Coming in for landing in a heavy cross wind

Insight

Eurozone bonds yields and stocks falling on the latest jump in energy prices – both oil and gas – following confirmation the NordSteeam1 gas pipeline will remain shut while Russian sanctions are in place.

The US has been out for Labor Day with both stocks and bonds, but which hasn’t prevented Eurozone bonds yields and stocks falling on the latest jump in energy prices – both oil and gas – following confirmation the NordSteeam1 gas pipeline will remain shut while Russian sanctions are in place. Eurozone Services and hence Composite PMIs have been revised lower, so too in the UK, further highlighting the contrasting economic fortunes of the United States versus Europe (and much of the rest of the world). A message not lost on currency markets, where the DXY USD index has risen to a new 20+ year high. The RBA is widely expected to lift the Cash Rate by 50bps today. US ISM Services is the main economic draw in the coming 24 hours.

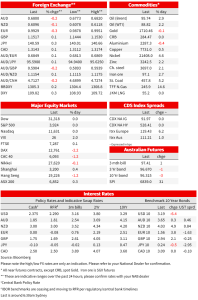

Energy markets remain front and centre , with European gas prices on the Netherlands exchange jumping 30% at Monday’s open following confirmation that the Nordsteam1 gas pipeline had not reopened after the 3-day shutdown that started last Wednesday, a Russian spokesman making it abundantly clear that it would remain shut while sanctions on Russia remain in place. Prices have been pared to show ‘just’ a 17% up on the day at EUR24.50 per megawatt hour. The best that can be said is that the price is still well off the EUR311, 25 August, high.

Adding to the energy market misery (if you are a user not a supplier that is) OPEC+ unexpectedly agree to reverse the 100,00 barrels per day output increase that had been agreed in August for September , somewhat against expectations that the meeting might convey just such a threat without acting on it as early as October. Expected or not, the oil market has been buying the rumour of just such an output reduction and evidently sold the fact with Brent crude $2 lower post meeting, albeit still up a hefty $2.72 versus Friday night’s close (WTI +$1.95)

Adding to oil market supply-side woes, the EU’s Josef Burrell has been out saying that Iran nuclear talks are diverging not converging. “I am sorry to say that I am less confident today than 28 hours before on the convergence of the negotiation process and on the process of closing a deal right now,” Borrell told a press conference. Chances of a deal this side of the US November mid-terms look increasingly slim, a view NAB’s commodity experts have held for a while.

In economic news, there have been some quite chunky downward revisions in the Final vintages of the European Services PMIs, in pan European terms from 50.2 from 49.8, dragging the Composite reading down to 48.9 from 49.2 (led by Germany, whose Services reading is now 47.7 versus a 48.2 Preliminary read). In the UK, a preliminary 52.2 Composite read- that stood out like a sore thumb in the preliminary release- has been revised away to just 50.9, intuitively far more realistic.

And in the UK, Liz Truss was formally anointed as the new Leader of the Conservative Party and hence PM overnight, by a smaller than expected majority (at 57% of the vote, this is the lowest of any Tory leader in recent history). Truss gave only a short acceptance speech with no details, saying “We need to show we will deliver…” Deliver a bold plan to cut taxes and grow the economy…” “Dealing with the issues we have on energy supply…” “And I will deliver on the NHS…”. “We will deliver for our country…” using all the fantastic talents of the party… “We will deliver, we will deliver, and we will deliver.” To which my London colleague Gavin Friend quips, “And now reality bites”.

Whether UK fiscal policy will flip from being contractionary to expansionary, or merely less contractionary, the risk that the Bank of England will see fit to push on with several more Bank Rate rise of at last 50bps in short order, is arguably heightened, pending the detail of what fiscal policy will soon look like. Overnight, we’ve heard from BoE policy maker Catherine Mann (admittedly a hawk) calling for “forceful” action to contain inflation . She says an upward drift in expectations about where consumer prices are headed has become “apparent” and that officials “cannot be complacent.” “Acting more forcefully now, to ensure that the drift does not become the norm, is designed to avoid depending on a deeper and longer contraction to return inflation to target,” Mann says. Asked whether her remarks open the door to a 75-basis point increase from the BOE, the scale delivered by the US Federal Reserve, Mann replied, “It’s an important question. What we need to be doing is to make sure the medium-term inflation expectations don’t drift.”

Ahead of Thursday’s ECB meeting and following the latest jump in energy prices into Europe, benchmark Eurozone bond yield are higher, in Germany by 4bps at 10 years and Italy by more than 10bps (recall some ECB Council members are reportedly agitating for an early start to QT, which will disproportionally impact the euro-peripheral bond market if so). The gas price jump has also taken another bite out of the Eurostoxx 50 (-1.5%) with the German DAX the worse of any individual Eurozone markets (-2.2%). The FTSE100 in contrast finished +0.1%, where the latest fall in GBP is to note given the heavy dependence on overseas earnings by UK PLC.

FX sees the USD continuing to flex its muscles and showing they are in better shape than anyone else’s. The DXY index has made a new 20+ year high, spending time above 110.0 and currently up about 0.25% on the day at 109.8, led by similar sized quarter percent losses for both the EUR and JPY. GBP/USD’s low of $1.1444 is, depending on where you look, just about matching the early-stage pandemic low, beyond which we need to go back to 1985 for lower levels.

AUD/USD has just about held above last Thursday’s 0.6771 low, currently hovering around the 0.6800 level. Relevant to it, and the NZD’s fortunes, remain the Chinese Yuan. Overnight, the PBoC announcing a two-percentage point cut to banks’ foreign currency required reserve ratio , from 8% to 6%, a move designed to free up more foreign currency that could potentially be sold for Yuan. USD/CNH fell back from a high of 6.9550 on the news, but at around 6.94 is still two big figures above last Friday’s 6.92 weekly close.

NAB Markets Research Disclaimer

Coming in for landing in a heavy cross wind

Insight

NAB Portal Pay’s Tenant Portal helped One Agency Lindy Harris in Singleton increase efficiencies, boost compliance, and grow faster in a high-demand market.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.