NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

No respite from rising Treasury yields – 10s up another 4bps to 2.70% +32bps on week further hurting tech. stocks/NASDAQ vs other indices and boosting USD DXY index to 100.

https://soundcloud.com/user-291029717/rates-push-ever-higher-as-food-prices-soar?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

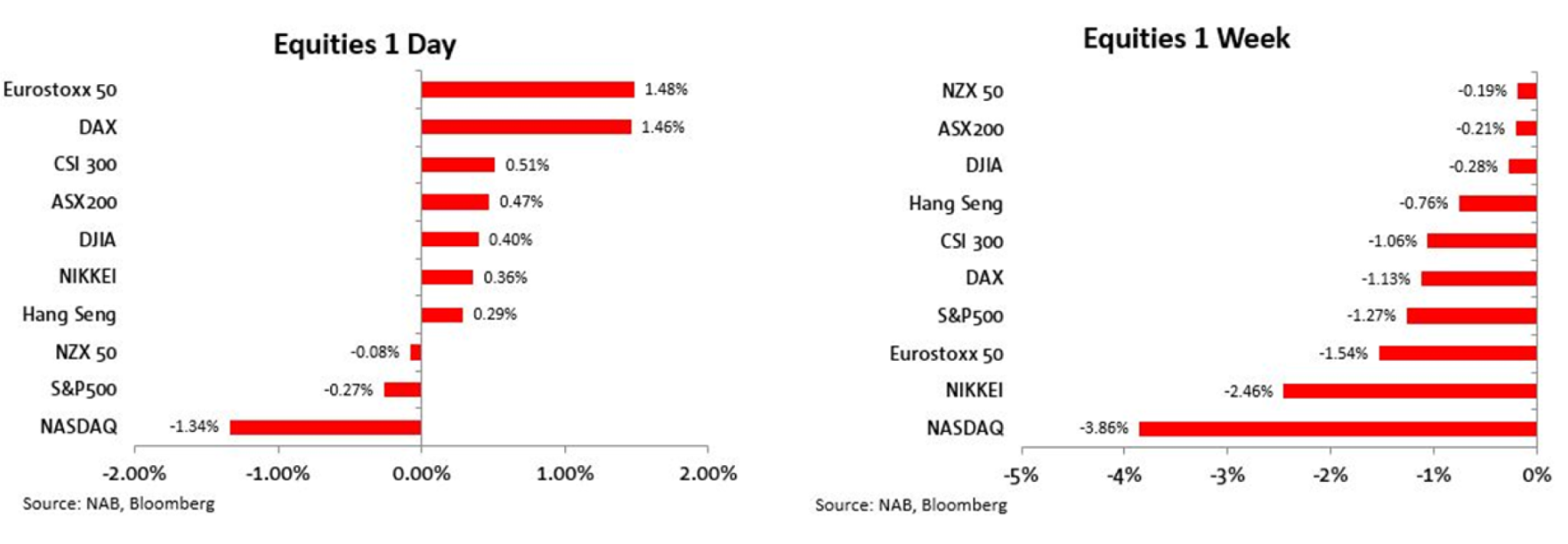

Like yesterday’s Formula 1 winner Charles Leclerc, the US Treasury market remains firmly in the global markets box seat on Friday, driving much of the volatility across all asset classes. 10-year yields rose another 4bps and hit 2.70% for the first time in the cycle. In turn this dragged the rates-sensitive US tech sector lower, the NASDAQ ending Friday down 1.3% versus only 0.3% for the S&P 500 and after the Eurostoxx 50 earlier ended +1.6%.and the UK FTSE more than 2%. JPY and GBP were the main contributors to a further lift in the USD, DXY briefly exceeding 100 for the first time since 15 May 2020 before ending the week at 99.80. AUD lost another 0.3% to 0.7458, finishing the week more than two cents off Tuesday’s post-RBA meeting high.

No respite from the US bond market sell-off on Friday with yields up 4-5bps across the curve bringing the back up in 10-yar yields over the week to 32bps (n the 30-year yield on which most mortgage rates are set in the US, up 29bps). 2s added the most (5bps) for a very slight curve flattening but this can’t disguise the significant re-steepening in the cure over the course of the week (around 23bps for 2/10s).

There was no US data of note out on Friday but Federal Reserve Bank of Chicago President Charles Evans and his Atlanta colleague Raphael Bostic spoke at a ‘inclusive employment’ event hosted by the Chicago Fed on Friday and both said they favour raising rates to neutral, while cautioning that they will monitor how the economy performs as they proceed. “We are in the middle of adjusting monetary policy from our very accommodative stance after Covid towards a neutral setting by the end of the year probably, certainly early next year depending on what the pace will be”, Evans said. “I am of the opinion that a lot of what we see are supply chain issues and that those are going to come off the boil. It is still going to take longer than I thought initially, with the chip shortages and all kinds of things…I am optimistic that we can get to neutral, look around and find that we are not necessarily that far from where we need to go”.

Bostic meanwhile said “I think it is fully appropriate that we move our policy closer to a neutral position. But I think we need to do it in a measured way…..we are going to learn a lot as we go through this year. With the reduction in the fiscal stimulus and that waning over time, that is also going to lead to a pullback in aggregate demand in ways that should allow the demand and the supply responses to start to come closer to each other”. Neither Bostic nor Evans are 2022 FOMC voters, while note that judging from the median FOMC member ‘long run’ dot in the March Summary of Economic projections (SEO) neutral is currently deemed to be 2.40%.

