The latest NAB Regional & Agribusiness webinar provides insights on the Australian & Global Economies, and a regional and rural property update. Watch the webinar here.

A volatile night where earlier price action in Asia was largely reversed.

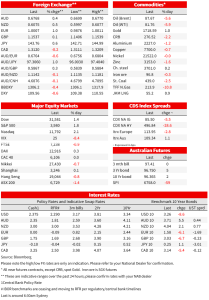

A volatile night where earlier price action in Asia was largely reversed. The spark for the reversal looks to have been the plunge in UK yields after BoE officials expected the government’s fiscal moves to reduce inflation in the short term, but uncertainty remains what path government policy will take. Chancellor Kwarteng also met with BoE Governor Bailey, affirming the government’s commitment to BoE independence, removing uncertainty generated on the campaign trail. Bailey also noted that the BoE may revise plans to start selling Gilt holdings next month if it judges the market will struggle to digest the huge issuance needs to fund the government’s proposed energy bill rescue scheme – some £200b over the next 18 months. UK 2yr yields plunged -20bps to 3.00%, as markets re-priced the expected peak in inflation. Longer term yields though were less moved with the UK 10yr Gilt -6.3bps to 3.03%. The plunge in UK yields was felt globally with the US 2yr yield -7.6bps to 3.43%.

Also adding to the move in yields were renewed growth concerns with China extending the lockdown in Chengdu; also reflected in oil prices with Brent -5.6% to $87.67. Helping insulate a little was ongoing hawkish Fed rhetoric and a WSJ article by Fed whisperer Timiraos which suggested a 75bp hike in Sep was the default option. Risk assets rallied on the fall in yields, exacerbated by positioning, with the S&P500 +1.8%. Equity markets also took some heart from some select quoting of a speech by the Fed’s Brainard, again chasing the elusive Fed pivot angle. Playing perhaps to a downshift in the pace of hikes was the Bank of Canada last night which hiked by 75bps. Although the post-meeting statement still pointed to further hikes, the prior reference to front loading hikes was removed and the BoC said that “as the effects of tighter monetary policy work through the economy, we will be assessing how much higher interest rates need to go to return inflation to target”. There was though little reaction in Canadian rates.

Data was very light, but in the US the Atlanta Fed’s GDP Now tracker downgraded Q3 growth to 1.4% annualised from a prior iteration of 2.6%. So back to the narrative of only a small rebound of the two quarters of negative growth seen in H1 2022. The Fed’s Beige Book, although not market moving, played to that view with the comment “The outlook for future economic growth remained generally weak, with contacts noting expectations for further softening of demand over the next six to twelve months”. Labour markets remained tight, but isome signs of acute inflation easing (“Price levels remained highly elevated, but nine Districts reported some degree of moderation in their rate of increase ”). As for hard data, the US Advanced Trade Balance was broadly in line at -70.bn against -70.2bn expected. In Asia yesterday, China’s trade balance played to the view of slowing momentum (exports 7.1% y/y against 13.0% expected). Meanwhile Chengdu’s lockdown has been extended for the downtown area; easing for suburban areas. China’s zero-COVID policy very much in force into the lead up to 16 October where Present Xi goes for his third five-year term.

In terms of US Fed development, Fed whisperer Nick Timiraos penned a piece that suggested the Fed’s default option for September was a 75bp hike: “The Federal Reserve appears to be on a path to raise interest rates by another 0.75 percentage point this month in the wake of Chairman Jerome Powell’s public pledge to reduce inflation even if it increases unemployment. Fed officials have done little to push back against market expectations of a third consecutive 0.75-point rate rise in recent public statements and interviews ahead of their Sept. 20-21 policy meeting”. (see WSJ: Fed on Path for Another 0.75-Point Interest-Rate Lift After Powell’s Inflation Pledge).

Fed speak was consistent with continued hawkishness. The Fed’s Bar noted in Q&A that “There may be further slowdown and even some pain in the economy. It’s far worse to let inflation continue to be too high”. The Fed’s Mester was similar, noting the Fed had more work to do to get inflation under control and re-iterated her view that the fed funds rate needed to increased to just “somewhat above” 4% by early next year, as well as pushing back against the pricing of cuts in 2023 (“I do not anticipate the Fed cutting the fed funds rate target next year”). The Fed’s Barkin earlier in an FT interview also made similar remarks, while also attempting to re-frame what a recession is: “ The word recession doesn’t have to mean a calamitous decline in activity…The word recession can mean a rebalancing to get the economy back to normal.” (see Barkin: Fed must ‘put inflation to bed’ by keeping rates high, says top official). Note Powell is speaking tonight.

Although Fed rhetoric overall was hawkish, markets seemed to read more into Brainard’s [not less hawkish] comments. Brainard noted that: “At some point in the tightening cycle, the risks will become more two-sided. The rapidity of the tightening cycle and its global nature, as well as the uncertainty around the pace at which the effects of tighter financial conditions are working their way through aggregate demand, create risks associated with overtightening”. Read in isolation that may have sounded like a hint of a Fed pivot signal. It wasn’t. Equities though loved it with the S&P500 extending gains on those headlines. Brainard also stated in the subsequent and concluding paragraph that “ We are in this for as long as it takes to get inflation down… and the policy rate will need to rise further… Monetary policy will need to be restrictive for some time to provide confidence that inflation is moving down to target”. (see Brainard: Bringing Inflation Down).

In FX, it was been very volatile, with Asia’s sizeable moves yesterday mostly reversed except for the Yen. To re-cap, unrelenting USD strength drove the NZD down to 0.5997 (its lowest in 2 years), USD/JPY lifted to just shy of 145 and to a fresh 24 year high, the AUD printed sub-0.67, GBP got as low as 1.1406 (lowest level since 1985!). All those moves have been mostly reversed with USD (DXY) now -0.6% and over the past 24 hours, the AUD is +0.4% to 0.6768, NZD +0.5% to 0.6075. GBP is now just above 1.15. USD/Yen though is still 0.6% higher over the past 24 hours to 143.76. The spark for the reversal appeared to be the earlier comments by BoE officials given until a week ago, people were calling UK inflation to hit 22%!

The latest NAB Regional & Agribusiness webinar provides insights on the Australian & Global Economies, and a regional and rural property update. Watch the webinar here.

The NAB Rural Commodities Index continued to climb in June – up by 2.2% month-on-month in Australian dollar (AUD) terms.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.