The NAB Consumer Stress Index has eased to a 2-year low and marks its 50th iteration.

Insight

Australia’s GDP continues to grow in spite of subdued wages growth and consumer spending. Gaining a greater understanding of how these contradictory trends break down across regional and metropolitan areas, as well as consumer spending categories, is behind NAB’s expansion of its Consumer Spending and Cashless Retail analyses.

Our real GDP growth forecasts remain relatively unchanged, with growth of around 0.6 per cent in Quarter 2 2017, or 1.68 per cent for the year to June. The much-discussed liquefied natural gas (LNG) exports, as well as building activity after weather-related disruption, are adding to GDP and will reach a peak in late 2017. After that, we still expect GDP growth to slow and return to 2 per cent during 2018, before increased non-mining investment and public spending strengthen it to nearer 3 per cent come 2019.

While there has been much talk of problems with natural resources, rural exports will also face more challenging conditions. June’s well-below-average rainfall was behind our wheat production forecast of 23.3 million tonnes, a decline of more than a third compared to last year. Conversely, the drought has caused an uptick in cattle slaughter. If it remains dry, the financial forecast could deteriorate further, with dairy production also coming under pressure.

Elsewhere, improved profit outcomes in the non-rural sectors of the economy have seen companies reporting the best business conditions for years, especially in the service sectors (as per NAB’s July Monthly Business Survey).

Conditions are back around pre-GFC levels and have carried business confidence with them: confidence is now around twice the long-run average. This rise in confidence is being led by the Construction, Manufacturing and Mining sectors, with the latter rebounding on stronger commodity prices and a firmer global outlook.

All these signals of GDP expansion are, however, in marked contrast to weak discretionary retail conditions and high levels of household debt. Consumers facing record low wages growth, high household debt and concerns about the labour market outcome have affected this sector, as has the 20 per cent increase to energy (gas) bills from July.

The new NAB Customer Spending Behaviours index unpacks this trend by analysing more than 4 million daily transactions (excluding mortgage and other credit facility payments) to provide detailed national and regional insights.

The index shows that national consumer spending growth slowed to 2 per cent year on year in Quarter 1 2017, down from 3.1 per cent the previous year. This translates into an average monthly fall in metropolitan spending from $2,171 in Quarter 4 2016 to $1,997 in Quarter 1 2017.

A notable exception was in the Electricity, Gas, Water and Waste category in some states. Spending in Sydney increased by 6.5 per cent, and in regional New South Wales by 6 per cent. In Queensland, Brisbane’s spend grew 4.9 per cent and the state’s regional spend grew 8.7 per cent. These compare sharply to Melbourne’s -3 per cent contraction and regional Victoria’s 0.1 per cent growth. Adelaide contracted by -6.8 per cent and regional South Australia by -6 per cent.

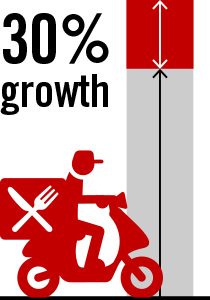

The category experiencing the strongest spending growth was Arts and Recreation Services, at 12 per cent. The only online retail sector reporting strong growth was takeaway food, which registered 30 per cent per annum growth thanks to delivery services such as Deliveroo, Foodora and UberEATS. It’s unclear how much more growth we can expect in this sector.

Another new index, the NAB Cashless Retail Sales Index, measures all cashless retail spend on NAB platforms – about 2 million daily transactions on debit and credit cards both online and in person, plus services such as PayPal and BPAY. It also includes domestic and international online spend.

This index shows that the value of cashless retail spending increased 5.6 per cent year on year in June, down from May’s 8.7 per cent year-on-year growth. This continues the downward growth trend that started in early 2015. It was most evident in household goods, clothing and footwear, and department store purchases. Once again, cafes, restaurants and takeaways provided the strongest growth. ‘Other’ retailing, including recreational goods, pharmaceuticals and cosmetics, also improved slightly.

Overall, we see strong near-term growth that will fade as LNG and construction activity peak in 2018, while growth in 2019 should improve to nearer 2.5 per cent as infrastructure spending and non-mining business investment increase. With inflation subdued and unemployment likely to remain around 5 per cent (or more), we don’t anticipate seeing rate rises from the RBA until 2019.

This article was first published in Business View magazine (Issue 24).

The NAB Consumer Stress Index has eased to a 2-year low and marks its 50th iteration.

Insight

Change is a constant in our global environment, but that's all the more reason to keep moving forward on your terms.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.