancing Rates by 75bps to 0.75% and 1.25% respectively, in line with NAB’s and the majority view. The ECB Statement noted inflation was “far too high” and speaking at her press conference, ECB President Lagarde made it very clear that more hikes should be expected, stressing that the current policy setting is too far away from a rate that will achieve a 2% inflation target. President Lagarde noted the reference to several meetings meant “probably more than two, including this one, but it’s probably also going to be less than five”.

Supporting the rate hike and forward guidance, the new ECB forecast (unsurprisingly) revealed a downgrade to the 2023 growth outlook and an upward revision to the inflation profile. The 2022 growth forecast was revised up, reflecting a stronger 22H1 than expected (to 3.1% from 2.8%), but 2023 was downgraded to 0.9% from 2.1% and to 1.9% in 2024 from 2.1%. Looking at the details and in a classic case of Central Banks looking at the economy with a glass half full, the next 3 quarters (22Q3-23Q1) were marked much weaker (from 50bp per quarter to zero), avoiding negative numbers. No energy means no growth, so not sure how one can square this circle, specially now that we must add an aggressive policy tightening on top of it.

As for the inflation numbers, the ECB raised its forecasts, pushing 2022 to 8.1% from 6.8%, 2023 to 5.5% from 3.5% and 2024 remaining at 2.3%. The ECB said risks to inflation were on the upside while risks to growth were primarily on the downside. In its non-base case downside scenario, the ECB said growth would be -0.9%, noting a long-lasting war in Ukraine remains a significant risk to growth

Answering to a question on terminal rate and neutral, Lagarde said ‘“I am not scratching my head around the neutral rate versus the terminal rate” instead she stressed the ECB desire to head towards that 2% medium-term target. This hawkish outlook triggered a sell-off in core global bond yields led by European counter parts. Germany’s 2-year rate up a massive 22bps and 10-year rate up 14bps to 1.71%. 10y gilts and BTPS rose 11bps to 3.147% and 3.964% respectively.

The move up in yields was also turbo charged by the fact Fed Chair began speaking a few minutes after ECB Lagarde’s press conference had begun. Powell reiterated his hawkish message from Jackson Hole, stressing that “We need to act now, forthrightly, strongly as we have been doing,”. Adding that the “The Fed has and accepts responsibility for price stability,” Powell also noted that history cautions against prematurely loosening policy. Supporting his rhetoric Powell also reference the strength of the US labour market noting “Demand is very, very strong still”. The data flow overnight reinforced this point with US jobless claims falling to 222k, its lowest level since May. Claims are reliable US cyclical indicator and continue to suggest tightens in the US labour market.

Another important point made by Fed Chair Powell and consistent with a theme we have been stressing in FX strategy (slower growth and higher unemployment a necessary evil to bring inflation to heel), the Fed Chair emphasised that “By our policy interventions, what we hope to achieve is a period of growth below trend, which will cause the labor market to get back into better balance, and that will bring wages back down to levels that are more consistent with 2% inflation.”

Markets are interpreting softer activity data as a trigger for a possible central bank pivot, but the message from the Fed and now from the ECB, is that the only thing that matters is drivers that will bring inflation to heel. The Powell ‘s remarks added to the move up in core global bond yields, with the 2y UST yield ending the day 5.5bos higher whole the 10y Note closed at 3.317%, 2.5bps higher on the day.

