We hear from NAB’s new Chief Economist, as she unpacks the latest economic data with Deb Knight, Host of Money News – 2GB. Watch now.

Video

August has been a terrible month for balance fund investors with no diversification gains from holding a portfolio of equities and bonds.

NZ: Dwelling consents (m/m%), Jul: 5.0 vs. -2.2 prev.

JN: Industrial production (m/m%), Jul: 1.0 vs. -0.5 exp.

NZ: ANZ activity outlook (net%), Aug: -4.0 vs. -8.7 prev.

CH: Manufacturing PMI, Aug: 49.4 vs. 49.2 exp.

CH: Non-manufacturing PMI, Aug: 52.6 vs. 52.3 exp.

GE: Unemployment rate (%), Aug: 5.5 vs. 5.5 exp.

EC: CPI (y/y%), Aug: 9.1 vs. 9.0 exp.

EC: CPI core (y/y%), Aug: 4.3 vs. 4.1 exp.

CA: GDP (annl’sd q/q%), Q2: 3.3 vs. 4.4 exp.

US: ADP employment change (k), Aug: 132 vs. 300 exp.

US: MNI Chicago PMI, Aug: 52.2 vs. 52.1 exp

Month end yields no surprises, but rather an extension of the major themes seen during August with further increases in core global bond yields and weaker equities. FX moves have been more subdued, risk aversion in the air has weighed on the AUD and NZD while another increase in ECB rate hike expectation, after EZ CPI beats estimates, supports the euro, GBP remains in struggle street.

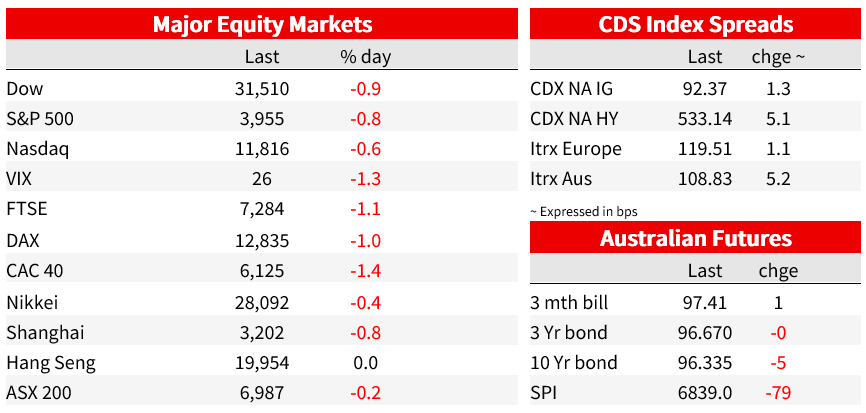

August has been a terrible month for balance fund investors with no diversification gains from holding a portfolio of equities and bonds. European equities have led the declines overnight and for the month, the Eurostoxx 50 fell 1.25% on the last day August recording a 5.15% decline for the whole month. The DAX was not too far behind, falling 0.97% overnight and 4.81% in August. The Stoxx 600 fell over 4% in the month with the energy sector the only positive performer notwithstanding the fact that oil prices decline just over 12% in August. Not surprisingly, given the deteriorating economic backdrop exacerbated by Russia weaponization of energy supply, retail and real estate were the month’s underperforming sectors.

The S&P 500 closed 0.78% lower overnight, falling 4.24% in August while the NASDAQ fell 0.56% overnight and 4.64% over the month. The S&P 500 sector performance reveals a similar pattern to their European counterparts, energy was the months outperformer up 2.18% while utilities was the only other sector that managed to record (modest) gains in the month, up 0.07%. Real Estate (-5.71%) Healthcare ( -5.88%) and IT ( -6.26%) ended at the bottom of the performance board.