Also on the central bank front ,The European Central Bank will do “whatever it takes” to stop an inflationary overshoot becoming permanent, ECB Governing Council member and Bank of Greece Governor Yannis Stournaras said Friday, echoing the historic speech of Mario Draghi a decade ago. “We’ll do whatever it takes — and I’ll stop here as we’re in a silent period — not to let temporary inflation becoming structural and permanent”. There are “a series of supply side shocks, the pandemic could not be foreseen, the war could not be foreseen,” Stournaras said. “It’s creating very high spot inflation. We could kill it if we wanted to in a month,” but it would also kill the economy, he added.

We also had a Bloomberg source story Friday saying that the ECB is working on a crisis tool to deploy in the event of a blowout in the bond yields of weaker euro-zone economies, according to officials familiar with the plans. The institution’s staff is designing a backstop that would be available for the Governing Council to use against debt-market stress caused by shocks outside the control of individual governments, said the officials, who asked not to be identified because the matter is confidential. The report says it’s not clear what the tool would look like, though such an instrument would presumably involve bond purchases in some form to contain yields. The report hit an hour in front of the Eurozone bond market close, and saw the likes of 10 year BTP yields off 5bps (from 2.40% to 2.35%) but the move was reversed in to the close, perhaps viewed on refection as something on a non-story.

The one piece of significant economic news Friday night was Canadian Employment, which jumped by 72.5k in March, close to expectations and following the bumper 336.6k February gains, while the unemployment rate fell by a tenth more than expected to 5.3% from 5.5%. Hourly wage rates were up 3.7% in the year to March as expected and up from 3.3% last time. The data cements the case for the Bank of Canada going by 50bps when it meets on Thursday. Indeed money markets ended Friday pricing slightly more than a 50bps increase.

Equity markets put in a mixed performance Friday, all European and APAC indices finishing higher, including a 1.5% gains for the Eurostoxx 50, but US stocks suffering under the weight of the latest rise in Treasury yields, the NASDAQ (-1.3%) more so than the S&P 500 (-0.3%). On the week though, it was a down-week all round, but again the more interest rate sensitive US tech. sector faring worse (NASDAQ -3.9%, Eurostoxx 50 and S&P500 sown 1.5%an 1.2% respectively while the ASX 200 was off just 0.2%).

In currencies, the AUD gave back a little more of its run up to 0.7661 seen soon after last Tuesday’s RBA meeting and pivot away from using the word ‘patient’ to describe its policy disposition. AUD/USD lost 0.3% to 0.7458. AUD has opened the week in Wellington softer still, after Australian Prime Minister Scott Morrison yesterday called the Federal Election for Saturday March 21, the last possible date and so kicking off a relatively long six-week election campaign. This morning’s Newspoll opinion poll puts Labour 8 points ahead of the Coalition, 54/46% (a slight narrowing) while PM Morrison has edged ahead of his opponent Anthony Albanese as preferred prime minister, 43% to 42%.

In contrast the EUR has opened about 0.5% stronger against the USD. This is after the first round of voting on Sunday in France’s Presidential elections, where incumbent Emmanuel Macron has won around 28% of the vote with far-right (but of late somewhat less far right) challenger Marine le Pen in second place on about 24%. The Euro has opened more than 0.5% higher in Wellington on the view that the result bolsters the likelihood of Macron being re-elected President in the second round run-off election on April 24. That said, an Ifop poll of 968 people on line in the hour after the first round of polling ended Sunday shows Macron leading Le Pen by just 51% to 49%.

The USD ended Friday little changed, but only after the DXY index pierced the 100 level for the first time since 15 May 2020, with gains against every G10 currency bar the NOK. Still rapidly rising US yields look to be the key USD driver here and high, lifting the DXY up 1.2% on the week and the broader BBDXY by 1.1%. The opening gains for EUIR/USD have reduced a weekly loss of 1.5% to about 1%.

In other weekend news, China’s President Xi Jinping on Saturday praised his country’s handling of the Covid pandemic, even as Shanghai reported record case numbers. Speaking at an event marking China’s hosting of the Winter Olympics, Mr Xi said some athletes said China deserved a gold medal for its approach. Mr Xi said China’s zero Covid policy had withstood the test of the Winter Olympics. There is little sign of China changing its approach. An editorial in state news agency Xinhua said the country would “firmly adhere” to its policy. “It will not be long before Chinese citizens affected by the virus can enjoy warm sunshine in spring days as things get back to normal,” it said. (BBC). His comments come as reports filter through of badly disrupted food supplies causing waves of anxiety among Shanghai residents. On the weekend, Shanghai reported more than 25,000 covid cases for Saturday.

Weekend Australian auction results showed the combined capitals recording the busiest week of the year to date and the sixth busiest auction week since CoreLogic records commenced in 2008. Auction activity was up 24.1% compared to the week prior. The preliminary clearance rate fell back below 70%, with 68.7% of the 3,073 results collected so far returning a successful result. Melbourne recorded a preliminary clearance rate of 68.6% against last week’s preliminary 69.1% and 67.0% final, while Sydney’s preliminary clearance rate of 65.1% compared to last week’s preliminary 68.2% and 63.8% final.

Finally, in commodities thermal coal (+12.7% on the week) was the standout mover in a week that saw ethe EU agree to ban the import of Russian coal. In contrast, iron ore was the worse performing commodity, down 3.9%. Oil was up over 2% Friday but -1% (WTI) and -1.5% (Brent) on the week.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.