Protecting your business online is simpler than you think. NAB Executive Business Direct and Small Business, Krissie Jones, shares practical advice on how you can get started.

Newsletter

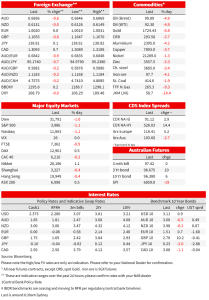

Goldman’s noted inflation could hit 22.4% y/y in the UK in early 2023 if gas prices don’t moderate and if there is little in the way of cost of living relief.

Turnaround Tuesday it wasn’t with equites falling sharply for a third consecutive day following US Fed Chair Powell’s Jackson Hole speech. Overnight it was ‘good news is bad news’ with the strong JOLTS data (11.239m vs. 10.375m expected) showing no signs of cooling in the labour market with the inference the Fed may need to be more aggressive to bring inflation under control. That notion was supported by hawkish Fed rhetoric with Williams stating “we need to have somewhat restrictive policy to slow demand” and that the Fed is “still quite a ways from that. ” Meanwhile across the pond Goldman’s warned UK inflation could hit 22.4% y/y in early 2023 if gas prices maintained at current levels, while for the ECB speakers such as Knot were leaning to a 75bp increase at the next meeting. These events saw the initial positive tone in APAC and early Europe reverse, while geopolitical risk also flared with Taiwan firing warning shots at a Chinese drone spotted near an offshore island.

Yields were mixed with the curve flattening slightly (2/10s down 2bps to -34.3bps). The 2yr yield rose around 2bps to 3.44% and the 10yr yield was little changed at 3.10%. There was some whipsaw action on news headlines that Taiwan fired warning shots at a Chinese drone that was spotted near an offshore island. Geopolitical angst didn’t last long and risk havens such as gold are lower at -0.8%, highlighting the strong JOLTS data and Fed rhetoric was the overwhelming narrative overnight. As for Fed pricing, markets still price around a 70% chance of a 75bp hike in September, while the peak in the Fed Funds rate has nudged higher to 3.88% in March 2023 (from 3.84% yesterday and 3.79% pre-Powell on Friday) , while there is 34bps worth of cuts still priced in 2023. Yields across the pond were similar, apart from the UK (10yr Gilt yields +10.2bps) where markets were playing catchup given the Bank Holiday on Monday.

Speaking of the UK, Goldman’s noted inflation could hit 22.4% y/y in early 2023 if gas prices don’t moderate and if there is little in the way of cost of living relief. That estimate is higher than Citi’s 18.6% which grabbed headlines last week, and is substantially higher than the BoE’s forecast peak of 13%. The extent to which the UK government provides cost of living relief will start to emerge from next week when the Tory leadership race wraps up on 5 September and a new PM is declared. Elsewhere in Europe, yields had initially moved lower on North Rhine Westphalia CPI coming in at 0.3% m/m (despite German CPI later being on consensus at 8.8% y/y), but reversed out on hawkish ECB messaging. Governing Council members Muller and Vasle both said a 75bp hike should be considered next week, earlier GC Member Knot said “some front-loading should not be excluded” and that he was leaning towards a 75bp hike. European gas prices fell again following up yesterday’s near-20% fall with another 7% drop, taking the Dutch TTF benchmark down to EUR253/Mwh. Gazprom will shut down the Nordstream pipeline to Germany for three days from today, but the market has become less nervous amid expected regulatory intervention to cap gas prices for power generation.

In terms of how that played out in equities, the S&P500 closed in the red at -1.1%, reversing the indicative 1% gains seen in futures during APAC. Since Fed Chair Powell’s words on Friday the S&P500 is -5.1% and at 3,986 is now below its 50 day moving average for the first time since 26 July. The VIX at 26.21 is also above its 50day moving average. How are Fed officials interpreting the move in equities? The Fed Kashkari in a podcast on Monday noted that he “was actually happy to see how Chair Powell’s Jackson hole speech was received. People now understand the seriousness of our commitment to getting inflation back down to 2%” and that he wasn’t excited by the stock market rally after the July FOMC meeting. Financial conditions are a key transmission mechanism for monetary policy and equities are part of that. Overall it also suggests the Fed put is a lot lower given where inflation is, something we wrote about in our NAB Markets Weekly (see NAB: What did we learn from Jackson Hole?).

In FX, the fall in gas prices and hawkish ECB-speak have helped support the euro, even against the backdrop of solid support for the USD. EUR (+0.0%) has managed to hang onto being above parity at 1.0020 even as the USD made broad-based gains with BBDXY +0.2%. Risk proxies such as the AUD (-0.8%), NZD (-0.5%) and USD/CAD (+0.7%) underperformed given the backdrop of lower commodity prices. GBP (-0.6%) meanwhile continues to trend lower against the backdrop of economic recession risks and headlines of insanely high inflation (see Goldman’s warning of 22.4% inflation above). Yesterday, the PBoC set the yuan fix at its strongest level compared to Bloomberg survey estimates in three years, some 249pips stronger on USD/CNY than the average estimate. This extended the run to five trading days for which the PBOC has set the yuan stronger than expected, a clear signal that it is trying to moderate the depreciating forces currently being exerted by the market.

The stronger fixings haven’t prevented USD/CNY rising to as high as 6.92, putting the yuan at its weakest level in two years. It is now looking inevitable that the psychological 7 level will be tested in the not-too-distant future. Weakness in the economy was highlighted overnight with one of China’s largest developers said the country’s property market has tumbled into a severe depression: “All these exert mounting pressure on all participants in the property market, which has slid rapidly into severe depression” (see WSJ: China’s Property Market Has Slid Into Severe Depression, Real-Estate Giant Says).

As for the data, US JOLTS data were much stronger than expected at 11.239m vs. the consensus of 10.375m, with upward revisions to boot. The data suggests there are no signs yet of a cooling in the labour market with the inference the Fed needs to be more aggressive. Note the number of people unemployed in the US 5.67m, suggesting even if layoffs rise, there is ample opportunity to get re-employment elsewhere. US Conference Board Consumer Confidence was also better than expected at 103.2 against a consensus of 98.0. The fall in gas prices has been a likely driver. Fed speak meanwhile played to the hawkish tone set by Powell. The Fed’s Williams noted “I do think with demand far exceeding supply, we do need to get real interest rates … above zero ” and that rates will have to be held higher for longer. The Fed’s Barkin noted more fully the unavoidable risk of recession in getting inflation under control, while Bostic said “inflation remains too high, and our policy stance will need to move into restrictive territory if inflation is to come down expeditiously.”

NAB Markets Research Disclaimer

Protecting your business online is simpler than you think. NAB Executive Business Direct and Small Business, Krissie Jones, shares practical advice on how you can get started.

Newsletter

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.