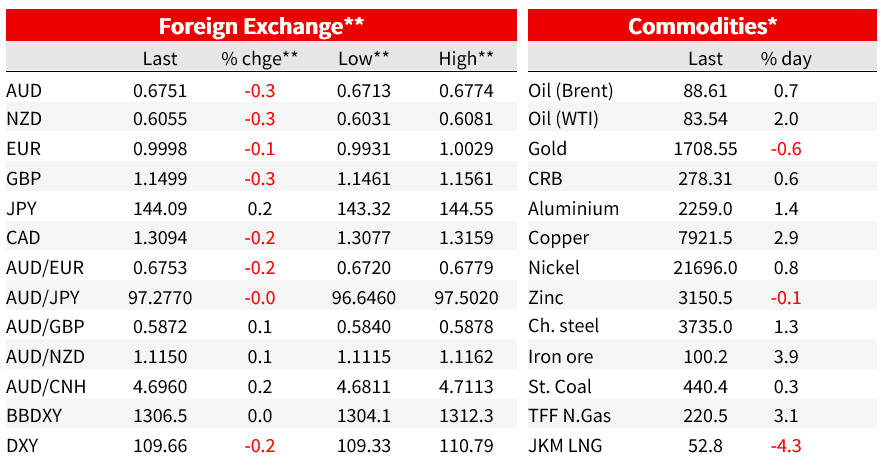

Meanwhile in FX land, the Euro struggled to rise after the ECB with Powell’s hawkish remarks a counter force. Just before the ECB announcement the euro traded to an overnight high of 1.0029 with Powell pushing the pair down to 0.9931, before recovering to 0.9997 where it currently trades.

The AUD regained the ground lost after the dovish take on Governor Lowe’s speech (see below) and currently sits at 0.6754, both antipodean currencies are down between 0.4% and 0.3% relative to levels this time yesterday. GBP is also lower (0.25% to 1.1154) with the market showing little reaction to UK PM Truss announcement of her much-anticipated energy package . Although specifics of how the scheme will operate remain vague, its core element is that energy prices will be allowed to rise by just 23% in Oct (rather than the scheduled 80%) and will then be capped through Sep ’24. In addition, similar supports were announced for businesses, but extending over just a 6m horizon. The policy is expected to reduce inflation by 4-5 percentage points and while the cost will depend on how gas prices fare, the current estimate is around £150b ( potentially 5% to 6% of GDP).

The other notable mover has been the yen, down another 0.25% to £144.08 and showing little reaction to the step up in rhetoric by government officials hinting at possible direct market intervention. History shows this is a futile exercise, unless done in coordination with other governments and currently it is hard to see the US and others interested in cooperating. The only one that can save the yen from spiralling out of control is the BoJ, but the incentive to do so remains unclear, notwithstanding the cost to household cost of living.

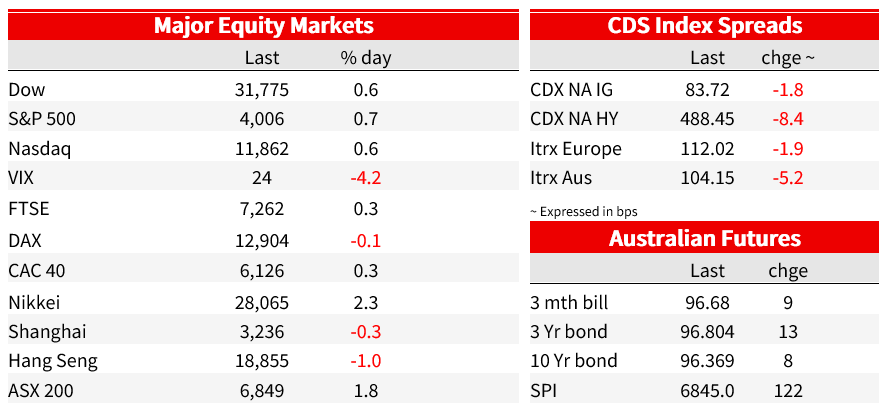

As for the RBA yesterday, the market had a dovish take on RBA Governor Lowe’s key post-meeting speech where he said that “…the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises”, although he added that the tightening from here would be “guided by the incoming data and the evolving outlook for inflation and the labour market”. His comments supported widespread views that a step down to hiking in 25bps increments might be imminent. Soon after, the Australian 3-year bond settled about 10bps lower in yield, but that move has reduced to 5bps with global forces back in charge.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.