NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

A goldilocks payrolls report failed to support risk assets on Friday, with equities and the USD quickly reversing on news that Russia was not restarting gas flows through the Nord Stream pipeline

• Goldilocks payrolls overshadowed by the Nord Stream closure

• Equities closed in the red on Friday and the USD was little changed

• US yields first lower on both payrolls and on Nord Stream headlines

• China’s lockdown grows, Shenzhen joins Chengdu in lockdown

• Coming up: AU Inventories, Caixin Services PMI, US Labor Day

• This week: RBA & Lowe, AU Q2 GDP, ECB, BoC, Fed’s Powell

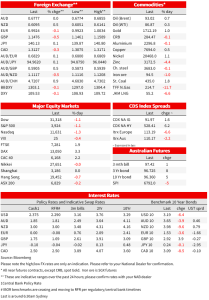

A goldilocks payrolls report failed to support risk assets on Friday, with equities and the USD quickly reversing on news that Russia was not restarting gas flows through the Nord Stream pipeline (no date for resumption was given). The S&P500 which was up by 1.3% post payrolls, fell sharply into the red to close down -1.1%. A similar was story was seen for the USD which had fallen -0.6% on the DXY post payrolls, rallying back to finish broadly unchanged (DXY -0.1%). Yields which fell sharply post payrolls, held onto to the sharp falls on the Nord Stream headlines with the US 2yr yield -11.9bps to 3.39%. The 2/10s curve steepened to -21bps with the 10yr yield -6.4bps to 3.19%. Highlighting the geopolitical angst, gold rose 1.0% to 1,712 despite the USD being little changed on the day. Note European cash markets were closed by the time the Nord Stream headlines hit – EuroStoxx futures point to -2.5% when trading resumes tonight. Except gas and wholesale electricity prices to also spike. Aside from European gas, the other focus is on expected rate hikes by the RBA, ECB and BoC.

First the to goldilocks payrolls report with payrolls broadly in line, but unemployment and wages coming in softer than expected . Headline payrolls were 315k against the 298k consensus, while the prior two months were revised down by a combined 107k. Unemployment rose two-tenths to 3.7% from 3.5% (3.5% expected) alongside a rise in the participation rate to 62.4% from 62.1%. Average hourly earnings also grew at a softer rate with average hourly earnings 0.3% m/m against 0.4% expected and down from 0.5%. On a 12-month basis, wage growth was a still-hot 5.2%, but that too was a touch below estimates. The increase in the part rate and a softening in average hourly earnings may be a tentative sign that intense labour market tightness is starting to ease slightly, and eases some of the fears stemming from other indicators such as job openings. Markets interpreted the print as lessening the chances of a 75bp hike at the 21 September FOMC, now 55% priced from around 75%. Meanwhile the expected peak in the fed funds rate has also fallen back to 3.83% from 3.95%. Next week’s CPI figures will also be key to whether it is 50 or 75 on 21 September.

Russia’s suspending gas flows through Nord Stream fully unwound the positive risk tones that came from the goldilocks payrolls report. Gazprom said officially that it extended the shutdown of the Nord Stream pipeline, citing a leak, and that the pipeline would not restart until repairs were fully implemented with no date given for re-opening (note it was scheduled to re-open on Saturday 3 September). The pipeline had been operating at 20% of its capacity and the absence of flows will continue to test Europe. The move to suspend gas flows was seen by some analysts as retaliation for the G7’s plan to put a price cap on Russian oil, such a cap is expected to ready before early December. Russia has already stated it will not sell oil to countries who agree to the plan, and for any plan to work it would require non-G7 nations to also agree. China and India have increased their imports of Russian oil over recent months. OPEC+ also meets tonight, with no change expected in terms of production targets. Brent oil was up 0.7% to $93.02.

Europe is faced with an even dire energy outlook and a few countries have announced fiscal packages. Over the weekend, Germany announced a €65b (~2%/GDP) support package for businesses and consumers. Meanwhile, Sweden and Finland announced liquidity and credit guarantee measures for power companies, many of which are struggling to post collateral as margin on derivative contracts. The more concerning impact at the moment is coming from the industrial sector, with numerous anecdotes of firms cutting back production. ArcelorMittal on the weekend said it was closing two of its plants in Germany given soaring energy costs. How monetary policy should respond to that is less clear, though the ECB will undoubtedly decide to hike rates this week. According to the latest Reuters poll, 30 of the 61 polled expect the ECB to announce a jumbo 75-basis point hike, 27 expect a 50-basis point rise – while four expect a 25-basis point hike.

