The NAB Consumer Stress Index has eased to a 2-year low and marks its 50th iteration.

Insight

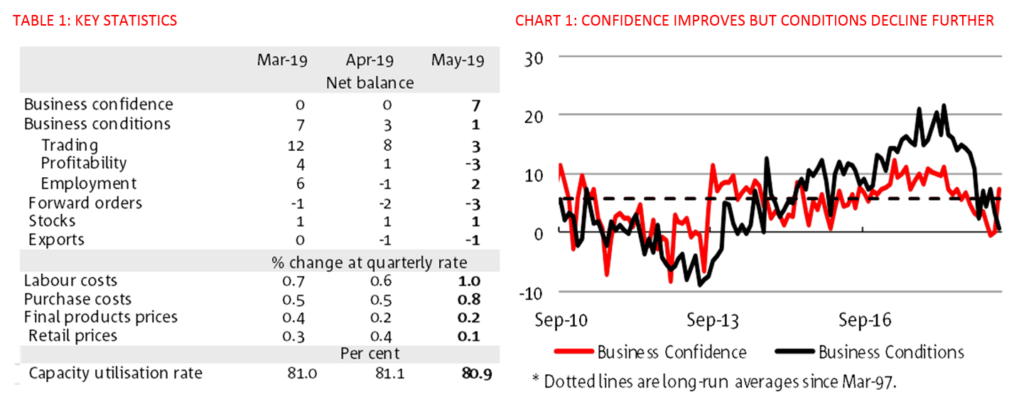

Confidence saw a post-election spike in May but conditions decline further with the private sector continuing to lose momentum.

Business conditions weakened further in the month and are now well below average – the key message remains that the private sector continues to lose momentum. The goods distribution industries (especially retail – which is clearly in recession) remain particularly weak, and manufacturing is not far behind. The services industries appear to be holding up better but have also seen a deterioration over the past year. By state, NSW continues to be the best performer on the mainland, while Tas also continues a strong run of readings. WA has weakened notably in 2019, despite the mining sector showing strength. Business confidence saw a post-election spike in May (while the Survey was sent out on 14 May, interviewing started on 20 May) while expectations of rate cuts may also have helped. However, the increase may not persist with other forward-looking indicators remaining weak. Worryingly, forward orders declined further, and capacity utilisation is now a touch below average. With activity continuing to lose momentum, and capacity utilisation declining, the survey continues to show weak price pressure across inputs and final products.

Podcast

Our podcast series to accompany the NAB Monthly Business Survey continues, giving you a 10 minute summary of the key survey developments this month. Listen now.

Key highlights

Business conditions fell 2pts to +1 index point in May. The fall was driven by a decline in profitability and trading sub-components (profits down 4pts to -3 index points and trading down 5pts to +3 index points). The employment index rose to +2 index points in the month, following the sharp decline last month. At these levels the trading and profitability indexes are well below average, while employment is now around average. Each component remains well below the levels of a year ago. Business confidence rose sharply in the month (+7 index points) but is unlikely to persist at these levels given the weakness in other forward-looking indicators.

According to Alan Oster, NAB Group Chief Economist “Business confidence saw a sharp increase in the month following the Federal election and a confirmation from the RBA that rates would be cut in June. We think this will be a short-term spike given other forward-looking indicators saw further deterioration in the month. Forward orders declined further and in addition to being well below average are negative. Capacity utilisation has also pulled back in 2019 to date and is now a touch below average”.

“While confidence, at least at face value was a positive outcome, business conditions deteriorated further. Trading conditions and profits are particularly weak. The employment index which we are watching closely, partially reversed some of its decline last month, but is only around average” said Mr Oster.

In the month, business conditions declined across all states except Queensland (increase) and Western Australia which was unchanged. In trend terms, conditions remain highest in New South Wales, followed by Victoria and South Australia. Western Australia is weakest – and negative – after having weakened recently.

“Conditions have weakened across all states over the past year though NSW, VIC and SA are most favourable in trend terms. Of some concern is the recent deterioration in WA which is now negative, despite the mining sector still showing strength” Mr Oster said.

“Across industries we continue to see the best conditions in mining and the services sector – recreation & personal, and finance, business & property services. The goods distribution industries, including wholesale and retail remain weakest” Mr Oster said.

The service sectors continue to show the best conditions with goods distribution industries such as retail and wholesale having deteriorated sharply over recent months. In addition to the weakness in the goods distribution, manufacturing is now negative. Mining remains the most positive with conditions at high levels in the sector.

“While the retail industry has lagged the other sectors for some time, the recent deterioration has seen conditions in the industry fall to levels not seen since the GFC. This suggests that the consumer remains highly cautious with anything but spending on essentials because of ongoing slow income growth, high debt levels and possibly some concerns over falling house prices” Mr Oster said.

“Forward-looking indicators suggest that the bounce in confidence is likely to be short-lived and that conditions are unlikely to turn around any time soon. We will also continue to closely watch the employment index for a lead on any turning points in the labour market” said Mr Oster.

For more information, please see the:

The NAB Consumer Stress Index has eased to a 2-year low and marks its 50th iteration.

Insight

Change is a constant in our global environment, but that's all the more reason to keep moving forward on your terms.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.