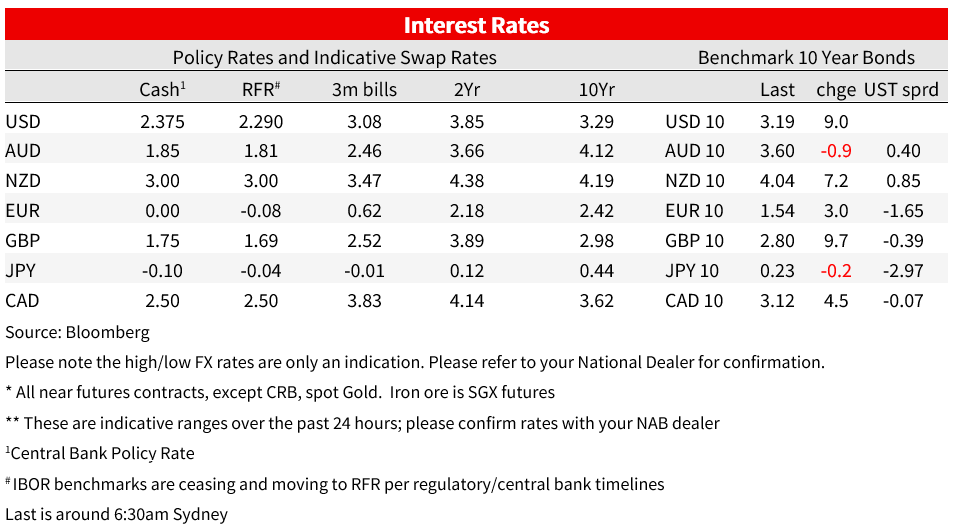

The Euro Area CPI for August was the major data release overnight beating estimate for the headline as well as the core reading. The headline reading printed at 9.1%, one tenth higher than expected by consensus, a new record high while the core reading came at 4.3%, also one tenth above estimates. Reacting to the data release, Bundesbank Chief Nagel said “there’s an urgent need for the Governing Council to act decisively at its next meeting to combat inflation” and argued for a “strong rise” in rates in September and further interest rate steps over following months. This week ECB Vasle said that “We haven’t seen the highest numbers for inflation — not in Slovenia, not in the euro zone,” while Bloomberg also notes that six GC members have publicly said that a rate hike of more than 50bps should be discussed. ECB rate expectations have continued to edge higher, pricing for the September meeting climbed another 2bps overnight to 67bps, up from 44bps a fortnight ago. The ECB deposit rate is now seen at 1.61% by December, up from 91bps at the start of August.

Against this backdrop the recent rise in European bond yield extended overnight, 10 Bund yields gained 3bps to 1.54%, Italian BTPS climbed 6bps to 3.89% while 10y Gilts jumped 10bps to 2.80%. The monthly chart reveals an eye watering rise in EU yields with 10y Gilts leading the charge, up 94bps, BTPS up 87bps and Bunds 78bps.

A similar theme can be seen in he US Treasury markets, albeit in smaller magnitudes. In the last couple of hours of trading 10y UST have surge 8bps to 3.19% while the 2y rate climbed a smaller 4bps to 3.485%. The 2y10y curve is steeper on the day ( -30bsp), but still 6bps flatter on the on month. Gains in UST yield during Augusts were led by the 5y part of the curve , up 67bps while 2y yields gained 59bps and 10y climbed 53bps.

The revamped US ADP employment report was released overnight showing Private sector employment increased by 132k jobs in August and annual pay was up 7.6%. The gains in jobs slowed significantly relative to the close to 270k jobs recorded in the previous month with ADP chief economist noting “We could be at an inflection point, from super-charged job gains to something more normal.”. It is hard to draw any major ADP implications for the US payrolls data due out on Friday, like the ADP report, consensus also sees a big decline in job gains from 528k to 298k while average earning are seen at 0.4% mom from 0.5% previously. The ADP and expectations for payrolls depict a US labour market that remains tight, reinforcing the need for the Fed to remain on its hawkish path.

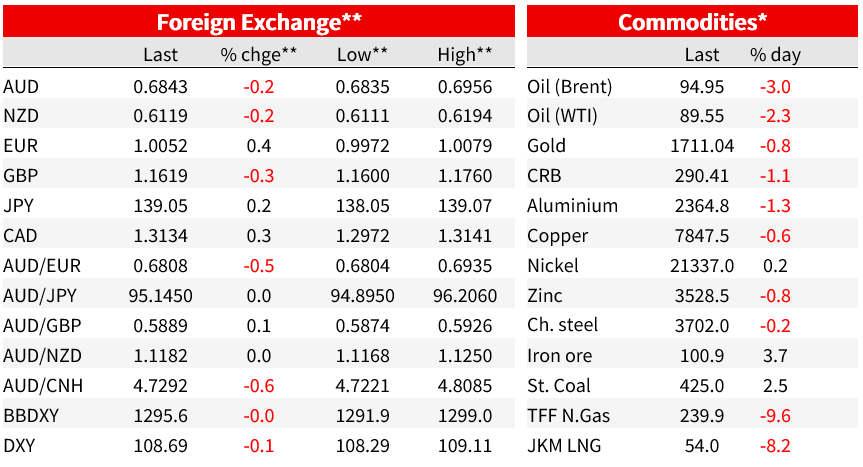

Moving onto FX, the euro has edged a little bit higher again, now trading at 1.0054 and up 0.37% over the past 24 hours. The move up in ECB rate hike expectations has been a key supporting factor while another decline in gas prices has also helped. The Dutch TFF benchmark fell 9.8% overnight, closing the day at 239.91, still 240% higher relative to levels recorded at the start of the year. A three-day “maintenance” shutdown has begun for the Nordstream pipeline that runs into Germany. Gazprom said it would suspend gas sales to French utility Engie over a dispute over payments, adding to the growing list of gas buyers that are now banned. However, market sentiment has improved as storage facilities fill and the EU looks to intervene in the energy market. Oil prices are closing the month on a soft note, with Brent crude down around 3% to USD96.50 per barrel.

The AUD (@ 0.6842) and NZD (@ 0.6115) are a tad lower (~0.2%) relative to levels this time yesterday with the risk aversions seen in equity market not helping their cause. In August the AUD fell 2% while NZD slipped 2.6%. Meanwhile GBP has remained in struggle street, edging lower again overnight to 1.1622 and down over 4.5% during the month. JPY is the other big montlty underperformer within the majors, down 4.58% in August and still looking vulnerable to further rise in UST yields. USD/JPY now trades at 139,02 with not a lot resistance to test a move back above 140.

We hear from NAB’s new Chief Economist, as she unpacks the latest economic data with Deb Knight, Host of Money News – 2GB. Watch now.

Video

An exclusive Commercial Real Estate webinar on the Retail Property, Insights and Outlook. Watch now.

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.