In FX, currencies whipsawed with the USD (DXY) initially falling 0.6%, but fully reversing on the Russia headlines. On net the major moves were: EUR -0.1% to 0.9924; GBP -0.5% to 1.1476 and USD/KPY +0.1% to 140.13. The AUD (+0.0% to 0.6777) and NZD (+0.5% to 0.6095) were more resilient. Elsewhere, the PBOC set its daily yuan fix at a stronger-than-expected level for the eighth day in a row, helping USD/CNY stabilise around the 6.90 mark on Friday. In the session ahead focus will be on EUR and GBP given the gas headlines, and as the new UK PM addresses the country and unveils the UK’s response to the energy crisis.

Finally, there is more news of Chinse lockdowns with most of Shenzhen having gone into a weekend lockdown and kicking off mass. According to Caixin news, there are now 65m people in full/partial lockdown across 33 cities in China, while other cities are tightening restrictions ahead of China’s party congress on 16 October, where President Xi is expected to be elected to historic third, 5-year term. Following this, it is unclear whether China will start to pivot away from its zero-COVID policy. For as long as the policy exists, any stimulus measures are unlikely to gain traction, amid a challenging time for the Chinese property market and the economy in general.

Coming up this week:

Australia: All eyes on the RBA with two key events that could shape expectations. The RBA is expected to lift rates by 50bps on Tuesday (21 of 23 economists surveyed) and Governor Lowe is giving his annual Anika Foundation speech on Thursday, titled “Inflation and the Monetary Policy Framework ”. All focus will be on the outlook and whether the language supports a step down to 25bp hike increments after September, and on exactly what the Governor’s “even keel” comments mean in regard to charting inflation back to 2-3%, against an uncertain growth outlook. Also, this week are Q2 GDP figures on Wednesday and NAB pencils in growth of 0.7% q/q, below the consensus of 1.0%. Analysts will likely update their forecasts after pre-GDP partials early in the week with Inventories on Monday and Net Exports on Tuesday. The wage indicators out of GDP will also be parsed closely and they are expected to run much hotter than the WPI given they include hours and bonus payments.

Offshore:

• US: A quiet start with markets closed for Labor Day on Monday. Focus thereafter will be on the Services ISM on Tuesday and then to Fed Chair Powell on Thursday who is speaking in a moderated discussion on monetary policy hosted by the Cato Institute. It is not clear how much more Powell can add in terms of hawkishness given his Jackson Hole address. As for the Services ISM, this will be watched closely given the S&P Services PMI has been in contraction territory for two consecutive months (currently 44.1), with the consensus for the ISM much stronger at 55.2 from 56.7. Also on the calendar is the Fed’s Beige Book and the Fed’s Brainard also speaks on monetary policy. North of the border the Bank of Canada meets on Wednesday and where a 75bp hike to 3.25% is expected.

• CH: A big week of data which is likely to be overshadowed by China’s ongoing zero-COVID policy with Chengdu in lockdown and other cities tightening restrictions ahead of the party congress on 16 October, where President Xi is expected to be elected to a historic third five year term. The Trade Balance is on Wednesday, CPI/PPI on Friday, and Aggregate Finance figures are due anywhere from Friday to the following week. The Trade Balance is the statistic one to watch given slowing global growth and uncertain domestic demand given property headwinds, drought impacts, and China’s ongoing zero-COVID policy.

• EZ/UK: Fallout from the indefinite closure of Nord Stream the initial focus, and then Thursday’s ECB meeting. Markets are close to fully pricing in a 75bp hike after numerous ECB officials said they were leaning that way, though there is still likely to be a debate around 50 v 75. Also important will be the ECB’s outlook given activity so far has been resilient to the intense pressure coming from energy prices and inflation in general. Across the channel the new UK PM is announced on Monday and thereafter focus on their response to the cost of living crisis. BoE Governor Bailey talks on Wednesday.

• AU: Inventories/Profits, Job Ads, Inflation Gauge: Big day for data, but all mostly second-tier and unlikely to be market moving. The pre-GDP partials of Inventories and Profits are out with consensus at 1.5% q/q/ and 4.5% respectively. Perhaps of more interest is the unofficially monthly inflation gauge for August which may give an indication of the extent of inflation pressures in August. ANZ job ads are also out.

• NZ: Volume of Buildings: Unlikely to be market moving, consensus is for 1.0% q/q.

• CH: Caixin Services PMI: Consensus is for a fall to 540.0 from 55.5.

• EZ: Final-Services PMIs, Retail Sales: Retail Sales are expected to rise 0.4% m/m, while the final services PMI is expected to be the same as the preliminary of 50.2.

• UK: Liz Truss expected to be confirmed as UK PM tonight – market nerves about the Truss policy mix evident in the sell off in the GBP and UK gilts

• US: Labour Day Holiday: Markets are closed.

NAB Markets Research Disclaimer

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.