We expect growth in the global economy to remain subdued out to 2026.

Insight

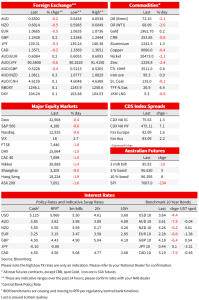

The AUD had fallen to a new post November 2022 following more disappointing China data

CH: Manufacturing PMI, May: 48.8 from 49.2 vs. 49.5 exp.

CH: Non-manufacturing PMI, May: 54.5 from 56.4 vs. 55.2 exp.

AU: CPI (y/y%), Apr: 6.8 from 6.3% vs. 6.4 exp.

GE: CPI EU harmonised (y/y%), May: 6.3 from 7.6% vs. 6.7 exp.

CA: GDP (annualised q/q%) 3.1% in Q1 vs -0.1% in Q4 and 2.5 exp.

US: Chicago PMI, May: 40.4 from 48.6 vs. 47.3 exp.

US: JOLTS job openings (m), Apr: 10.1 from upward revised 9.745mn (9.59) vs. 9.4 exp.

May is ending with US stock indices down just over 0.5% on the day and little changed on the month for the S&P but with the NASDAQ up nearly 6% (thank you, Nvidia). Bond yield are lower both in the US and Europe after two Fed official signalled support for a pause this month and German and French CPI data suggested a bigger than expected drop in pan-Eurozone inflation to be reported later today. AUD/USD meanwhile found no love from a post-CPI lift to June RBA rate hike expectations, instead suffering at the hands of downside misses on China PMIs and related fresh weakening in the Yuan, to an overnight low of 0.6458 (though back to ~0.65 now). The US House vote on the Fiscal Responsibility Act which will suspend the debt ceiling for two years, should come in the next few hours. Passage is assumed, though very short-dated T.Bill yields have backed up a little ahead of the vote.

Neither US data not incoming Fed speak have gone unnoticed in overnight markets. The JOLTS (job openings) report showed an unexpected jump to be back above 10 million in April (10.1mn with March revised up to 9.75mn from 9.59mn). Still 2 million below the peak of a year ago (12.03mn) while the Quit Rate (percentage of those in work quitting their job) fell to 2.4 from 2.5 and a high of 3.0 a year ago. There are still 1.8 job opening for every unemployed person. Other data shows a much larger than expected drop in the Chicago PMI, to 40.4 from 48.6 , which together with other regional PMIs, suggest that tonight’s manufacturing ISM is at risk of a slightly bigger drop than the official consensus for 47.0 from 47.1.

The Fed’s Beige Book reported a broadly stagnant economy, characterizing activity as “little changed” in April and early May. There was some deceleration noted in employment growth, and a rise in consumer loan delinquencies. Labor demand also appeared to cool, while the pace of inflation appeared to slow in many districts, with consumers showing a bit more price sensitivity. Home prices and rents rose slightly, while commercial real estate remained weak.

On the Fed, Fed Vice Chair Philip Jefferson said, “A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle”. Echoing this, Philadelphia Fed President Patrick Harker (also a FOMC voter this year) said “I think we can take a bit of a skip for a meeting and frankly, if we’re going to go into a period where we need to do more tightening, we can do that every other meeting.” In contrast Cleveland Fed President Mester earlier told the FT, “I don’t really see a compelling reason to pause — meaning wait until you get more evidence to decide what to do,” she said. “I would see more of a compelling case for bringing [rates] up . . . and then holding for a while until you get less uncertain about where the economy is going.” Note though Mester is not a 2023 FOMC voter. Following the Jefferson and Harker comments, US money markets scaled back their pricing for June quarter point Fund rate hike to about 40% from 60% earlier, though a hike by July remains close to 100% priced.

Canada reported Q1 GDP at 3.1% at a quarterly annualised rate, above the 2.5% consensus though the monthly March number was unchanged (-0.1% expected). Pricing for a quarter point BoC rate rise next week has actually paired back a bit (~27% from 30%) though this probably has more to do with the fall in Fed pricing than the local GDP data.

