NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The Euro and Italian bonds took a hit with German judges challenging the ECB on its QE activity.

https://soundcloud.com/user-291029717/germanys-judges-declare-war-on-the-ecb?in=user-291029717/sets/the-morning-call

“Back at base bugs in the software; Flash the message “something’s out there!”; Floating in the summer sky; Ninety-nine red balloons go by”, Nena 1983

Risk sentiment continues to be buoyed on news of more countries/states rolling back containment measures (latest being California and Hong Kong), followed by reports of more companies re-opening operations (Starbucks said 85% of its stores will re-open by end of the week). That’s giving hope that rollback will allow economic activity to resume and that we may be passed the trough in economic activity.

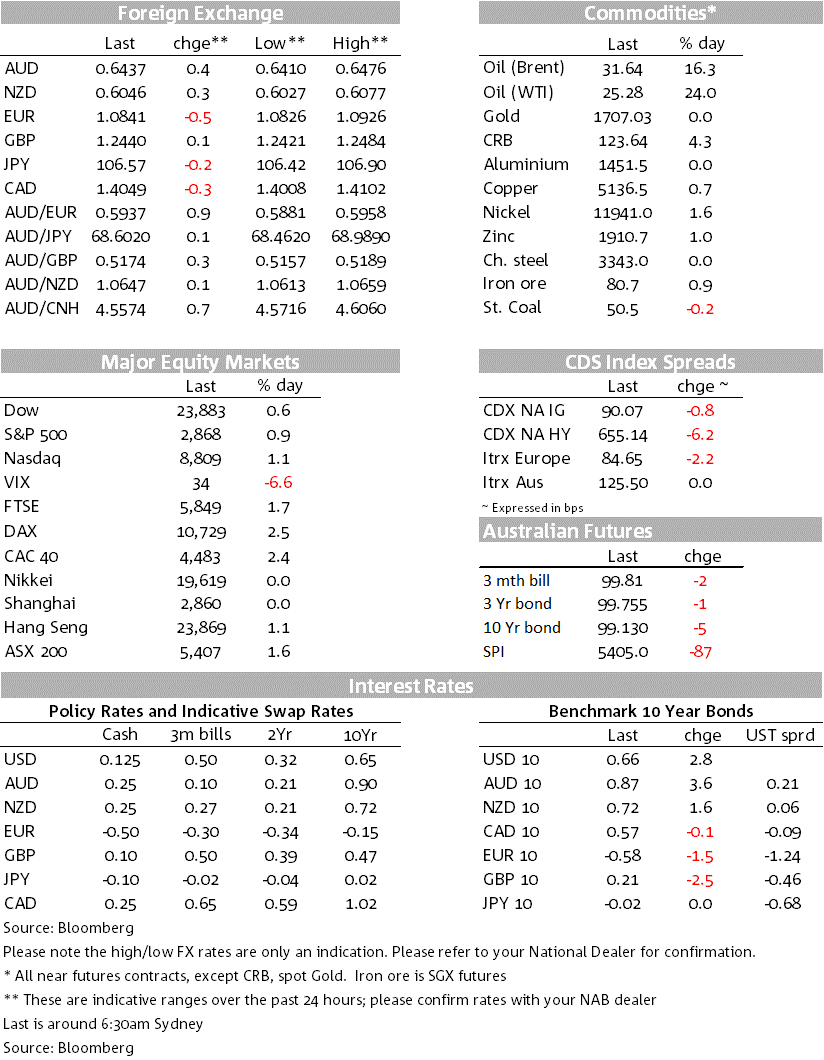

Equities rose with the S&P500 up +0.9% along with G10 FX global growth proxies of AUD +0.3% and NZD +0.5%. Despite the positive sentiment the USD also rose (DXY +0.3%) as the EUR fell -0.5% following the German Constitutional Court’s ruling that the ECB must undertake a “proportionality assessment” of its government bond buying program within 3 months and threatened to block the Bundesbank’s participation if it did not.

At this stage it is likely the ECB will be able to justify its program, but the key outcome is the ECB’s “whatever it takes” now comes with limits. It’s no surprise than to see only a limited impact of the court’s ruling on markets, the exception being Italian 10yr yields up +10bps. Other global yields were little moved with US 10yr yields +2.8bps to 0.66%. Commodities also lifted with WTI June +22% and up for the fifth consecutive day; Brent +15%.

The court ruled 7 v 1 that the German authorities acted unconstitutionally by not challenging the ECB’s bond buying program (they had “a duty to take active steps against” QE “in its current form”) and the ECB needs to carry out a “proportionality assessment” of its public sector purchase program to ensure their “economic and fiscal policy effects” did not outweigh its policy objectives, and threatened to block new bond-buying unless the ECB did so within three months. The Bundesbank’s Weidmann noted the decision emphasises the important design features of the public sector purchase program that, overall, ensure there is a sufficient distance from monetary financing. Given the Bundesbank’s support, it is likely the ECB will be able to justify its bond buying program to German authorities.

The ruling though does set the scene for a legal challenge against the ECB’s new €750b pandemic emergency purchase programme, which has looser limits than the previous public sector asset purchase program. It overall also suggests governments need to step in and take pressure off the ECB. There was only a limited impact on markets, but the ruling does provide a limit to the ECB’s “whatever it takes” pledge. EUR is now down 0.5% for the day at 1.0841. Italy’s 10 year rate rose by 10bps to 1.86% against a 2bps fall in the Germany 10-year rate to minus 0.58%.

The Non-manufacturing ISM was a little better than expected, but was much weaker below the surface. The Headline was 41.8 v 38e and 52.5p; the headline though was flattered by supplier deliveries which rose to 78.3 with supply chains tightening as firms closed. The more important Business Activity Index was just 26, New Orders 32.9 and Employment 30 – all deep into the contraction territory and more consistent with the Markit Services PMI of 26.7. Also out was the March Trade Balance, again largely expected (-44.4bn v -44.2e).

Yesterday’s RBA meeting also came and went without much fanfare with the cash rate and 3yr yield target held at 0.25%. The AUD was little moved on the news, having already lifted on positive risk sentiment. The only change was the RBA broadening its repo-acceptable collateral to include investment grade corporate bonds to assist with the smooth functioning of markets. The inclusion of investment grade corporate bonds potentially provides a liquidity boost for what had mostly been largely illiquid assets and provides a liquidity outlet for funds who may also be facing redemptions; some material tightening in corporate spreads is thus likely. The RBA also provided some information on its central forecast scenario which will be published on Friday.

The RBA sees unemployment peaking at around 10% and will still be above 7% by the end of next year.

Other data publishes also painted a sobering picture of the economy with weekly payrolls data showing that 7.5% of Australian jobs have been lost in the five weeks since the lockdown began, equivalent to about 1 million people losing employment. The PM also noted that more than 1 million JobSeeker claims had been processed and 4.7 million were receiving JobKeeper – that overall suggests 50% of the labour force is now being assisted by the government.

Most focus this morning will be on Australian Retail Sales and NZ Unemployment. Unlike in prior releases, Australian Retail Sale is unlikely to be as market moving given the ABS now publish a flash measure – the flash rose 8.0% m/m in March and that is where the consensus is. Also out today is the quarterly volumes measure which feeds into GDP.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.