We expect growth in the global economy to remain subdued out to 2026.

Insight

It has been a quiet start to the week in Europe and the US with the latter out celebrating Labor Day. US equity futures closed little changed while US Treasury futures are pointing to some small upside pressure on yields.

NZ: Terms of trade, q/q%: Q2: 0.4 vs. -1.5 prev.

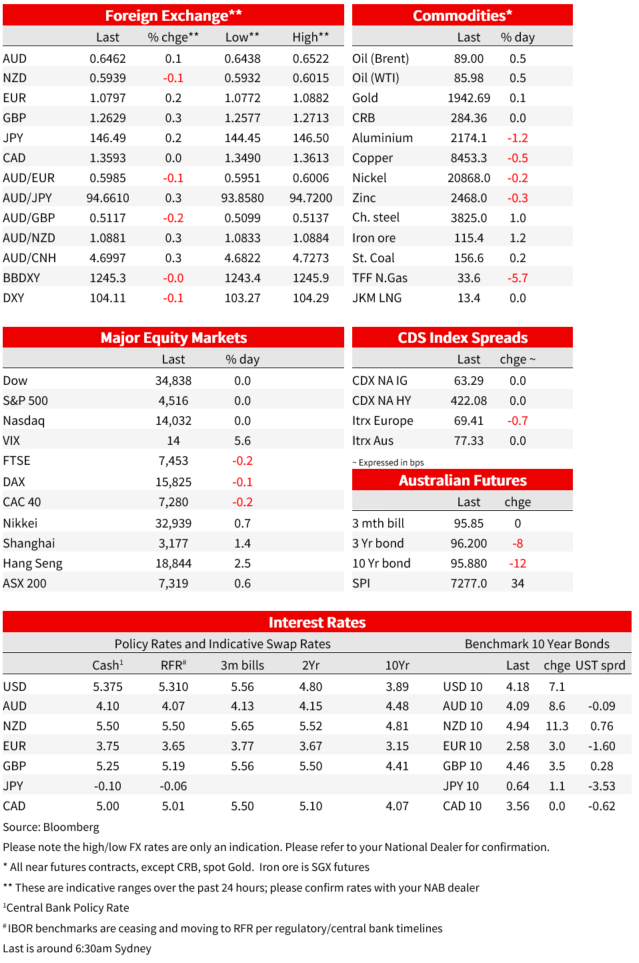

It has been a quiet start to the week in Europe and the US with the latter out celebrating Labor Day. US equity futures closed little changed while US Treasury futures pointing to some small upside pressure on yields. After opening higher, following positive vibes coming from Chinese equities, European equity indices closed little changed while European bonds edge a little bit higher. European FX also edged a tad higher while the AUD is essentially unchanged at 0.6461.

Chinese equities were the big movers during our trading time yesterday with the CSI 300 index closing 1.5% higher while the Hang Seng index rose 2.5%. Notably too, property developers indices in both markets jumped close to 8%. Late last week policy makers in Beijing announced some relaxation of mortgage rules, lowering the required down payments and increasing access to lower mortgage rates. Sentiment was boosted following weekend reports of a strong pick up in property sales activity in Beijing and Shanghai. One report noted in Shanghai the same number of transactions in one day as for the entire month of August. Existing home sales on Saturday in Beijing were double the previous Saturday, while there were 1800 units of new homes sold that day, more than half the 3100 units sold throughout August.

The positive Asian vibes boosted European equity indices at the open, but the move proved short lived with early gains eroding over the reminder of the day. Light trading conditions were a feature given the US holiday absence. Europe’s Stoxx 600 gauge closed little changed after rising as much as 0.8% earlier. On a holiday shortened session, US equity futures closed little changed with the S&P 500 min down 0.06% while the NASDAQ 100 mini was 0.04%.

European yields ticked higher with Bund yields climbing for a second day in a row. The 10y rate gained 3bps to 2.58% while 10y Gilts gained 3.5bps to 4.463%. Meanwhile with the UST market closed, Treasury futures point to some small upside pressure on yields, with the implied 10-year rate up about 2bps.

Speaking in London, ECB President Lagarde didn’t give much away in terms of policy guidance ahead of the Bank’s meeting next week. The President noted that “We have increased our policy rates by a cumulative total of 425 basis points in the space of 12 months — a record pace in record time. And we will achieve a timely return of inflation to our 2% medium-term target.”, adding that “Actions speak louder than words,”. Money markets are placing around one-in-four odds on the ECB raising rates a quarter-point to 4% next week. That compares to as much as a 60% chance before economic data showed core inflation in the euro area slowed.

Unsurprisingly currency moves have also been subdued. European pairs have edged a little bit higher with GBP at the top of the leader board, up 0.3% to 1.2633 while the euro is +0.15% to 1.0796. The AUD (+0.06% to 0.6461) and NZD (-0.08% to 0.594) are little changed, both antipodean pairs traded in narrow ranges overnight (~30pips) and start the new day around the middle of the overnight range. Of note, CNY was unable to enjoy any lift from the positive vibes evident in the Chinese equity market. Indeed, CNY closed 0.11% weaker at 7.27 . For now, supportive PBoC measures (strong fixes and lower FX deposit ratio) are seemingly helping slowdown but not necessarily reverse the currency weakness.

Oil and iron prices also ticked a little bit higher over the past 24 hours (+0.5%). Last week il prices gained on the back of news that Russia will extend export curbs. Saudi Arabia —the other big OPEC+ influencer – is widely expected to follow Moscow by extending its voluntary curbs into October.

Finally on LNG, Chevron has begun mediation discussions with workers at facilities in Western Australia . Bloomberg notes the two facilities operated by Chevron – Gorgon and Wheatstone – made up roughly 7% of global LNG supply last year. Employees at the two plants last week voted down the company’s pay package proposal. The unions will begin partial strikes from Sept. 7 and will ramp up to full days from Sept. 14, according to people with knowledge of the matter

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect growth in the global economy to remain subdued out to 2026.

Insight

Financial institution issuance has recorded another high-volume year in the Australian dollar bond market, with some key questions still to explore ahead of a fast start in 2025.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.