In Europe, weaker than expected CPI data from France and Germany (but not Italy) and following a prior day downside surprise from Spain, has seen ECB pricing scaled back a bit, with now slightly less than two quarter-point hikes price from at least two previously.

AUD/USD’s fall to a new post-November 2022 low of 0.6458 largely tracks the weakening Yuan (to above 7.10 to the USD Wednesday) and which in turn followed May China official PMI data that disappointed expectations and so playing further to the view that the post-zero covid economic recovery is losing momentum (and manufacturing going backwards). Manufacturing fell to 48.8 from 49.2 (and a post-covid high of 52.6 in February) with non-manufacturing 54.5 from 56.4 and it’s high of 58.2 in March. While the composite PMI at 52.9, from 54.4, is ostensibly still consistent with very decent Q2 GDP growth (circa 1.5-2.0%q/q) evidence of policy levers being pulled to incentivise stronger consumer spending and/or infrastructure spending are increasingly required to reduce the market’s current China growth worry warts.

The fall in the Aussie came despite money markets lifting their implied probability of a quarter point rate rise next week to 36% from 21% (and now full pricing a rise by August). This followed the April Monthly CPI Indicator which rose 6.8% y/y from 6.3%y/y in March (NAB 6.6%, consensus 6.4%). In original terms it rose 0.8% m/m. Two key points are worth noting outside of base effects from automotive fuel which drove the y/y rate higher. The first is signs goods inflation does not look to have slowed further, and indeed furniture unwound its progress in Q1, up 4.9% in April. The RBA forecasts goods disinflation to continue over 2023, and today’s data suggests it may not be a smooth process. The second is rent inflation has picked up further (0.8% m/m) and rents will be a large contributor to CPI for some time given pressures in the rental market.

Interpreting the Monthly CPI is difficult given it is only a partial indicator of month-to-month inflation dynamics. In the first month of the quarter, including yesterday’s April release, it has very incomplete coverage of services inflation. Governor Lowe, including in front of the Senate Economics committee yesterday, has rightly pointed to services as a key source of risk for persistence in too-high inflation and there is very little new news on that available today and which is, as Dr Lowe was at pains to point out, largely driven by Unit Labour Costs and in the absence of a return to pre-covid productivity trends (circa +1.0%) makes wages growth of 3.5% or more inconsistent with meeting the inflation target. What news there was in CPI overall suggested little further progress on disinflation, including across goods.

Australia Q1 construction figures were better than expected at 1.8% against 0.5% consensus. Strength was driven by engineering (+5.3%) while residential building remained soft (-2.0% m/m). Only some components of today’s release feeds into GDP and on our calculations we think it will make a flat contribution to GDP growth in Q1.

In G10 FX, the AUD actually ended Wednesday mid-pack, with loses exceeded by the NZD, EUR and CHF (all down 0.4-0.5% vs 0.2% for AUD) while the SEK, CAD and JPY end New York trade 0.2-0.3% firmer (leaving the DXY USD index barely changed, +0.06%). The outlier is NOK, up 0.9%, and NOK, a curio insofar as oil prices are down another 2.0-2.5%, Brent to $72.20 and WTI to $67.66, seemingly on intensifying demand concerns led by China. This is in front of the (June 4) OPEC+ meeting, to which we see that journalists from Bloomberg, Reuters and the Wall Street Journal have been excluded.

Bonds are ending the New York day with 2-year Treasuries down 4.7bps thanks to the Fed June pause speak and 10s down 4.4bps. Earlier benchmark Eurozone bond yields finished some 6ps lower (France, Germany) and UK gilts 10bps down.

Finally looking across global equity markets, not a single one is in the green with all major European and APAC indices down at least 1% on the last trading day of May (Eurostoxx50 -1.7%).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect growth in the global economy to remain subdued out to 2026.

Insight

Financial institution issuance has recorded another high-volume year in the Australian dollar bond market, with some key questions still to explore ahead of a fast start in 2025.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.